(I write a monthlyish opinion piece for Barron’s. A shorter version of this post appeared there in June 2025. My previous pieces are here.)

As recession fears grow, it’s natural to look back to the experience of past downturns to think about how we might better prepare for the next one. Here is one lesson: We’re less likely to see a deep and persistent downturn if we can sustain state and local government spending.

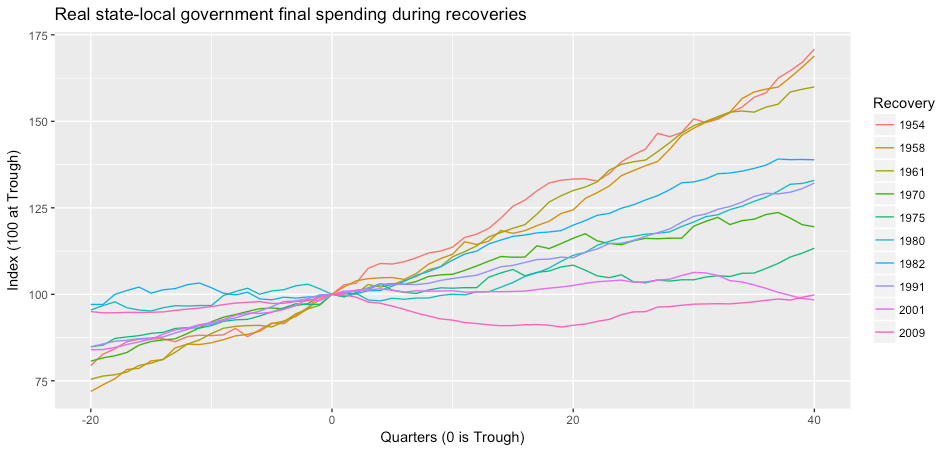

An underappreciated macroeconomic development of the past decade was the sustained turn to austerity at the state and local level. Between 2007 and 2013, state and local employment fell by 700,000 — a decline without precedent in US history. If public employment per capita were the same today as in 2005, there would be more than 2 million additional people working for state and local governments. (See the figure nearby.)

Some may see this as a good thing — fewer public employees means less government waste.

But in the American federal system, it is state and local governments that provide the public services that people and businesses rely on. In our daily lives, we depend on teachers, firemen, sanitation workers, librarians and road crews employed by our state, county or city. The only federal employee we are likely to encounter is the person delivering the mail.

And from an economic standpoint, spending is spending, whether useful or wasteful. There are still debates over whether the 2007 stimulus was big enough. But what’s sometimes forgotten is that increased federal spending was accompanied by deep spending cuts at the state and local level. As a share of potential GDP, state and local spending fell by a full point between 2007 and 2013, and has remained at this lower level ever since. As people like Dean Baker and Rivka Deutsch warned at the time, these cutbacks canceled out much of the federal stimulus.

Some might argue that these spending cuts, while unfortunate, were unavoidable given state balanced-budget requirements. It is certainly true that state governments have less fiscal room for maneuver than the federal government does, and local governments have still less. But balanced-budget rules don’t mean that these governments cannot borrow at all — if it did, there wouldn’t be a $3 trillion municipal-debt market.

Balanced budgets mean many things. In some states, balanced budgets are written into the state constitution, but in others, they are simply statutes that can be waived by a vote of the legislature. In some places, revenues and expenditure must actually balance at the end of the year, while in others, the adopted budget must balance but the state may end the year with a deficit if revenues end up falling short. Most important, balanced budget rules normally apply only to the operating budget; they don’t restrict borrowing for investment spending.

Yet it was state and local investment that fell most steeply following the Great Recession. Adjusted for inflation, state and local capital expenditure fell by 15 percent between 2007 and 2013, by far the steepest drop on record. In real terms, investment spending at the state and local level was no higher in 2022 than it was 15 years earlier.

Not surprisingly, this fall in state capital spending was accompanied by a fall in state and local borrowing. Over the decade of the 2010s, nominal state and local debt was flat. In other words, net borrowing by state and local governments was essentially zero — the first sustained period in modern US history where that was true. This persistent loss of demand may have done as much as the disruptions to the financial system to hold back recovery after the 2007-2009 recession.

In 20078, there was a fiscal response on the federal level, even if it turned out to be too small. In the current climate, that seems unlikely. So whether the next recession is followed by a quick recovery or turns into a sustained period of weak growth, will depend even more on how well state and local spending holds up.

It’s not hard to imagine governments feeling compelled to curbing spending in a downturn. Many are already stretched thin even in these comparatively flush times. Maryland and Los Angeles, for example, both recently saw their credit ratings downgraded. Washington DC, whose tax base is suffering from federal layoffs, already faces rising borrowing costs.

Even where the local economy holds up better, governments may feel it is prudent to cut back on investment — a classic example of a choice that may look individually rational but, when taken across the board, is collectively self-defeating, as spending cuts in one place result in lost income elsewhere.

Nor is state fiscal capacity only a concern in a downturn. It will take years for to return many federal services to their pre-DOGE levels, assuming future administrations even wish to do so. But demand for these services has not gone away. So states — especially larger ones — may find themselves forced to assume responsibility for things like food safety or weather data, for which they previously depended on Washington. States and localities may also find themselves paying more in areas where they already had primary responsibility, like education and transportation. All this will call for bigger budgets and, at least in some cases, more debt, not just in a recession but perhaps indefinitely.

What can be done to help states find the financial space to maintain spending in a downturn, or to increase it to compensate for federal cutbacks?

The most basic, but also most difficult, requirement is a change in outlook among state and local budget officials. The idea that government should spend more in a recession is a hard enough sell at the federal level; it’s not something state (let alone local) officials think about at all. The natural instinct of state budget makers to federal cutbacks will be to cut their own spending as well; it will not be easy to convince them that they should, in effect, steer into the skid by spending more.

But circumstances can force policymakers out of their comfort zones. The problems of providing public goods and stabilizing the macroeconomy will not go away just because the federal government steps back from solving them. Even if it’s impossible for other levels of government to fully replace the federal government, small steps in that direction are still worth taking. We can’t expect states and localities — even California or New York City — to recreate NASA or NIH. But it is certainly possible for state and local governments to do more with their budgets than they currently do.

In a number of states, even capital spending is financed out of current revenues rather than with debt. Unsurprisingly, public investment in these states appears to be more pro-cyclical than elsewhere. A taboo against borrowing even for capital projects means, in effect, letting fiscal space go to waste. This will be especially costly in a downturn if a federal stimulus is not forthcoming.

Almost all states have constitutional or statutory ceilings on debt and debt service. In practice, these limits are more important than balanced-budget rules, since they apply to borrowing for capital spending as well as operations. These are worth revisiting. There is nothing wrong with these in principle. But in some cases, they may be excessively restrictive, limiting the issue of new debt even in cases where the risks are minimal and the social value is great.

Of particular concern are limits that are based only on the most recent year of tax revenue or state income, rather than an average of the past several years. These rules can impart a pro-cyclical bias to capital spending, reducing it during a recession even though that is when it is most macroeconomically valuable, and when borrowing (and perhaps other) costs are lower. It’s a perverse form of fiscal guiderail that encourages states to borrow when interest rates are high, and discourages it when rates are low.

Another important limit on state fiscal space is credit ratings. State and local budget officials are deeply protective of their credit ratings; fear of a downgrade can discourage new borrowing even when there is no legal obstacle and when the capital projects it would finance are sorely needed. These concerns are certainly understandable, if perhaps sometimes exaggerated. The problem is that rating agencies may not be the best judges of government credit risk.

