TLDR: The value of corporate equity relative to GDP is at a historical high. But this does not necessarily mean there’s a bubble: profits and shareholder payouts are also very high relative to historical values.

I first started thinking about economics thirty years ago, during the (first) tech boom.

This was the era of “irrational exuberance,” the phrase coined by the recently deceased Alan Greenspan and made famous by Robert Shiller. I wrote a review of Shiller’s book of that title for In These Times — one of my first published articles. My first paper in graduate school was a replication of a paper by Brad DeLong and Larry Summers1, which argued that seemingly excessive stock valuations could be explained by rational investors extrapolating recent earnings growth into the future.

All of which is seeming at least a little bit relevant today.

Between the start of 1995 and the end of 1999, the price-earnings ratio for the S&P 500, as measured by Shiller, more than doubled, from 20 to nearly 44. Then over the next three years, it fell back nearly as far. Today, price-earnings ratios by the same metric are just shy of 40, not far from the peak of the first tech boom. Everything old is new again, it seems. (Except that, as Paul Krugman notes, people generally liked the products of the first internet companies.) So the obvious question is whether this is also a bubble — whether the second half of the late-1990s story will get a rerun as well.

There are many people out there with highly specialized expertise whose whole job is to think about stock valuations. I am not one of those people! If you are looking for investment advice, you have come to the wrong blog.

But I do think I have something to add.

Most of what makes financial-analyst jobs hard has to do with specific companies and specific markets. Things get easier when we are looking at the stock market as a whole. (And that is where my own background in heterodox macro is more likely to help.) When we are talking about corporate equity in the aggregate, rather than individual securities, some arithmetic comes into play that helpfully limits the space of possibilities.

One way to think of a share is that it gives a claim on future payments by the corporation that issued it. This is not all that a share is — as Arjun and I stress in Against Money, it’s important to keep sight of financial assets’ existence as concrete objects with their own specific properties, and not reduce them to simply a future cashflow. But certainly the cashflow it gives claim to is one very important property of a share.

Again, the value of share is not reducible to present value of expected (in either the statistical and/or psychological sense) future payments. But those should act as an anchor. Unless we have good reason to think there is a change on value market participants put on future payments, we should expect share prices to vary roughly in proportion to them. And even if we think valuation of shares can vary indefinitely with respect to payments they give claim to, it’s worth knowing how much of current share prices would have to be explained in these terms, and how much can be explained by variation in the payments.

In the rest of this post, I am going to look at the US nonfinancial corporate sector. This means excluding the 20-25% of corporate equity issued by financial businesses, and including closely-held corporations as well as those listed on public exchanges. This is mainly because that’s the universe for which it’s easiest to get consistent data. But I also think it’s a reasonable thing to be interested in substantively.

*

If we look at nonfinancial corporate equity over the 80 years since World War II, here is what we see:

The figure shows the total value of nonfinancial corporate equity,as a share of potential GDP. (I am skeptical of potential as a measure of actual economic potential, but here it is just functioning as a trend, to smooth out short-term changes in the denominator.) This, I would argue, is the most straightforward measure of the value of the stock market in broad social terms — how much claim wealth in this form gives on social labor and its products. This is also, of course, the metric used by Piketty.

As the figure shows, stock market value in that sense has had three long upswings. The first peaked in the late 1960s at 0.9, the second in 2000 at 1.6, and the third is ongoing, with the ratio currently at 2.3. (The data in this post is drawn from the Fed’s Financial Accounts, and goes through the first quarter of 2026.) Over the long run, there is a clear upward trend, especially over the past 15 years. (The dotted line shows the post-WWII average.) By this metric, the current stock market boom has now run well ahead of the late 1990s one.

How should we think about this?

Logically, the value of corporate equity relative to GDP must reflect a combination of four factors: value added in the corporate sector as a share of GDP; corporate profits as a share of their value added; payouts to shareholders as a percentage of profits; and the value placed by markets on each dollar of payouts.

In other words, if corporate stock is worth more relative to GDP, that can be either because more of GDP is now happening in the corporate sector; or because more of the income from that activity is going to profits; or because more of those profits are being paid out to shareholders (rather than retained in the firm); or because financial markets place a greater value on each dollar of payment. Or of course some combination of those.

We can write this as an accounting identity:

equity/GDP = value added/GDP * profits/value added * payouts/profits * equity/payouts

As with any accounting identity applied historically, it is useful insofar as it corresponds to (1) categories in the relevant data, and (2) distinct causal factors we believe to be at work.

