I’m picking up, after some months, the project I was working on over the summer on potential output. Obviously the political context is different now. But the questions of what potential output actually means, how tightly it binds, and how close the economy is to it at any given moment, are not going away. Previous entries: one, two, three, four, and five.

*

You’ve probably heard the story about Ed Rensi, the former McDonald’s CEO who claimed the company’s move to replace cashier’s with self-serve kiosks was a response to minimum wage increases.

“I told you so,” he writes. “In 2013, when the Fight for $15 was still in its growth stage, I and others warned that union demands for a much higher minimum wage would force businesses with small profit margins to replace full-service employees with costly investments in self-service alternatives.”

Is this for real? Maybe not: The shift toward kiosks has been happening for a while, so it’s not just a response to the recent minimum wage hikes; and it may not end up reducing labor costs anyway.

But let’s say the move is as as Rensi claims. Then we should call it what it is: an increase in labor productivity. With fewer workers McDonald’s will produce just as many hamburgers; in other words, production per worker will be higher. [1]

As I’ve suggested, this sort of thing is a real problem for a certain strand of minimum wage advocacy. Advocates like to point to productivity gains in response to higher wages as an argument in their favor. (The gains are usually imagined in terms of loyalty, motivation, lower turnover, etc. rather than machines, but functionally it’s the same.) But productivity gains can only reduce the job losses from a minimum wage increase if those losses are large; they are not consistent with a story in which employment stays the same. [2]

But at the macro level, this dynamic has different implications. If the McDonald’s case is typical — if higher labor costs regularly lead to higher productivity — then we need to rethink our idea of supply constraints. There is more space for expansionary policy than we usually think.

Let’s start at the beginning. Suppose there is some policy change, or some random event, that boosts desired spending in the economy. It could be more government spending, it could be lower interest rates, it could be a rise in exports. What happens then?

In the conventional story, higher spending normally leads to greater production of goods and services, which in turn requires higher employment. This leaves fewer people unemployed. Lower unemployment increases the bargaining power of workers, forcing employers to bid up nominal wages. [3] These higher wages are passed on to prices, leading to higher inflation. When inflation reaches whatever level is considered price stability, then we say the economy is at full employment, or at potential output. (In this story the two are equivalent.) If spending continues to rise past this point, the responsible authorities (normally the central bank) will intervene to bring it back down.

This is the story you’ll find in any good undergraduate macroeconomics textbook. It’s a reasonable story, as far as these things go. In the strong form it’s usually given in, it implies a hard limit to how much demand can increase before inflation starts rising unacceptably. Once the pool of unemployed workers falls to the “full employment” level, any further increase in employment will lead to rapid increases in money wages, which will be passed on one for one to inflation.

One place this chain can break is that new workers are not necessarily drawn from the ranks of the currently unemployed — that is, if the size of the laborforce is endogenous. Insofar as people counted as out of the laborforce are in fact available for employment (or net immigration responds to demand), an increase in output doesn’t have to reduce the ranks of the officially unemployed. In other words, the official unemployment rate may underestimate the space available for raising output via increased employment. This motivates the question of how much the the fall in laborforce participation since 2007 is due to demographics, and how much is due to weak demand.

The conventional story can also break down at two other places if productivity growth is endogenous. First, output can increase without a proportionate increase in employment. And second, wages can rise without a proportionate rise in prices.

It’s useful to think about this in terms of a couple of accounting identities, which in my opinion should be part of every macroeconomics textbook. [4] The first is obvious (but worth spelling out), the second a little less so:

(1) growth in demand = percent change in labor productivity + percent change in employment + inflation

(2) percent change in nominal wages = percent change in labor productivity + percent change in labor share + inflation