In the wake of the financial crisis of 2007-2009, there was a brief period of intensified scrutiny of rating agencies’ practices. The obvious problem was the AAA ratings given to mortgage-backed securities that, in retrospect, were anything but risk-free. But on the other side, rating agencies were giving systematically lower ratings to municipal borrowers than to corporate borrowers with the same chance of default. A review by Moody’s at the time suggested that the historical default rate on A-rated municipal bonds was comparable to that on AAA-rated corporate debt.

This problem has receded from view, but it was never really addressed. More recent studies have confirmed that, after adjusting for their different tax treatment, municipal borrowers pay substantially higher interest rates than corporate borrowers with similar default risk — a difference that might be explained, at least in part, by their different treatment by rating agencies.

More broadly, credit ratings are a problematic service for for-profit businesses to provide in the first place. By their nature, they need to be freely available to anyone who might buy the rated debt. Meanwhile the debt issuer, who pays for them, has opposing interests to those of the lenders who will use them. Credit ratings are public goods; there’s a clear case for them to be provided by a public rating agency, as some economists have proposed. If bond ratings were a public service, based on consistent, transparent principles, that might relieve some of the anxiety that deters state and local governments from making full use of their fiscal capacity.

A more radical idea would be a public option not just for credit rating, but for lending. A few years ago, there was a wave of interest in the idea of a national investment authority. These proposals did not really make sense in the form they were originally put forward; given that the federal government already enjoys the lowest interest rate of any borrower in the economy, there is no use in creating a new entity to issue debt on its behalf. But there is a better case for a new public entity to lend to state and local governments, which face more serious constraints on their financing.

Unfortunately, the same federal retrenchment that calls for a larger role for state governments, also means proposals like a public rating agency or a national investment authority are unlikely to get off the ground for the foreseeable future.

The one place where capacity does still exist at the federal level is the Federal Reserve. Indeed, thanks to the Supreme Court’s ruling in Trump v. Wilcox, the Fed’s stature has been elevated; it is now, apparently, the only independent agency constitutionally permitted at a federal level.

Many people (including me) have long called for the Fed to support the market for municipal debt, in the same way that it supports other financial markets. For years, there was debate about whether this was something the Fed had the legal authority to do. But during the pandemic, the Fed made it clear that it did, by creating the Municipal Liquidity Facility (MLF), which promised up to $500 billion in loans to state and local governments.

In the event, only a handful of municipal borrowers made use of the MLF. But as thoughtful observers of the program pointed out, this greatly understates its impact. The existence of a Fed backstop meant that muncicpal borrowers were less risky than they would otherwise have been, which allowed them to access private credit on more variable terms. A study from the Dallas Fed found that, despite its limited makeup, the existence of the MLF led to interest rates on municipal bonds as much s five points lower than they otherwise would have been.

Like many pandemic measures, the MLF was quickly wound down. But there’s a strong case that something similar should become part of the Fed’s permanent repertoire.This wouldn’t have to be an open ended commitment to lend to local governments; it might, for instance, be offered only in response to natural disasters — or recessions.

Supporting state and local borrowing is presumably not a role that the Fed wants. Stabilizing demand is definitely not a role that state governments want. In a more rational political system, these responsibilities would land elsewhere. But in the real world, problems must be solved by those who are in a position to solve them. If the federal government is stepping down, someone else is going to have to step up.

(I am an occasional contributor to roundtables of economists in the magazine The International Economy. The topic of this month’s roundtable was: Is a serious global debt crisis possible?)

As Hyman Minsky famously described, when market participants believe that crises are possible, they behave in ways that make the system relatively robust. Only when the chance of a crisis is deemed very low, or forgotten entirely, do financial markets accept the degree of leverage and illiquid commitments that make a crisis possible.

This means, among other things, that crises are inherently difficult if not impossible to predict. A predicted crisis is a crisis that does not occur.

So to the question of whether a serious crisis is likely in the near future, the sensible answers range from “maybe” to “I don’t know.”

There are other questions we have a better chance of answering. First, are the authorities able to handle a crisis if one does occur? And second, what kind of spillovers will a financial crisis have for the rest of the economy?

On both questions, the answers would seem to be reasonably encouraging for the rich countries, less so for the developing world.

The 2007-2009 financial crisis and the 2020 pandemic were very different events in many ways. But one thing they had in common, is that both demonstrated the awesome power of a committed central bank to overcome almost any kind of disruption to the financial system. The Fed, in particular, was willing to buy a much wider range of assets, and intervene in a wider range of markets, than almost anyone would have previously predicted. Today there can be little doubt that the Fed can stem the contagion from even the biggest bank failure or sovereign default, if it wishes to.

That last caveat is worth emphasizing. The decade after 2007 saw a sharp divergence between the US and Europe. While the Fed moved aggressively to repair the financial system, the ECB moved more slowly — in part because of tighter institutional constraints, but also, it’s now clear, because decision makers at the ECB saw the crisis as a chance to push through a broader set of policy changes. Not only Greece but also Spain, Italy and Ireland were in effect held hostage by the ECB, which refused to restore liquidity to their banking systems until they accepted various structural reforms.

This divergence suggests that, in the rich countries, the question may be less what central banks are able to do in response to a banking crisis, and more what they are willing to do.

As for the second question, it’s worth maintaining a bit of skepticism that finance is as important to the rest of us as it appears in its own eyes. In retrospect, it seems clear that the long-term damage to the US economy after the 2007 crash had more to do with the collapse of housing market — a pillar of the real economy — than with the the financial aftershocks that got so much attention at the time. When we think about the dangers of a financial crisis today, we should ask not only what are the chances of bank failures and asset market disruptions, but how important those markets are for real activity. Mortgages and cryptocurrencies are very different in this respect.

For the developing world, unfortunately, such a relatively sanguine view is harder to sustain. Central banks are much less powerful in countries where a large fraction of domestic obligations involve foreign currencies, and where financial conditions are largely determined beyond the borders. Serious spillovers to the real economy are more likely in this case. If there is a crisis in the near future, it may finally teach the lesson that the world has been slowly learning: Outside the core of the world economy, an essential requirement for any kind of macroeconomic management is a degree of financial delinking.

The euro crisis of the 2010s is well in the past now, but it remains one of the central macroeconomic events of our time.But the nature of the crisis remains widely misunderstood, not only by the mainstream but also — and more importantly from my point of view — by economists in the heterodox Keynesian tradition. In this post, I want to lay out what I think is the right way of thinking about the crisis. I am not offering much in the way of supporting evidence. For the moment, I just want to state my views as clearly as possible. You can accept them or not, as you choose.

During the first 15 years of the euro, a group of peripheral European countries experienced an economic boom followed by a crash, with GDP, employment and asset prices rising and then falling even more rapidly. As far as I can tell, there are four broad sets of explanations on offer for the crises in Greece, Ireland, Italy, Portugal and Spain starting in 2008.

(While the timing is the same as the US housing bubble and crash, that doesn’t mean they are directly linked — however different they are in other respects, most of the common explanations for the European crisis I’m aware of locate its causes primarily within Europe.s)

The four common stories are:

1. External imbalances. The fixed exchange rate created by the euro, plus some mix of slow productivity growth in periphery and weak demand growth in core led to large trade imbalances within Europe. The financial expansion in the periphery was the flip side of a causally prior current account deficit.

2. Monetary policy. Both financial instability and external imbalances were result of Europe being far from an optimal currency area. Trying to carry out monetary policy for the whole euro area inevitably produced a mix of stagnation in the core and unsustainable credit expansion in the periphery, since a monetary stance that was too expansionary for Greece, Spain etc. was too tight for Germany.

