TLDR: The value of corporate equity relative to GDP is at a historical high. But this does not necessarily mean there’s a bubble: profits and shareholder payouts are also very high relative to historical values.

I first started thinking about economics thirty years ago, during the (first) tech boom.

This was the era of “irrational exuberance,” the phrase coined by the recently deceased Alan Greenspan and made famous by Robert Shiller. I wrote a review of Shiller’s book of that title for In These Times — one of my first published articles.My first paper in graduate school was a replication of a paper by Brad DeLong and Larry Summers1, which argued that seemingly excessive stock valuations could be explained by rational investors extrapolating recent earnings growth into the future.

All of which is seeming at least a little bit relevant today.

Between the start of 1995 and the end of 1999, the price-earnings ratio for the S&P 500, as measured by Shiller, more than doubled, from 20 to nearly 44. Then over the next three years, it fell back nearly as far. Today, price-earnings ratios by the same metric are just shy of 40, not far from the peak of the first tech boom. Everything old is new again, it seems. (Except that, as Paul Krugman notes, people generally liked the products of the first internet companies.) So the obvious question is whether this is also a bubble — whether the second half of the late-1990s story will get a rerun as well.

There are many people out there with highly specialized expertise whose whole job is to think about stock valuations. I am not one of those people! If you are looking for investment advice, you have come to the wrong blog.

But I do think I have something to add.

Most of what makes financial-analyst jobs hard has to do with specific companies and specific markets. Things get easier when we are looking at the stock market as a whole. (And that is where my own background in heterodox macro is more likely to help.) When we are talking about corporate equity in the aggregate, rather than individual securities, some arithmetic comes into play that helpfully limits the space of possibilities.

One way to think of a share is that it gives a claim on future payments by the corporation that issued it. This is not all that a share is — as Arjun and I stress in Against Money, it’s important to keep sight of financial assets’ existence as concrete objects with their own specific properties, and not reduce them to simply a future cashflow. But certainly the cashflow it gives claim to is one very important property of a share.

Again, the value of share is not reducible to present value of expected (in either the statistical and/or psychological sense) future payments. But those should act as an anchor. Unless we have good reason to think there is a change on value market participants put on future payments, we should expect share prices to vary roughly in proportion to them. And even if we think valuation of shares can vary indefinitely with respect to payments they give claim to, it’s worth knowing how much of current share prices would have to be explained in these terms, and how much can be explained by variation in the payments.

In the rest of this post, I am going to look at the US nonfinancial corporate sector. This means excluding the 20-25% of corporate equity issued by financial businesses, and including closely-held corporations as well as those listed on public exchanges. This is mainly because that’s the universe for which it’s easiest to get consistent data. But I also think it’s a reasonable thing to be interested in substantively.

*

If we look at nonfinancial corporate equity over the 80 years since World War II, here is what we see:

The figure shows the total value of nonfinancial corporate equity,as a share of potential GDP. (I am skeptical of potential as a measure of actual economic potential, but here it is just functioning as a trend, to smooth out short-term changes in the denominator.) This, I would argue, is the most straightforward measure of the value of the stock market in broad social terms — how much claim wealth in this form gives on social labor and its products.This is also, of course, the metric used by Piketty.

As the figure shows, stock market value in that sense has had three long upswings. The first peaked in the late 1960s at 0.9, the second in 2000 at 1.6, and the third is ongoing, with the ratio currently at 2.3. (The data in this post is drawn from the Fed’s Financial Accounts, and goes through the first quarter of 2026.) Over the long run, there is a clear upward trend, especially over the past 15 years. (The dotted line shows the post-WWII average.) By this metric, the current stock market boom has now run well ahead of the late 1990s one.

How should we think about this?

Logically, the value of corporate equity relative to GDP must reflect a combination of four factors: value added in the corporate sector as a share of GDP; corporate profits as a share of their value added; payouts to shareholders as a percentage of profits; and the value placed by markets on each dollar of payouts.

In other words, if corporate stock is worth more relative to GDP, that can be either because more of GDP is now happening in the corporate sector; or because more of the income from that activity is going to profits; or because more of those profits are being paid out to shareholders (rather than retained in the firm); or because financial markets place a greater value on each dollar of payment. Or of course some combination of those.

As with any accounting identity applied historically, it is useful insofar as it corresponds to (1) categories in the relevant data, and (2) distinct causal factors we believe to be at work.