For the first term, we are, again, using all nonfinancial corporate equity, which includes closely held as well as publicly-traded corporations, and the BEA’s estimate of potential GDP. (Both are in current dollars.) Value added is defined, as usual, as sales less the cost of non-labor inputs. Profits are after tax (and of course also after depreciation); conceptually, these are the funds potentially available for distribution to shareholders.2

Payouts I am defining as dividends less net new equity issues. That share repurchases are conceptually equivalent to dividends is not, I think, too controversial at this point (though it creates a lot of headaches). We are also adding shares retired through cash acquisitions, and subtracting shares issued whether in IPOs or otherwise. This might seem odd at the level of an individual firm, but at the aggregate level these other flows seem clearly equivalent to buybacks and dividends. If firm A buys up all the shares in firm B for cash, that is a payment from the corporate sector to shareholders, just as if firm A were buying back its own shares. Similarly, new shares issued are a reduction in the aggregate payments from the corporate sector to shareholders just as a reduction in dividend payments would be.

It might sound strange to define IPOs (which generally are quite exciting for stock market participants) as equivalent to dividend reductions (which generally are not.) But this is where the aggregate perspective matters. Shareholders as a whole already own all the equity of the corporate sector as a whole. An IPO is a payment from shareholders to the corporate sector, exactly like buyback is a payment from the corporate sector to shareholders, without in either case any change in aggregate ownership rights. Or looking at it from another point of view, new corporations are in general competing with existing firms; the profits flowing out to shareholders of the new firm are to a first approximation deductions from the profits flowing to claimants on existing firms. Nice for the shareholders in the new firm, if it succeeds; but no use to shareholders as a class.

Finally, the valuation term asks, in effect, what is the market price of a dollar of income from the corporate sector. It’s analogous to the price-earnings or price-dividend ratios one sees at the level of individual corporations or indexes, though not identical given the nonstandard (but, I would argue, appropriate) way I have defined payouts. Here it also functions as the residual term, reflecting any change in the value of equity not explained by the other factors.

The figures below show the values of each of these terms over the past 80 years. What do we see?

We will start with the first term, corporate value added as a share of GDP. This shows how much of economic activity takes place in the corporate sector, and is potentially available for shareholders.

As it turns out, the corporate value added term does not do anything interesting. Yes, it is modestly lower (around 50 percent) after 2000 than its average in the earlier decades (53 percent), suggesting that all else equal, we might expect the value of corporate equity to be slightly lower relative to GDP in the 21st than in the 20th century. But this change is very small compared with the movements in the other terms. This factor might be important if we were comparing the US to other countries, but it is not part of the story here.

Next, profits:

Profits as a share of value added shows much more variation, falling by half in the 1980s, then rising in this century, in two big jumps — one after 2000 and the second over the past five or so years. While the corporate share of GDP doesn’t vary by even 10 percent over the whole period, profits as a share of value added are fully three times greater today than they were for much of the 1980s.

The third term is payouts.

Payouts (as I’ve defined them) also show large variation, rising from a bit under 40 percent of profits in the early decades to over 80 percent in more recent ones. The timing here is a bit different — though there is plenty of short-term variation, the long-run shift happens in a single big jump in the early 1980s. (This was the topic of an essay in my dissertation, which I never managed to publish as an academic article but did turn into a report for the Roosevelt Institute.) This term gets relatively little attention in discussion of stock prices, but it seems to me that it is as fundamental as profits to any discussion of long-term trends in the value of corporate equity.

Finally, the valuation term shows a lot of short- and medium-term variation but, perhaps surprisingly, no long run trend. Today’s ratio of around 40 is close to what we see in the 1950s and 1960s.

Again, what we are measuring with this last term is the ratio of equity value to shareholder payouts, including net share repurchases. The big spikes in the early 1970s and in 2000 are because those years saw exceptionally high new equity issues, which means very low payouts by my metric, and therefore very high ratios of equity value to payouts.

It is more common to talk about equity in relation to earnings, on the implicit assumption that profits are of equal value to shareholders whether they are paid out or not. I’ve shown this latter ratio below. But personally, I do not think that that is a good assumption. Shareholders evidently care a great deal about payouts — why else would companies pay dividends and make share repurchases? I think it is important to distinguish between corporations and the shareholders who exercise claims on them — the former are not simply the personal property of the latter. From this point of view, it is more natural to talk about valuation in terms of the price shareholders place on the income they actually get from corporations, as opposed to the underlying profits.