3. Fiscal irresponsibility. The root of the crisis in peripheral countries was the excessive debt incurred by their own governments. The euro was a contributing factor since it led to an excessive convergence of interest rates across Europe, as markets incorrectly believed that peripheral debt was now as safe as debt of core countries.

4. Banking crises. The booms and busts in peripheral Europe were driven by rapid expansions and then contractions of credit from the domestic banking systems, with dynamics similar to that in credit booms in other times and places. The specific features of the euro system did not play any significant role in the development of the crisis, though they did importantly shape its resolution.

In my view, the fourth story is correct, and the other three are wrong. In particular, trade imbalances within Europe played no role in the crisis. In this post, I am going to focus on why I think the external balances story is wrong, since that’s the one that people who are on my side intellectually seem most inclined toward.

As I see it, there were two distinct causal chains at work, both starting with a credit boom in the peripheral countries.

easy credit —> increased aggregate spending —> increased output and income —> increased imports —> growing trade deficit —> net financial inflows

That the two outcomes — external imbalances and banking crisis — went together is not a coincidence. But there is no causal link from the first to the second. Both rather are results of the same underlying cause.

Yes, in the specific conditions of the late-2000s euro area, a credit boom led to an external deficit. But in principle it is perfectly possible to have a a credit-financed asset bubble and ensuing crisis in a country with a current account surplus, or one with current account balance, or in a closed economy. What was specific to the euro system was not the crisis itself, but the response to it. The reason the euro made the crisis worse because it prevented national governments from taking appropriate action to rescue their banking systems and stabilize demand.

This understanding is, I think, natural if we take a “money view” of the crisis, thinking in terms of balance sheets and the relationship between income and expenditure. Here is the story I would like to tell.

Following the introduction of the euro in 1998, there were large credit expansions in a number of European countries. In Spain, for example, bank credit to the non-financial economy increased from 80 percent of GDP in 1997 to 220 percent of GDP in 2010. Banks were more willing to make loans, at lower rates, on more favorable terms, with less stringent collateral requirements and other lending standards. Borrowers were more willing to incur debt. The proximate causes of this credit boom may well have been connected to the euro in various ways. European integration offered a plausible story for why assets in Spain might be valued more highly. The ECB might have followed a less restrictive policy than independent central banks would have (or not — this is just speculation). But the euro was in no way essential to the credit boom. Similar booms have happened in many other times and places in the absence of currency unions — including, of course, in the US at roughly the same time.

In most of these countries, the bulk of the new credit went toward speculative real estate development. (In Greece there was also a big increase in public-sector borrowing, but not elsewhere.) The specifics of this lending don’t matter too much.

Now for the key point. What happens when a a Spanish bank makes a loan? In the first step the bank creates two new assets – a deposit for the borrower, and the loan for itself. Notice that this does not require any prior “saving” by a third party. Expansion of bank credit in Spain does not require any inflow of “capital” from Germany or anywhere else.

Failure to grasp is an important source of confusion. Many people with a Keynesian background talk about endogenous money, but fail to apply it consistently. Most of us still have a commodity money or loanable-funds intuition lodged in the back of our brains, especially in international contexts. Terms like “capital flows” and “capital flight” are, in this respect, unhelpful relics of a gold standard world, and should probably be retired.

Back to the story. After the deposits are created, they are spent, i.e. transferred to someone else in return, in return for title to an asset or possession of a commodity or use of a factor of production. If the other party to this transaction is also Spanish, as would usually be the case, the deposits remain in the Spanish banking system. At the aggregate level, we see an increase in bank credit, plus an increase in asset prices and/or output, depending on what the loan finances, amplified by any ensuing wealth effect or multiplier.

To the extent that the loans finance production – of beach houses in Galicia say — they generate incomes. Some fraction of new income is spent on imported consumption goods. Probably more important, production requires imported intermediate and capital goods. By both these channels, an increase in Spanish output results in higher imports. If the credit boom leads Spain to grow faster relative to its trade partners — which it will, unless they are experiencing similar booms — then its trade balance will move toward deficit.

(That changes in trade flows are primarily a function of income growth, and not of relative prices, is an important item in the Keynesian catechism.)

Now let’s turn to the financial counterpart of this deficit. A purchase of a German good by a Spanish firm requires a bank deposit to be transferred from the Spanish firm to the German firm. Since the German firm presumably doesn’t hold deposits in a Spanish bank, we’ll see a reduction in deposits in the Spanish banking system and an equal increase in deposits in the German banking system. The Spanish banks must now replace those deposits with some other funding, which they will seek in the interbank market. So in the aggregate the trade deficit will generate an equal financial inflow — or, better said, a new external liability for the Spanish banking system.

The critical thing to notice here is that these new financial positions are generated mechanically by the imports themselves. It is simply replacing the deposit funding the Spanish banks lost via payment for the imports. The financial inflow must take place for the purchase to happen — otherwise, literally, the importer’s check won’t clear.

But what if there is an autonomous inflow – what if German wealth owners really want to hold more assets in Spain? Certainly that can happen. These kinds of cross-border flows may well have contributed to the credit boom in the periphery. But they have nothing to do with the trade balance. By definition, autonomous financial flows involve offsetting financial transactions, with no implications for the current account.

Suppose you are a German pension fund that would like to lend money to a Spanish firm, to take advantage of the higher interest rates in Spain. Then you purchase, let’s say, a bond issued by Spanish construction company. That shows up as a new liability for Spain in the international investment position. But the Spanish firm now holds a deposit in a German bank, and that is an equal new asset for Spain. (If the Spanish firm transfers the deposit to a Spanish bank in return for a deposit there, as I suppose it probably would, then we get an asset for Spain in the interbank market instead.) The overall financial balance has not changed, so there is no reason for the current account to change either. Or as this recent BIS paper puts it, “the high correlations between gross capital inflows and outflows are overwhelmingly the result of double-entry bookkeeping”. (The importance of gross rather than net financial positions for crises is a pint the bIS has emphasized for many years.)

It may well happen that the effect of these offsetting financial transactions is to raise incomes in Spain (the contractor got better terms than it would at home) and/or banking-system liquidity (thanks to the fact that the Spanish banking system gets the deposits without the illiquid loan). This may well contribute to a rise in incomes in Spain and thus to a rise in the trade deficit. But this seems to me to be a second-order factor. And in any case we need to be clear about the direction of causality here — even if the financial inflows did indirectly cause the higher deficit, they did not in any sense finance it. The trade balances of Germany and Spain in no way affect the ability of German institutions to buy Spanish debt, any more than a New Yorker’s ability to buy a house in California depends on the trade balance between those states.

At this point it’s important to bring in the TARGET2 system.

Under normal conditions, when someone wants to take a cross-border position within the euro systems the other side will be passively accommodated somewhere in the banking system. But if a net position develops for whatever reason, central banks can accommodate it via TARGET2 balances. Concretely, let’s say soon in Spain wants to make a payment to someone in Germany, as above. This normally involves the reduction of a Spanish bank’s liability to the Spanish entity and the increase in a German bank’s liability to the German entity. To balance this, the Spanish bank needs to issue some other liability (or give up an asset) while the German bank needs to acquire some asset. Normally, this happens by the Spanish bank issuing some new interbank liability (commercial paper or whatever) which ends up, perhaps via various intermediaries, as an asset for a German bank. But if foreign banks are unwilling to hold the liabilities of Spanish banks (as happened during the crisis) the Spanish bank can instead borrow from its own central bank, which in turn can create two offsetting positions through TARGET2 — a liability to the euro system, and a reserve asset (a deposit at the ECB). Conceptually, rather than the transfer of the despot being offset by a liability fro the Spanish to the German bank the interbank market, it’s now offset by a debt owed by the Spanish bank to its own national central bank, a debt between the central banks in the TARGET2 system, and a claim by the German bank against its own national central bank.