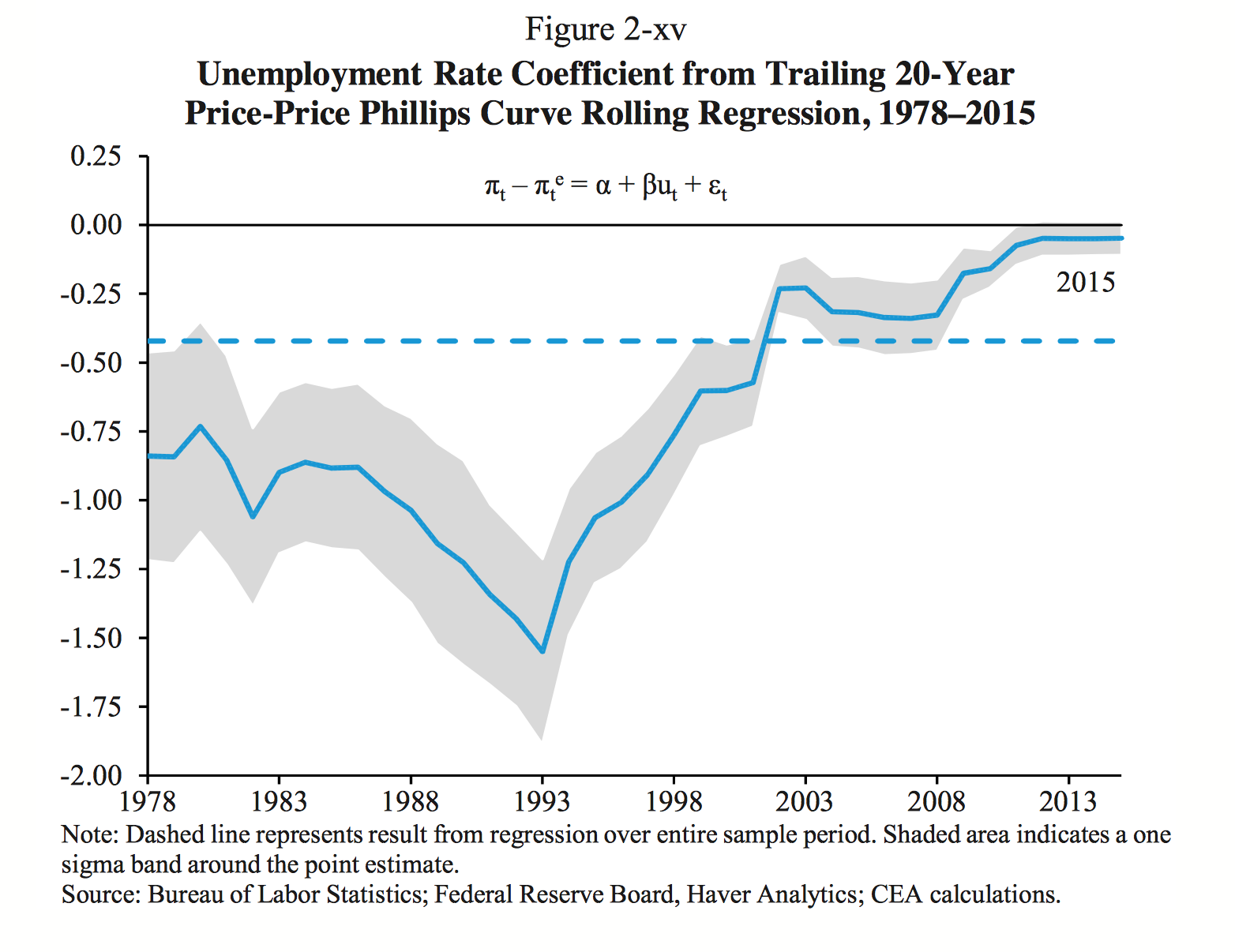

The standard story is that productivity change on its own due to technology, and the labor shared is fixed and can be ignored in this context. If productivity and labor share can be taken as given, then an increase in demand (money spent on final goods and services) must lead to higher inflation if either employment fails to rise, or if it rises only with higher wages. In this story, if nominal wages rise thanks to a lower unemployment rats, that will pass on one for one to inflation. Pick up an advanced undergraduate textbook like Blanchard or Krugman or Carlin and Soskice, and you will find a Phillips curve of exactly this form, with exactly this story behind it. [5] Policy discussions at central banks conducted in same terms.

This is what underlies idea of hard supply constraints. Output growth is dictated by the fixed, exogenous growth of the laborforce and of productivity. If changes in demand push the economy off that fixed trajectory, all you’ll get is higher or lower inflation. Concretely: To keep inflation at 2 percent, unemployment must be such as to generate nominal wage growth 2 points above the technologically-determined growth of productivity.