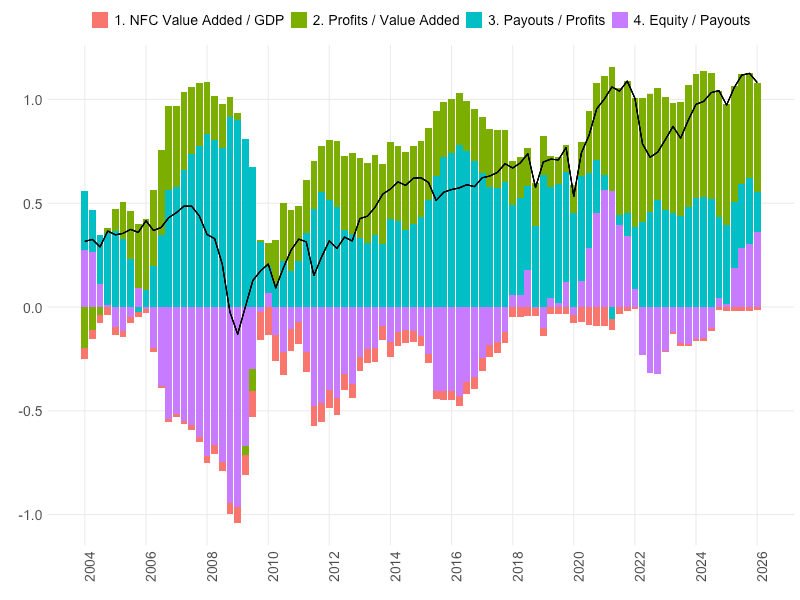

All of these series (except the last one) are combined in the next figure, which is really the whole point of this post. If you take one thing from one I’ve written here, this picture is it.

Equity value relative to GDP and its components, 1947-2026:

For this figure, I’ve converted the values to logs. This has the big advantage of converting the multiplicative relationship to an additive one, so that we can visually see the contribution made by each of them. But it can make interpreting the figure a bit tricky. Here, zero is the average value over the full period; positive one is a value about 2.7 times greater than the average, while negative one is a value about one-third of the average. The black line similarly describes the deviation of the equity-GDP ratio from its full-period average; the heights of the bars correspond to the contribution each term makes to that deviation. The data is quarterly; for all the terms except equity, I use rolling one-year averages.

As we can see, the log of the equity-GDP ratio is currently about 1.1 above its long-run average, corresponding to a value nearly three times greater. (2.2 today, versus a long run average of 0.85.) Just over half of this (0.53) is explained by higher profits relative to value added, 0.19 is explained by higher payouts relative to profits, and 0.36 is explained by the valuation term.

So already we can see that a simple explanation of today’s high equity values is going to be incomplete. Relative to the long-run average, we have three distinct factors each of which explains a significant share of today’s higher values.

Another thing that jumps out from the figure is that the previous historical peaks in equity values reflect quite different mixes of these components.

In the 1960s, profits as a share of value added were, for a while, well above average, though not as high as today; but the fraction of those profits flowing out to shareholders was much lower. Thus the much lower ratio of equity to GDP, despite comparable valuation ratios.

In the late 1990s, profits as a share of value added were much lower — less than 5 percent at the height of the tech bubble, compared with 10 percent in the 1960s and 15 percent today. But the fraction of profits paid out to shareholders was historically high, averaging over 100 percent for the 1998-2000 period. It’s worth noting in this context, also, that the collapse of equity value in the 1970s reflected a fall in shareholder payouts much more than in profitability; this is perhaps important context for the shareholder revolt that followed.

The big takeaway from this decomposition is that we should be cautious about assuming the stock market is overvalued — that we’re in a bubble, that this is another bout of irrational exuberance — simply because equity prices are high relative to the historical norm. Shareholders have it better than the historical norm, too. Corporations are more profitable. And more of those profits are flowing out to them. A bit of exuberance might be rational, under the circumstances.

On the other hand: If we focus on just the past 20 years, as in the figure below, the picture looks a bit different.

Yes, both profits and payouts are high relative to their long-run averages; but those shifts mostly came earlier, while the big rise in equity prices is more recent. Apart from the relatively brief collapse in profits during the Great Recession, almost all the variation in equity prices over the past two decades comes from the valuation term, rather than changes in the underlying payments to shareholders.