In this sense, within the euro system TARGET2 balances stand at the top of the hierarchy of money. Just as non financial actors settle their accounts by transfers of deposits at commercial banks, and banks settle their balances by transfers of deposits at the central bank, central banks settle any outstanding balances via TARGET2. It plays the same role as gold in the old gold standard system. Indeed, I sometimes think it would be better to describe the euro system as the “TARGET2 system.”

There is however a critical difference between these balances and gold. Gold is an asset for central bank; TARGET2 balances are a liability. When a payment is made from country X to country Y in the euro area, with no offsetting private payment, the effect on central bank balance sheets is NOT a decrease in the assets of the central bank of X (and increase in the assets of the central bank of Y) but an increase in the liabilities of the central bank of X. This distinction is critical because assets are finite and can be exhausted, but new liabilities can be issued indefinitely. The automatic financing of payments imbalances through the TARGET2 system seems like an obscure technical detail but it transforms the functioning of the system. Every national central bank in the euro area is in effect in the situation of the Fed. It can never be financially constrained because all its obligations can be satisfied with its own liabilities.

People are sometimes uncomfortable with this aspect of the euro system and suggest that there must be some limit on TARGET2 balances. But to me, this fundamentally misunderstands the nature of a single currency. What makes “the euro” a single currency is not that it has the same name, or that the bills look the same in the various countries, or even that it trades at a fixed ratio of one for one. What makes it a single currency is that a bank deposit in any euro-area country will settle a debt in any other euro-area country, at par. TARGET2 balances have to be unlimited to guarantee the this will be the case — in other words, for there to be a single currency at all.

(In this sense, we should not have been so fixed on the question of being “in” versus “out” of the euro. The relevant question is the terms on which payments can be made from one bank account another, for settlement of which obligations.)

The view of the euro crisis in which trade imbalances finance or somehow enable credit expansion is dependent on a loanable-funds perspective in which incomes are fixed, money is exogenous and saving is a binding constraint. It’s implicitly based on a model of the gold standard in which increased lending impossible without inflow of reserves — something that was not really true in practice even in the high gold standard era and isn’t true even in principle today. What’s strange is that many people who accept this view would reject those premises – if they realized they were applying them.

Meanwhile, on the domestic side, abundant credit was bidding up asset prices and encouraging investment that was, ex post, unwise (and in some case fraudulent, though I have no idea how important this was quantitatively). When asset prices collapsed and the failure of investment projects to generate the expected returns became clear, many banks faced insolvency. There was a collapse in activity in the real-estate development and construction activity that had driven the boom and, as banks tightened credit standards across the board, in other credit-dependent activity; falling asset values further reduced private spending; all these effects were amplified by the usual multiplier. The result was a steep fall in output and employment.

I don’t believe there’s any sense in which a sudden stop of cross-border lending precipitated the crisis. Rather, the “nationalization” of finance came after. Banks tried to limit their cross-border positions came only once the crisis was underway, as it became clear that there would be no systematic euro-wide response to insolvent banks, so that any rescues or bailouts would be by national governments for their own banks.

Credit-fueled asset booms and crashes have happened in many times and places. There was nothing specific to the euro system about the property booms of the 2000s. What was specific to the euro system was what happened next. Thanks to the euro, the affected governments could not respond as developed country governments have always responded to financial crises since World War II — by recapitalizing insolvent banks and shifting public budgets toward deficit until private demand recovers.

(I write a monthly-ish opinion piece for Barron’s. This is my most recent one. You can find earlier ones here.)

Since the onset of the pandemic, policy makers in the U.S. and elsewhere have embraced a more active role for government in the economy. The extraordinary scale and success of pandemic relief, the administration’s embrace of the expansive Build Back Better program, and the revived industrial policy of the Inflation Reduction Act and the Chips and Science Act all stand in sharp contrast with the limited-government orthodoxy of the past generation.

The debt ceiling deal announced this weekend looks like a step back from this new path – albeit a smaller one than many had feared. Supporters of industrial policy and more robust social insurance have reason to be disappointed – especially since the administration, arguably, had more room for maneuver than it was willing to use.

To be fair, the agreement in part merely anticipates the likely outcome of budget negotiations. Regardless of the debt ceiling, the administration was always going to have to compromise with the House leadership to pass a budget. The difference is that in a normal negotiation, most government spending continues as usual until a deal is reached. Raising the stakes of failure to reach a deal shifts the balance in favor of the side more willing to court disaster. Allowing budget negotiations to get wrapped up with the debt ceiling may have forced the administration to give up more ground than it otherwise would.

The Biden team’s major nonbudget concession was to accept additional work requirements for some federal benefits. The primary effect of work requirements, with their often onerous administrative burdens, will be to push people off these programs. This might be welcome, if you would prefer that they not exist in their current form at all. But it’s a surprising concession from an administration that, not long ago, was pushing in the other direction.

In a bigger sense this change directly repudiates one of the main social-policy lessons of recent years. Pandemic income-support programs were an extraordinary demonstration of the value of simple, universal social insurance programs, compared with narrowly targeted ones. The expiration of pandemic unemployment benefits gave us the cleanest test we are ever likely to see of the effect of social insurance and employment. States that ended pandemic benefits early did not see any faster job growth than ones that kept it longer – despite the fact that these programs gave their recipients far stronger incentives against work than those targeted in the budget deal.

These compromises are all the more disappointing since there were routes around the debt ceiling that the administration, for whatever reason, chose not to explore. The platinum coin got a healthy share of attention. But there were plenty of others.

The Treasury Department, for example, could have looked into selling debt at a premium. The debt ceiling binds the face value, or principal, of federal debt. There is no reason that this has to be equal to the amount the debt sells for – this is simply how auctions are currently structured. For much of U.S. history, government debt was sold at a discount or premium to its face value. Fixing an above-market interest rate and selling debt at more than face value would allow more funds to be raised without exceeding the debt ceiling.

The administration might also have asked the Federal Reserve to prepay future remittances. In most years, the Fed makes a profit, which it remits to the Treasury. But it can also report a loss, as it has since September. When that happens, the Fed simply creates new reserves to make up the shortfall, offsetting these with a “deferred asset” representing future remittances. (Currently, the Fed is carrying a deferred asset of $62 billion.) The same device could be used to finance public spending without issuing debt. Ina report a decade ago, Fed staff suggested that deferred assets could be used in this way to give the Treasury department “more breathing room under the debt ceiling.” (To be clear, they were not saying that this was a good idea, just noting the possibility.)

Another route around the debt ceiling might come from the fact that about one-fifth of the federal debt – some $6 trillion – is held by federal trust funds like Social Security, rather than by the public. (Another $5 trillion is held by the Federal Reserve.) This debt has no economic function. It is a bookkeeping device reflecting the fact that trust fund contributions to date have been higher than payments. Retiring these bonds, or replacing them with other instruments that wouldn’t count against the ceiling, would have no effect on either the government’s commitment to pay scheduled benefits or its ability to do so. But it would reduce the notional value of debt outstanding.

None of these options would be costless, risk-free, or even guaranteed to work. But there is little evidence they were seriously considered. This is a bit disheartening for supporters of the administration’s program. It’s hard to understand why you would go into negotiations with one hand tied behind your backs, and not have a plan B in case negotiations break down.