But an alternative story is that variation in demand can lead to adjustment in one of the other terms. One possibility is that the laborforce adjusts, as participation rates vary in response to demand conditions. This is what is most often meant by hysteresis: persistent deviations in unemployment from the “natural” level lead to people entering or exiting the laborforce. That implies that even when headline unemployment rates are fairly low, further increases in employment may be possible without a rise in wages. Another possibility is that while higher employment will lead to (or require) higher wages, the wage increase is not passed on to prices but comes at the expense of profits instead. This is Anwar Shaikh’s classical Phillips curve; I’ve written about it here before.

A third possibility is that higher wages are accompanied by higher productivity. Again, this appears as a problem when we are talking about wage increases from legislation, union contracts, or similar developments. But it’s not a problem if the wage increases are thanks to low unemployment. In this case, the joint movement of wages and productivity just means that output can rise higher — that supply constraints are softer. That’s what I want to focus on now.

There are a number of reasons why productivity might rise with wages. Some of them simply amount to mismeasurement of employment — it appears that output per worker is rising but really the effective number of workers is. Others are more fundamental. If productivity responds strongly and persistently to demand, it blurs the distinction between aggregate supply and aggregate demand, to the point that it’s not clear what “potential output” even means.

*

Suppose we do find a consistent pattern where, if demand is strong, unemployment is low, and wages are rising rapidly, then productivity growth is high. What could be happening?

1. Increased hours. If we measure productivity as output per worker, as we usually do, then an increase in average hours worked will show up as an increase in productivity. There is a cyclical component to this — in recessions, employers reduce hours as well as laying off workers. According to the BLS, seasonally adjusted weekly hours fell from 34.4 prior to the recession to a low of 33.7 in summer 2009. While a 2 percent fall in hours might seem small, it’s a big change in less than two years, especially when you consider that real output per worker normally rises by less than 2 percent a year.

2. Workers moving into real jobs from pseudo-employment or disguised unemployment. In any economy there are activities that are formally classified as jobs but are not employment in any substantive sense — you can take these “jobs” without anyone making a decision to hire you, and they don’t come with a wage or any similar claim on any established production process. Joan Robinson’s examples were someone who gathers firewood in a poor country, or sells pencils on streetcorners in a richer one. You could add work in family businesses and various kinds of self-employment and commission-based work to this category. In countries with traditional rural sectors — not the US — work on a family farm is the big item here. These activities absorb people who are unable to find formal jobs; the marginal product of additional workers here is normally very low. So if higher demand draws people from this kind of disguised unemployment back into regular jobs, measured productivity will rise.

3. Workers may be more fully utilized at their existing jobs. Because hiring and firing is costly, business don’t immediately adjust staffing in response to changes in sales. when demand falls, businesses will initially keep some redundant workers because paying them is cheaper than laying them off and replacing them later; and when demand rises, businesses will first try to get more work out of existing employees rather than paying the costs of hiring more. Some of this takes the form of the hours adjustment above, but some of it simply takes the form of hiring “too little” or “too much” labor for the current level of production. These changes in the utilization of existing labor will show up as changes in labor productivity.

4. Higher wages may lead to more capital-intensive production. This is the McDonald’s story: When labor gets more expensive (or scarcer), businesses use more capital instead. This is presumably what people mean when they say “Econ 101” shows that rising wages lead to less employment (assuming they mean anything at all). This may be seen as a negative when it’s a question of raising wages through legislation or unions, but it shouldn’t be when it’s a question of rising wages due to labor scarcity. Insofar as businesses can substitute machines for labor, rising wages will not be passed on to prices, so there is more space to push unemployment down.

5. Productivity-boosting innovations may be more likely when demand is strong and wages rise. This is a variant of the previous story. Now instead of high wage leading business to adopt more capital-intensive techniques from those already available, they redirect innovation toward developing new labor-saving techniques. Conceptually this is not a big difference, but it implies a different signal in the data. In the previous case we would expect the productivity improvements to be associated with higher investment and to be concentrated at the firms actually experiencing higher wages costs; in this case they might not be.