This is even more true over the past two years — equity values have increased sharply while profits have been stable and aggregate payments to shareholders have fallen, as dividend growth has stalled and net equity issue has turned positive. As a share of GDP, the net payments flowing from corporations to shareholders today are very close to where they were a decade ago; but corporate equity is worth 60 percent more. It’s hard to avoid the conclusion that either equity was undervalued in the mid-2010s, or it is overvalued now.

So which side do we focus on? Over the long run, most — tho not all — of the increase in the value of wealth in the form of corporate equity, is explained by what we might call fundamentals — the flow of payments to owners of that wealth. Over the short to medium run, on the other hand, almost all of the increase in the value of equity comes from valuation, and whatever financial-market dynamics drive that. Or as the old saying goes, in the short run the market is a voting machine, but in the long run it’s a weighing machine.

*

I want to say a bit more about the profits and payouts parts of the picture.

That high stock prices reflect to some extent a high level of corporate profits seems to be reasonably well understood, at least based on recent coverage in the Financial Times. This of course does not mean that high stock prices are justified, or sustainable; it just shifts the question to how justified or sustainable the high profits are.

This goes double to the extent that high valuations are based on an expectation of further increases in profits, as this recent FT piece suggests:

Wall Street’s expectations for company profit growth are rising at the fastest pace since the post-pandemic rebound, fuelling concern that an “earnings bubble” could be forming in the estimates that have underpinned the US stock market’s rally.

Analysts are now forecasting a 25 per cent increase in S&P 500 company earnings for the coming year, according to Bloomberg data, boosted by a resilient US economy and the AI boom.

However, just ahead of the second-quarter earnings season, some investors are growing concerned about the speed at which analysts’ estimates are rising…

This Alphaville piece goes further, saying that “supernormal profits are unsustainable, because they always are.” I don’t know about that. I don’t know if there’s any reason to think the profit share is stationary, to use the statistics jargon — apart from a dip in 2008-2009, profits as a share of value added have been greater than their long-run average in every year of this century, and seem to be getting farther from it. Capital really has won some lasting victories in the class war.

That is one natural way to look at profits — as a distributional variable. But there’s another way of looking at them, from the demand side.

We know, as readers of Keynes, that an increase in investment automatically creates an equal quantity of additional saving. If, furthermore, there’s little or no incremental saving out of wage income (a reasonable assumption, in my opinion) and if the fiscal balance and trade balance don’t change significantly (perhaps less reasonable, but we’ll go with it) then this additional saving must take the form of an increase in profits. This relationship is often known as the Kalecki-Levy profits identity, and is one bit of heterodox economics that has established a foothold in finance and the business press. The same identity says that an increase in the fiscal deficit or trade surplus should similarly lead to an equal increase in aggregate profits.

Exploring the math of this and the extent to which it is a reasonable first approximation of real-world dynamics would be an interesting exercise for another post. But it raises another point which I think is very relevant for thinking about the current situation: Even if the AI companies themselves are not particularly (or at all) profitable, AI-related investment spending is probably an important factor in raising aggregate profits. Just like the California gold rush generated plenty of profits for somebody, even if the vast majority of prospectors themselves went broke.

Or as this recent FT piece puts it:

The AI boom is lifting the fortunes of hundreds of formerly drab industrial, utility and mining companies as investors turn to the “picks and shovels” needed to build and power vast data centres. …

The companies benefiting include Caterpillar, best known for construction equipment but now supplying generators for data centres, 150-year-old German engineering company Hochtief, which will enter the Dax later this month, and Nucor, a steel supplier that has credited “white hot” AI demand for a “tsunami of earnings power”. …

The vast amounts of electricity needed for AI training are also fuelling demand for specialised power management, high-voltage electronics and cooling technologies. This has led to big interest in traditional suppliers of electrical equipment…

You could think of it like this: As long as there is strong investment demand and easy financing for it, the profits will be there …. but not necessarily for the companies carrying out the investment and getting the financing.

And this, perhaps, is the point where the macro perspective needs to give way to the micro one. Because it may be that, yes, in the aggregate, an ease in financing brings forth additional investment, which generates enough profits to justify the initial financing. But debt must be paid back not in the aggregate, but by the specific companies that incurred it. If the investment is one place and the profits are somewhere else, then at some point somebody’s survival constraint is going to be violated.

And I think I will end this post here.

I very much want to discuss the payouts piece of the equation, which in my mind is as important as profits, and much less discussed. But this post is already too long, and has taken much too long to write. So the payouts piece should be along, well, if not this month, then next month, or soon.