Tellingly, the one alternative the Biden team did consider was invoking the 14th Amendment to justify issuing new debt in defiance of the ceiling. The amendment refers specifically to the federal government’s debt obligations. But of course, hitting the debt ceiling would not only endanger the government’s debt service. It would threaten all kinds of payments that are legally mandated and economically vital. The openness to the 14th Amendment route, consistent with other public statements, suggests that decision-makers in the administration saw the overriding goal as protecting the financial system from the consequences of a debt default – as opposed to protecting the whole range of public payments.

What looks like a myopic focus on the dangers to banks recalls one of the worst failures of the Obama administration.

In the wake of the collapse of the housing market, Congress in 2009 authorized $46 billion in assistance for homeowners facing foreclosure through the Home Affordable Modification Program. But the Obama administration spent just a small fraction of this money (less than 3%) in the program’s first two years, helping only a small fraction of the number of homeowners originally promised.

The failure to help homeowners was not due to callousness or incompetence. Rather, it was due to the overriding priority put on the stability of the banking system. As Obama’s Treasury Secretary Timothy Geithner later explained, they saw the primary purpose of HAMP not as assisting homeowners, but as a way to “foam the runway” for a financial system facing ongoing mortgage losses.

Geithner and company weren’t wrong to see shoring up the banks as important. The problem was that this was allowed to take absolute priority over all other goals — with the result that millions of families lost their homes, an important factor in the slow growth of much of the 2010s.

One wouldn’t want to push this analogy too far. The debt ceiling deal is not nearly as consequential – or as clear a reflection of administration priorities – as the abandonment of underwater homeowners was. But it does suggest similar blinders: too much attention to the danger of financial crisis on one side, not enough to equally grave threats from other directions.

It’s clear that Treasury Secretary Janet Yellen and the rest of the Biden administration are very attuned to the dangers of a default. But have they given enough thought to the other dangers of failing to reach a debt-ceiling deal — or of reaching a bad one? Financial crises are not the only crises. There are many ways that an economy can break down.

Last week, my Roosevelt colleague Mike Konczal said on twitter that he endorsed the Fed’s decision to raise the federal funds rate, and the larger goal of using higher interest rates to weaken demand and slow growth. Mike is a very sharp guy, and I generally agree with him on almost everything. But in this case I disagree.

The disagreement may partly be about the current state of the economy. I personally don’t think the inflation we’re seeing reflects any general “overheating.” I don’t think there’s any meaningful sense in which current employment and wage growth are too fast, and should be slower. But at the end of the day, I don’t think Mike’s and my views are very different on this. The real issue is not the current state of the economy, but how much confidence we have in the Fed to manage it.

So: Should the Fed be raising rates to control inflation? The fact that inflation is currently high is not, in itself, evidence that conventional monetary policy is the right tool for bringing it down. The question we should be asking, in my opinion, is not, “how many basis points should the Fed raise rates this year?” It is, how conventional monetary policy affects inflation at all, at what cost, and whether it is the right tool for the job. And if not, what should we be doing instead?

What Do Rate Hikes Do?

AtPowell’s press conference, Chris Rugaber of the AP asked an excellent question: What is the mechanism by which a higher federal funds rate is supposed to bring down inflation, if not by raising unemployment?1 Powell’s answer was admirably frank: “There is a very, very tight labor market, tight to an unhealthy level. Our tools work as you describe … if you were moving down the number of job openings, you would have less upward pressure on wages, less of a labor shortage.”

Powell is clear about what he is trying to do. If you make it hard for businesses to borrow, some will invest less, leading to less demand for labor, weakening workers’ bargaining power and forcing them to accept lower wages (which presumably get passed on to prices, tho he didn’t spell that step out.) If you endorse today’s rate hikes, and the further tightening it implies, you are endorsing the reasoning behind it: labor markets are too tight, wages are rising too quickly, workers have too many options, and we need to shift bargaining power back toward the bosses.

Rather than asking exactly how fast the Fed should be trying to raise unemployment and slow wage growth, we should be asking whether this is the only way to control inflation; whether it will in fact control inflation; and whether the Fed can even bring about these outcomes in the first place.

Both hiring and pricing decisions are made by private businesses (or, in a small number of cases, in decentralized auction markets.) The Fed can’t tell them what to do. What it can do – what it is doing – is raise the overnight lending rate between banks, and sell off some part of the mortgage-backed securities and long-dated Treasury bonds that it currently holds.

A higher federal funds rate will eventually get passed on to other interest rates, and also (and perhaps more importantly) to credit conditions in general — loan standards and so on. Some parts of the financial system are more responsive to the federal funds rate than others. Some businesses and activities are more dependent on credit than others.

Higher rates and higher lending standards will, eventually, discourage borrowing. More quickly and reliably, they will raise debt service costs for households, businesses and governments, reducing disposable income. This is probably the most direct effect of rate hikes. It still depends on the degree to which market rates are linked to the policy rate set by the Fed, which in practice they may not be. But if we are looking for predictable results of a rate hike, higher debt service costs are one of the best candidates. Monetary tightening may or may not have a big effect on unemployment, inflation or home prices, but it’s certainly going to raise mortgage payments — indeed, the rise in mortgage rates we’ve seen in recent months presumably is to some degree in anticipation of rate hikes.

Higher debt service costs reduce disposable income for households and retained earnings for business, reducing consumption and investment spending respectively. If they rise far enough, they will also lead to an increase in defaults on debt.

(As an aside, it’s worth noting that a significant and rising part of recent inflation is owners’ equivalent rent, which is a BLS estimate of how much homeowners could hypothetically get if they rented out their homes. It is not a price paid by anyone. Meanwhile, mortgage payments, which are the main actual housing cost for homeowners, are not included in the CPI. It’s a bit ironic that in response to a rise in a component of “housing costs” that is not actually a cost to anyone, the Fed is taking steps to raise what actually is the biggest component of housing costs.)

Finally, a rate hike may cause financial assets to fall in value — not slowly, not predictably, but eventually. This is the intended effect of the asset sales.

Asset prices are very far from a simple matter of supply and demand — there’s no reason to think that a small sale of, say 10-year bonds will have any discernible effect on the corresponding yield (unless the Fed announces a target for the yield, in which case the sale itself would be unnecessary.) But again, eventually, sufficient rate hikes and asset sales will presumably lead asset prices to fall. When they do fall, it will probably by a lot at once rather than a little at a time – when assets are held primarily for capital gains, their price can continue rising or fall sharply, but it cannot remain constant. If you own something because you think it will rise in value, then if it stays at the current price, the current price is too high.

Lower asset values in turn will discourage new borrowing (by weakening bank balance sheets, and raising bond yields) and reduce the net worth of households (and also of nonprofits and pension funds and the like), reducing their spending. High stock prices are often a major factor in periods of rising consumption,like the 1990s; a stock market crash could be expected to have the opposite impact.

What can we say about all these channels? First, they will over time lead to less spending in the economy, lower incomes, and less employment. This is how hikes have an effect on inflation, if they do. There is no causal pathway from rate hikes to lower inflation that doesn’t pass through reduced incomes and spending along the way. And whether or not you accept the textbook view that the path from demand to prices runs via unemployment wage growth, it is still the case that reduced output implies less demand for labor, meaning slower growth in employment and wages.

That is the first big point. There is no immaculate disinflation.