6. The composition of employment may shift toward higher-productivity sectors. This might happen for either of two reasons. First, higher wages will disproportionately raise costs for more labor-intensive sectors; these higher costs may be absorbed by profits or by prices, but either way they will presumably depress growth in those sectors to the benefit of less labor-intensive, more productive ones. Second, it may so happen that the more income-elastic sectors are also higher-productivity ones. In the short run this is presumably true since durables and investment goods are both capital-intensive and income-elastic. Over the longer run, the opposite is more likely — the composition of demand slowly but steadily shifts toward lower-productivity sectors.

7. The composition of employment may shift toward higher-productivity firms. This sounds similar but it’s a different story. Technical change isn’t an ineffable output-raising essence diffusing across society, it’s embodied in specific new production processes and new businesses — Schumpeter’s new plant, new firms, new men. This means that productivity increases often require new or growing firms to attract workers away from established ones. Given the “frictions” in the labor market, this will require offering a wage significantly above the going rate. And on the other side the fact that the least productive firms can’t afford to pay higher wages will cause them to decline or exit, which also raises average productivity. When wages are flat, on the other hand, low-productivity firms can continue operating. In this sense, higher wages are an integral part of productivity growth. [6]

8. There may be increasing returns in production. It may literally be the case that output per worker rises — at the firm, industry or economy-wide level — when the number of workers rises. Or this may be a more abstract version of some of the stories above. It’s worth noting that increasing returns is an area where the intuitions of people with economics training diverge sharply from people who look at the economy through other lenses. To almost anyone except an economist, it’s obvious that costs normally fall as more of something is produced. [7]

All of these stories imply that higher demand should lead to higher measured labor productivity. But to figure out how strong this relationship is in reality, we’ll look at different data depending on which of these stories we think it works through.

Another important difference between the stories is they imply different domains over which the relationship should operate. The first three suggest a more or less immediate response of productivity to changes in demand, but also one that cannot continue indefinitely. There’s limits to how much hours per worker can rise and how much additional effort can be extracted from the existing workforce, and a limited pool of disguised unemployment to draw from. (The last is not true in developing countries, where the “latent reserve army” in subsistence agriculture may be effectively unlimited.) The other mechanisms are presumably slower, requiring a sustained “high-pressure economy.” With these stories, increased demand may push the economy up against supply constraints, with rising inflation, bottlenecks, and so on; but if it keeps pushing against them, eventually they’ll give. In this case, potential output is a medium-term constraint — over longer periods it can adjust to actual output, rather than the reverse. So in the opposite of conventional story, a temporary increase in inflation can lead to a permanent increase in output. People like Laurence Ball say exactly this about hysteresis, but they are usually thinking of the longer-run adjustment coming on the laborforce side.

If we follow this a step further, we could even say that in the long run, the big problem isn’t that excessively high wages do lead to the substitution of capital for labor but that excessively low wages don’t. People like Arthur Lewis argue that it’s the low wages of poor countries that have led to low productivity there, and not vice versa; there’s a well-known argument that the reason the industrial revolution happened first in Britain rather than in China or India (or Italy or France) is not that that the necessary technical innovations were present only in Britain. They were present many places; it was the uniquely high cost of British labor that made them profitable to adopt for production.

*

I think that productivity does respond to demand. I think this is a good reason to doubt whether the US economy close to “potential output” today, and to doubt what, if anything, this concept actually means. But I also think we need to be clearer about how they are linked concretely. If we want to tell a story about productivity responding to demand, it makes a difference which of the stories above we have in mind. Heterodox people, it seems to me, are too quick to just invoke Verdoorn’s law (productivity rises with output), and justify it with some vague comments about how labor is used more efficiently when it is scarce. [8] Does this apparent law work via substitution of machines for labor, or through fuller utilization of existing employees’ times, or through reallocation of labor to more productive firms and/or industries, or through a labor-saving-bias in technical change, or pure increasing returns, or what? If you’re just making a formal model it may not matter. But if we want to connect the model to concrete historical developments, it certainly does.