Second, rate hikes will have a disproportionate effect on certain parts of the economy. The decline in output, incomes and employment will initially come in the most interest-sensitive parts of the economy — construction especially. Rising rates will reduce wealth and income for indebted households. 2. Over time, this will cause further falls in income and employment in the sectors where these households reduce spending, as well as in whatever categories of spending that are most sensitive to changes in wealth. In some cases, like autos, these may be the same areas where supply constraints have been a problem. But there’s no reason to think this will be the case in general.

It’s important to stress that this is not a new problem. One of the things hindering a rational discussion of inflation policy, it seems to me, is the false dichotomy that either we were facing transitory, pandemic-related inflation, or else the textbook model of monetary policy is correct. But as the BIS’s Claudio Borio and coauthors notein a recent article, even before the pandemic, “measured inflation [was] largely the result of idiosyncratic (relative) price changes… not what the theoretical definition of inflation is intended to capture, i.e. a generalised increase in prices.” The effects of monetary policy, meanwhile, “operate through a remarkably narrow set of prices, concentrated mainly in the more cyclically sensitive service sectors.”

These are broadly similar results to a2019 paper by Stock and Watson, which finds that only a minority of prices show a consistent correlation with measures of cyclical activity.3 It’s true that in recent months, inflation has not been driven by auto prices specifically. But it doesn’t follow that we’re now seeing all prices rising together. In particular, non-housing services (which make up about 30 percent of the CPI basket) are still contributing almost nothing to the excess inflation. Yet, if you believe the BIS results (which seem plausible), it’s these services where the effects of tightening will be felt most.

This shows the contribution to annualized inflation above the 2% target, over rolling three-month periods. My analysis of CPI data.

The third point is that all of this takes time. It is true that some asset prices and market interest rates may move as soon as the Fed funds rate changes — or even in advance of the actual change, as with mortgage rates this year. But the translation from this to real activity is much slower. The Fed’s ownFRB/US model says that the peak effect of a rate change comes about two years later; there are significant effects out to the fourth year. What the Fed is doing now is, in an important sense, setting policy for the year 2024 or 2025. How confident should we be about what demand conditions will look like then? Given how few people predicted current inflation, I would say: not very confident.

This connects to the fourth point, which is that there is no reason to think that the Fed can deliver a smooth, incremental deceleration of demand. (Assuming we agreed that that’s what’s called for.) In part this is because of the lags just mentioned. The effects of tightening are felt years in the future, but the Fed only gets data in real time. The Fed may feel they’ve done enough once they see unemployment start to rise. But by that point, they’ll have baked several more years of rising unemployment into the economy. It’s quite possible that by the time the full effects of the current round of tightening are felt, the US economy will be entering a recession.

This is reinforced when we think about the channels policy actually works through. Empirical studies of investment spending tend to find that it is actually quite insensitive to interest rates. The effect of hikes, when it comes, is likelier to be through Minskyan channels — at some point, rising debt service costs and falling asset values lead to a cascading chain of defaults.

In and Out of the Corridor

A broader reason we should doubt that the Fed can deliver a glide path to slower growth is that the economy is a complex system, with both positive and negative feedbacks; which feedbacks dominate depends on the scale of the disturbance. In practice, small disturbances are often self-correcting; to have any effect, a shock has to be big enough to overcome this homeostasis.

Axel Leijonhufvudlong ago described this as a “corridor of stability”: economic units have buffers in the form of liquid assets and unused borrowing capacity, which allow them to avoid adjusting expenditure in response to small changes in income or costs. This means the Keynesian multiplier is small or zero for small changes in autonomous demand. But once buffers start to get exhausted, responses become much larger, as the income-expenditure positive feedback loop kicks in.

The most obvious sign of this is the saw-tooth pattern in long-run series of employment and output. We don’t see smooth variation in growth rates around a trend. Rather, we see two distinct regimes: extended periods of steady output and employment growth, interrupted by shorter periods of negative growth. Real economies experience well-defined expansions and recessions, not generic “fluctuations”.

This pattern is discussed in a very interesting recent paper by Antonio Fatas,“The Elusive State of Full Employment.” The central observation of the paper is that whether you measure labor market slack by the conventional unemployment rate or in some other way (the detrended prime-age employment-population ratio is his preferred measure), the postwar US does not show any sign of convergence back to a state of full employment. Rather, unemployment falls and employment rises at a more or less constant rate over an expansion, until it abruptly gives way to a recession. There are no extended periods in which (un)employment rates remain stable.

One implication of this is that the economy spends very little time at potential or full employment; indeed, as he says, the historical pattern should raise questions whether a level of full employment is meaningful at all.

the results of this paper also cast doubt on the empirical relevance of the concepts of full employment or the natural rate of unemployment. … If this interpretation is correct, our estimates of the natural rate of unemployment are influenced by the length of expansions. As an example, if the global pandemic had happened in 2017 when unemployment was around 4.5%, it is very likely that we would be thinking of unemployment rates as low as 3.5% as unachievable.

There are many ways of arriving at this same point. For example, he finds that the (un)employment rate at the end of an expansion is strongly predicted by the rate at the beginning, suggesting that what we are seeing is not convergence back to an equilibrium but simply a process of rising employment that continues until something ends it.

Another way of looking at this pattern is that any negative shock large enough to significantly slow growth will send it into reverse — that, in effect, growth has a “stall speed” below which it turns into recession. If this weren’t the case, we would sometimes see plateaus or gentle hills in the employment rate. But all we see are sharp peaks.

In short: Monetary policy is an anti-inflation tool that works, when it does, by lowering employment and wages; by reducing spending in a few interest-sensitive sectors of the economy, which may have little overlap with those where prices are rising; whose main effects take longer to be felt than we can reasonably predict demand conditions; and that is more likely to provoke a sharp downturn than a gradual deceleration.

Is Macroeconomic Policy the Responsibility of the Fed?

One reason I don’t think we should be endorsing this move is that we shouldn’t be endorsing the premise that the US is facing dangerously overheated labor markets. But the bigger reason is that conventional monetary policy is a bad way of managing the economy, and entails a bad way of thinking about the economy. We should not buy into a framework in which problems of rising prices or slow growth or high unemployment get reduced to “what should the federal funds rate do?”

What’s missing here is any policy action by anyone other than the Fed. It’s this narrowing of the discussion I object to, more than the rate increase as such.

Rents are rising rapidly right now — at an annual rate of about 6 percent as measured by the CPI. And there is reason to think that this number understates the increase in market rents and will go up rather than down over the coming year. This is one factor in the acceleration of inflation compared with 2020, when rents in most of the country were flat or falling. (Rents fell almost 10 percent in NYC during 2020, perZillow.) The shift from falling to rising rents is an important fact about the current situation. But rents were also rising well above 2 percent annually prior to the pandemic. The reason that rents (and housing prices generally) rise faster than most other prices generally, is that we don’t build enough housing. We don’t build enough housing for poor people because it’s not profitable to do so; we don’t build enough housing for anyone in major cities because land-use rules prevent it.

Rising rents are not an inflation problem, they are a housing problem. The only way to deal with them is some mix of public money for lower-income housing, land-use reform, and rent regulations to protect tenants in the meantime. Higher interest rates will not help at all — except insofar as, eventually, they make people too poor to afford homes.

Or energy costs. Energy today still mostly means fossil fuels, especially at the margin. Both supply and demand are inelastic, so prices are subject to large swings. It’s a global market, so there’s not much chance of insulating the US even if it is “energy independent” in net terms. The geopolitics of fossil fuels means that production is both vulnerable to interruption from unpredictable political developments, and subject to control by cartels.

The long run solution is, of course, to transition as quickly as possible away from fossil fuels. In the short run, we can’t do much to reduce the cost of gasoline (or home heating oil and so on), but we can shelter people from the impact, by reducing the costs of alternatives, like transit, or simply by sending them checks. (The California state legislature’s plan seems like a good model.) Free bus service will help both with the short-term effect on household budgets and to reduce energy demand in the long run. Raising interest rates won’t help at all — except insofar as, eventually, they make people too poor to buy gas.

These are hard problems. Land use decisions are made across tens of thousands of local governments, and changes are ferociously opposed by politically potent local homeowners (and some progressives). Dependence on oil is deeply baked into our economy. And of course any substantial increase in federal spending must overcome both entrenched opposition and the convoluted, anti-democratic structures of our government, as we have all been learning (again) this past year.

These daunting problems disappear when we fold everything into a price index and hand it over to the Fed to manage. Reducing everything to the core CPI and a policy rule are a way of evading all sorts of difficult political and intellectual challenges. We can also then ignore the question how, exactly, inflation will be brought down without costs to the real economy, and how to decide if these costs are worth it. Over here is inflation; over there are the maestros with their magic anti-inflation device. All they have to do is put the right number into the machine.

It’s an appealing fantasy – it’s easy to see why people are drawn to it. But it is a fantasy.

A modern central bank, sitting at the apex of the financial system, has a great deal of influence over markets for financial assets and credit. This in turn allows it to exert some influence — powerful if often slow and indirect — on production and consumption decisions of businesses and households. Changes in the level and direction of spending will in turn affect the pricing decisions of business. These effects are real. But they are no different than the effects of anything else — public policy or economic developments — that influence spending decisions. And the level of spending is in turn only one factor in the evolution of prices. There is no special link from monetary policy to aggregate demand or inflation. It’s just one factor among others — sometimes important, often not.

Yes, a higher interest rate will, eventually reduce spending, wages and prices. But many other forces are pushing in other directions, and dampening or amplifying the effect of interest rate changes. The idea that there is out there some “r*”, some “neutral rate” that somehow corresponds to the true inter temporal interest rate — that is a fairy tale.

Nor does the Fed have any special responsibility for inflation. Once we recognize monetary policy for what it is — one among many regulatory and tax actions that influence economic rewards and incomes, perhaps influencing behavior — arguments for central bank independence evaporate. (Then again, theydid not make much sense to begin with.) And contrary to widely held belief, the Fed’s governing statutes do not give it legal responsibility for inflation or unemployment.

That last statement might sound strange, given that we are used to talking about the Fed’s dual mandate. But as Lev Menand points out in an important recent intervention, the legal mandate of the Fed has been widely misunderstood. What the Federal Reserve Act charges the Fed with is

maintain[ing the] long run growth of the monetary and credit aggregates commensurate with the economy’s long-run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

There are two things to notice here. First, the bolded phrase: The Fed’s mandate is not to maintain price stability or full employment as such. It is to prevent developments in the financial system that interfere with them. This is not the same thing. And as Menand argues (in the blog post and at more lengthelsewhere), limiting the Fed’s macroeconomic role to this narrower mission was the explicit intent of the lawmakers who wrote the Fed’s governing statutes from the 1930s onward.

Second, price stability, maximum employment and moderate interest rates (an often forgotten part of the Fed’s mandate) are not presented as independent objectives, but as the expected consequences of keeping credit growth on a steady path. As Menand writes:

The Fed’s job, as policymakers then recognized, was not to combat inflation—it was to ensure that banks create enough money and credit to keep the nation’s productive resources fully utilized…

This distinction is important because there are many reasons that, in the short-to-medium term, the economy might not achieve full potential—as manifested by maximum employment, price stability, and moderate long-term interest rates. And often these reasons have nothing to do with monetary expansion, the only variable Congress expected the Fed to control. For example, supply shortages of key goods and services can cause prices to rise for months or even years while producers adapt to satisfy changing market demand. The Fed’s job is not to stop these price rises—even if policymakers might think stopping them is desirable—just as the Fed’s job is not to … lend lots of money to companies so that they can hire more workers. The Fed’s job is to ensure that a lack of money and credit created by the banking system—an inelastic money supply—does not prevent the economy from achieving these goals. That is its sole mandate.

As Menand notes, the idea that the Fed was directly responsible for macroeconomic outcomes was a new development in the 1980s, an aspect of the broader neoliberal turn that had no basis in law. Nor does it have any good basis in economics. If a financial crisis leads to a credit crunch, or credit-fueled speculation develops into an asset bubble, the central bank can and should take steps to stabilize credit growth and asset prices. In doing so, it will contribute to the stability of the real economy. But when inflation or unemployment come from other sources, conventional monetary policy is a clumsy, ineffectual and often destructive way of responding to them.

There’s a reason that the rightward turn in the 1980s saw the elevation of central banks as the sole custodians of macroeconomic stability. The economies we live in are not in fact self-regulating; they are subject to catastrophic breakdowns of various forms, and even when they function well, are in constant friction with their social surroundings. They require active management. But routine management of the economy — even if limited to the adjustment of the demand “thermostat,” in Samuelson’s old metaphor — both undermine the claim that markets are natural, spontaneous and decentralized, and opens the door to a broader politicization of the economy. The independent central bank in effect quarantines the necessary economic management from the infection of democratic politics.

The period between the 1980s and the global financial crisis saw both a dramatic elevation of the central bank’s role in macroeconomic policy, and a systematic forgetting of the wide range of tools central banks used historically. There is a basic conflict between the expansive conception of the central bank’s responsibilities and the narrow definition of what it actually does. The textbooks tell us that monetary policy is the sole, or at least primary, tool for managing output, employment and inflation (and in much of the world, the exchange rate); and that it is limited to setting a single overnight interest rate according to a predetermined rule. These two ideas can coexist comfortably only in periods of tranquility when the central bank doesn’t actually have to do anything.

What has the Fed Delivered in the Past?

Coming back to the present: The reason I think it is wrong to endorse the Fed’s move toward tightening is not that there’s any great social benefit to having an overnight rate on interbank loans of near 0. I don’t especially care whether the federal funds rate is at 0.38 percent or 1.17 percent next September. I don’t think it makes much difference either way. What I care about is endorsing a framework that commits us to managing inflation by forcing down wages, one that closes off discussion of more progressive and humane — and effective! — ways of controlling inflation. Once the discussion of macroeconomic policy is reduced to what path the federal funds rate should follow, our side has already lost, whatever the answer turns out to be.

It is true that there are important differences between the current situation the end of 2015, the last time the Fed started hiking, that make today’s tightening more defensible. Headline unemployment is now at 3.8 percent, compared with 5 percent when the Fed began hiking in 2015. The prime-age employment rate was also about a point lower then than now. But note also that in 2015 the Fedthought the long-run unemployment rate was 4.9 percent. So from their point of view, we were at full employment. (The CBO, which had the long-run rate at 5.3 percent, thought we’d already passed it.) It may be obvious in retrospect (and to some of us in the moment) that in late 2015 there was still plenty of space for continued employment growth. But policymakers did not think so at the time.

More to the point, inflation then was much lower. If inflation control is the Fed’s job, then the case for raising rates is indeed much stronger now than it was in December 2015. And while I am challenging the idea that this should be the Fed’s job, most people believe that it is. I’m not upset or disappointed that Powell is moving to hike rates now, or is justifying it in the way that he is. Anyone who could plausibly be in that position would be doing the same.