Personally, I am most interested in the reallocation stories. They shift our idea of the fundamental constraint on capitalist economies from biophysical resources, to coordination. The great difficulty for any program of raise or transform production — industrialization, wartime mobilization, decarbonization — isn’t the limited supply of “real” resources, but the speed at which people’s productive activity can be redirected in a coordinated way. This connects with the historical fact that the more rapid and the larger scale is economic development, the more it requires some form of central planning. And it implies that at the most basic level, what the capitalist provides is not money or means of production, but cooperation.

To tell this story, it would be nice if big shifts in productivity growth took the form of changes in the composition of employment, rather than higher output per worker in given jobs. That may or may not be there in the data. For the more immediate question of how much space there is in the US for further expansion, it doesn’t matter as much which of these stories is at work, as long as we can show that at least some of them are. [9]

In the next post or two — which I hope to write in the next week, but we’ll see — I will ask what we can say about the link between demand and productivity based on historical US data. In particular, it’s fairly straightforward to decompose changes in output per worker into three components: within-industry output per hour, within-industry hours per worker, and shifts in the employment between industries. Splitting up productivity growth this way cannot, of course, directly establish a causal link with demand. but it can help clarify which stories are plausible and which are not.

[1] Throughout this discussion, I use “productivity” to mean labor productivity — output per worker or per hour. There is also “total factor productivity,” which purports to be a measure of output for a given input of labor and capital. This concept, which IMF chief economist Paul Romer memorably called “phlogiston,” is measured as the residual from a production function — the output growth the function does not explain. Since construction of the production function requires several unobseravable parameters, total factor productivity cannot be derived even in principle from economic data. It’s a fun toy for economic theory but useless for describing the behavior of actual economies.

Nonetheless it is widely used — for instance by the CBO as discussed here. As Nathan Tankus pointed out to me the other day, under the ARRA Medicare payments to hospitals are reduced each year based on an estimate of TFP growth for the economy as a whole. It’s a great example of the crackpot wonkery of the law’s authors.

[2] Unless productivity improvements all take the form of higher quality, rather than higher output per worker.

[3] This unemployment-money wages relationship was the original Phillips curve, but it’s better now to refer to it as a wage curve.

[4] It’s a topic for another time, but I think it would be very natural to replace the “aggregate supply” framework of the textbooks with these two identities.

[5] Other textbooks, like Mankiw, base the wage-unemployment relationship on a labor-supply curve rather than a bargaining relationship. Graduate textbooks, of course, replace the institutional detail of workers and employers with a single representative agent, in order to make more space for playing with math.

[6] Andrew Glyn and his coauthors have a good discussion of this in the context of the postwar boom in Capitalism Since 1945 (p. 122-123).

[7] For example, here’s Laurie Winkless in Science and the City, which happens to be sitting nearby:

Bessemer’s system rapidly began to change the world of steel manufacturing, and by 1875, costs had dropped to $32 (£23) per tonne. as always, in the supply-and-demand equation, the availability of cheap, high-quality steel made it immensely popular, leading to another huge drop in the price per tonne.

Winkless has made the mistake of studying the actual history of the steel history. If she were an economist, she would know that in the world of supply and demand, immense popularity makes prices rise, not fall!

[8] In Shaikh’s Capitalism, for example, there are a number of models that rely on the claim that productivity rises with output. It’s a big book and I may well have missed a part where he explains more fully why this is true. But as far as I can tell, all he says is that higher unit labor costs “provide a strong incentive for firms to raise productivity.”

[9] The politics of this question under Trump are for another time. But certainly Jeff Spross is right that we don’t want to oppose Trump’s (dubious) plans for a big stimulus by embracing the politics of austerity. We should not respond to Trump by reflexively insisting that the US is already at full employment, and by mocking “vulgar Keynesians” who think there might still be problems for macro policy to solve.

EDIT: Fixed the footnote numbering, which was garbled before.

While the significance lines can’t be taken literally given that these are overlapping periods, the figure makes clear that between 1947 and 2008, there were very few sustained periods in which both employment and productivity growth made large departures from trend in the same direction.

While the significance lines can’t be taken literally given that these are overlapping periods, the figure makes clear that between 1947 and 2008, there were very few sustained periods in which both employment and productivity growth made large departures from trend in the same direction.

{kind=link}