So let’s say a turn toward higher rates was less justified in 2015 than it is today. Did it matter? If you look at employment growth over the 2010s, it’s a perfectly straight line — an annual rate of 1.2 percent, month after month after month. If you just looked at the employment numbers, you’d have no idea that the the Fed was tightening over 2016-2018, and then loosening in the second half of 2019. This doesn’t, strictly speaking, prove that the tightening had no effect. But that’s certainly the view favored by Occam’s razor. The Fed, fortunately, did not tighten enough to tip the economy into recession. So it might as well not have tightened at all.

The problem in 2015, or 2013, or 2011, the reason we had such a long and costly jobless recovery, was not that someone at the Fed put the wrong parameter into their model. It was not that the Fed made the wrong choices. It was that the Fed did not have the tools for the job.

Honestly, it’s hard for me to see how anyone who’s been in these debates over the past decade could believe that the Fed has the ability to steer demand in any reliable way. The policy rate was at zero for six full years. The Fed was trying their best! Certainly the Fed’s response to the 2008 crisis was much better than the fiscal authorities’. So for that matter was the ECB’s, once Draghi took over from Trichet. 4 The problem was not that the central bankers weren’t trying. The problem was that having the foot all the way down on the monetary gas pedal turned out not to do much.

As far as I can tell, modern US history offers exactly one unambiguous case of successful inflation control via monetary policy: the Volcker shock. And there, it was part of a comprehensive attack on labor.

It is true that recessions since then have consistently seen a fall in inflation, and have consistently been preceded by monetary tightenings. So you could argue that the Fed has had some inflation-control successes since the 1980s, albeit at the cost of recessions. Let’s be clear about what this entails. To say that the Fed was responsible for the fall in inflation over 2000-2002, is to say that the dot-com boom could have continued indefinitely if the Fed had not raised rates.

Maybe it could have, maybe not. But whether or not you want to credit (or blame) the Fed for some or all of the three pre-pandemic recessions, what is clear is that there are few if any cases of the Fed delivering slower growth and lower inflation without a recession.

According to Alan Blinder, since World War II the Fed has achieved a soft landing in exactly two out of 11 tightening cycles, most recently in 1994. In that case, it’s true, higher rates were not followed by a recession. But nor were they followed by any discernible slowdown in growth. Output and employment grew even faster after the Fed started tightening than before. As for inflation, it did come down about two years later, at the end of 1996 – at exactly the same moment as oil prices peaked. And came back up in 1999, at exactly the moment when oil prices started rising again. Did the Fed do that? It looks to me more like 2015 – a tightening that stopped in time to avoid triggering a recession, and instead had no effect. But even if we accept the 1994 case, that’s one success story in the past 50 years. (Blinder’s other soft landing is 1966.)

I think the heart of my disagreement with progressives who are support tightening is whether it’s reasonable to think the Fed can adjust the “angle of approach” to a higher level of employment. I don’t think history gives us much reason to believe that they can. There are people who think that a recession, or at least a much weaker labor market, is the necessary cost of restoring price stability. That’s not a view I share, obviously, but it is intellectually coherent. The view that the Fed can engineer a gentle cooling that will bring down inflation while employment keeps rising, on the other hand, seems like wishful thinking.

That said, of the two realistic outcomes of tightening – no effect, or else a crisis – I think the first is more likely, unless they move quite a bit faster than they are right now.

So what’s at stake then? If the Fed is doing what anyone in their position would do, and if it’s not likely to have much impact one way or another, why not make some approving noises, bank the respectability points, and move on?

Four Good Reasons to Be Against Rate Hikes (and One that Isn’t)

I think that it’s a mistake to endorse or support monetary tightening. I’ll end this long post by summarizing my reasons. But first, let me stress that a commitment to keeping the federal funds rate at 0 is not one of those reasons. If the Fed were to set the overnight rate at some moderate positive level and then leave it there, I’d have no objection. In the mid-19th century, the Bank of France kept its discount rate at exactly 4 percent for something like 25 years. Admittedly 4 percent sounds a little high for the US today. But a fixed 2 percent for the next 25 years would probably be fine.

There are four reasons I think endorsing the Fed’s decision to hike is a mistake.

First, most obviously, there is the risk of recession. If rates were at 2 percent today, I would not be calling for them to be cut. But raising them is a different story. Last week’s hike is no big deal in itself, but there will be another, and another, and another. I don’t know where the tipping point is, where hikes inflict enough financial distress to tip the economy into recession. But neither does the Fed. The faster they go, the sooner they’ll hit it. And given the long lags in monetary transmission, they probably won’t know until it’s too late. People are talking a lot lately about wage-price spirals, but that is far from the only positive feedback in a capitalist economy. Once a downturn gets started, with widespread business failures, defaults and disappointed investment plans, it’s much harder to reverse it than it would have been to maintain growth.

I think many people see trusting the Fed to deal with inflation as the safe, cautious position. But the fact that a view is widely held doesn’t mean it is reasonable. It seems to me that counting on the Fed to pull off something that they’ve seldom if ever succeeded at before is not safe or cautious at all.5 Those of us who’ve been critical of rate hikes in the past should not be too quick to jump on the bandwagon now. There are plenty of voices calling on the Fed to move faster. It’s important that there also be some saying, slow down.

2. Second, related to this, is a question I think anyone inclined to applaud hikes should be asking themselves: If high inflation means we need slower growth, higher unemployment and lower wages, where does that stop? Inflation may come down on its own over the next year — I still think this is more likely than not. But if it doesn’t come down on its own, the current round of rate hikes certainly isn’t going to do it. Looking again at the Fed’s FRB/US model, we see that a one point increase in the federal funds rate is predicted to reduce inflation by about one-tenth of a point after one year, and about 0.15 points after two years. The OECD’s benchmark macro model make similar predictions: a sustained one-point increase in the interest rate in a given year leads to an 0.1 point fall in inflation the following year, an 0.3 fall in the third year and and an 0.5 point fall in the fourth year.

Depending which index you prefer, inflation is now between 3 and 6 points above target.6 If you think conventional monetary policy is what’s going to fix that, then either you must have have some reason to think its effects are much bigger than the Fed’s own models predict, or you must be imagining much bigger hikes than what we’re currently seeing. If you’re a progressive signing on to today’s hikes, you need to ask yourself if you will be on board with much bigger hikes if inflation stays high. “I hope it doesn’t come to that” is not an answer.

3. Third, embracing rate hikes validates the narrative that inflation is now a matter of generalized overheating, and that the solution has to be some form of across-the-board reduction in spending, income and wages. It reinforces the idea that pandemic-era macro policy has been a story of errors, rather than, on balance, a resounding success.

The orthodox view is that low unemployment, rising wages, and stronger bargaining power for workers are in themselves serious problems that need to be fixed. Look at how the news earlier this week of record-low unemployment claims got covered: It’s a dangerous sign of “wage inflation” that will “raise red flags at the Fed.” Or the constant complaints by employers of “labor shortages” (echoed by Powell last week.) Saying that we want more employment and wage growth, just not right now, feels like trying to split the baby. There is not a path to a higher labor share that won’t upset business owners.

The orthodox view is that a big reason inflation was so intractable in the 1970s was that workers were also getting large raises. From this point of view, if wages are keeping pace with inflation, that makes the problem worse, and implies we need even more tightening. Conversely, if wages are falling behind, that’s good. Alternatively, you might think that the Powell was right before when he said the Phillips curve was flat, and that inflation today has little connection with unemployment and wages. In that case faster wage growth, so that living standards don’t fall, is part of the solution not the problem. Would higher wages right now be good, or bad? This is not a question on which you can be agnostic, or split the difference. I think anyone with broadly pro-worker politics needs to think very carefully before they accept the narrative of a wage-price spiral as the one thing to be avoided at all costs.