For the first term, we are, again, using all nonfinancial corporate equity, which includes closely held as well as publicly-traded corporations, and the BEA’s estimate of potential GDP. (Both are in current dollars.) Value added is defined, as usual, as sales less the cost of non-labor inputs. Profits are after tax (and of course also after depreciation); conceptually, these are the funds potentially available for distribution to shareholders.2

Payouts I am defining as dividends less net new equity issues. That share repurchases are conceptually equivalent to dividends is not, I think, too controversial at this point (though it creates a lot of headaches). We are also adding shares retired through cash acquisitions, and subtracting shares issued whether in IPOs or otherwise. This might seem odd at the level of an individual firm, but at the aggregate level these other flows seem clearly equivalent to buybacks and dividends. If firm A buys up all the shares in firm B for cash, that is a payment from the corporate sector to shareholders, just as if firm A were buying back its own shares. Similarly, new shares issued are a reduction in the aggregate payments from the corporate sector to shareholders just as a reduction in dividend payments would be.

It might sound strange to define IPOs (whichgenerally are quite exciting for stock market participants) as equivalent to dividend reductions (which generally are not.) But this is where the aggregate perspective matters. Shareholders as a whole already own all the equity of the corporate sector as a whole. An IPO is a payment from shareholders to the corporate sector, exactly like buyback is a payment from the corporate sector to shareholders, without in either case any change in aggregate ownership rights. Or looking at it from another point of view, new corporations are in general competing with existing firms;the profits flowing out to shareholders of the new firm are to a first approximation deductions from the profits flowing to claimants on existing firms. Nice for the shareholders in the new firm, if it succeeds; but no use to shareholders as a class.

Finally, the valuation term asks, in effect, what is the market price of a dollar of income from the corporate sector. It’s analogous to the price-earnings or price-dividend ratios one sees at the level of individual corporations or indexes, though not identical given the nonstandard (but, I would argue, appropriate) way I have defined payouts. Here it also functions as the residual term, reflecting any change in the value of equity not explained by the other factors.

The figures below show the values of each of these terms over the past 80 years. What do we see?

We will start with the first term, corporate value added as a share of GDP. This shows how much of economic activity takes place in the corporate sector, and is potentially available for shareholders.

As it turns out, the corporate value added term does not do anything interesting. Yes, it is modestly lower (around 50 percent) after 2000 than its average in the earlier decades (53 percent), suggesting that all else equal, we might expect the value of corporate equity to be slightly lower relative to GDP in the 21st than in the 20th century. But this change is very small compared with the movements in the other terms. This factor might be important if we were comparing the US to other countries, but it is not part of the story here.

Next, profits:

Profits as a share of value added shows much more variation, falling by half in the 1980s, then rising in this century, in two big jumps — one after 2000 and the second over the past five or so years. While the corporate share of GDP doesn’t vary by even 10 percent over the whole period, profits as a share of value added are fully three times greater today than they were for much of the 1980s.

The third term is payouts.

Payouts (as I’ve defined them) also show large variation, rising from a bit under 40 percent of profits in the early decades to over 80 percent in more recent ones. The timing here is a bit different — though there is plenty of short-term variation, the long-run shift happens in a single big jump in the early 1980s. (This was the topic of an essay in my dissertation, which I never managed to publish as an academic article but did turn into a report for the Roosevelt Institute.) This term gets relatively little attention in discussion of stock prices, but it seems to me that it is as fundamental as profits to any discussion of long-term trends in the value of corporate equity.

Finally, the valuation term shows a lot of short- and medium-term variation but, perhaps surprisingly, no long run trend. Today’s ratio of around 40 is close to what we see in the 1950s and 1960s.

Again, what we are measuring with this last term is the ratio of equity value to shareholder payouts, including net share repurchases. The big spikes in the early 1970s and in 2000 are because those years saw exceptionally high new equity issues, which means very low payouts by my metric, and therefore very high ratios of equity value to payouts.

It is more common to talk about equity in relation to earnings, on the implicit assumption that profits are of equal value to shareholders whether they are paid out or not. I’ve shown this latter ratio below. But personally, I do not think that that is a good assumption. Shareholders evidently care a great deal about payouts — why else would companies pay dividends and make share repurchases? I think it is important to distinguish between corporations and the shareholders who exercise claims on them — the former are not simply the personal property of the latter. From this point of view, it is more natural to talk about valuation in terms of the price shareholders place on the income they actually get from corporations, as opposed to the underlying profits.

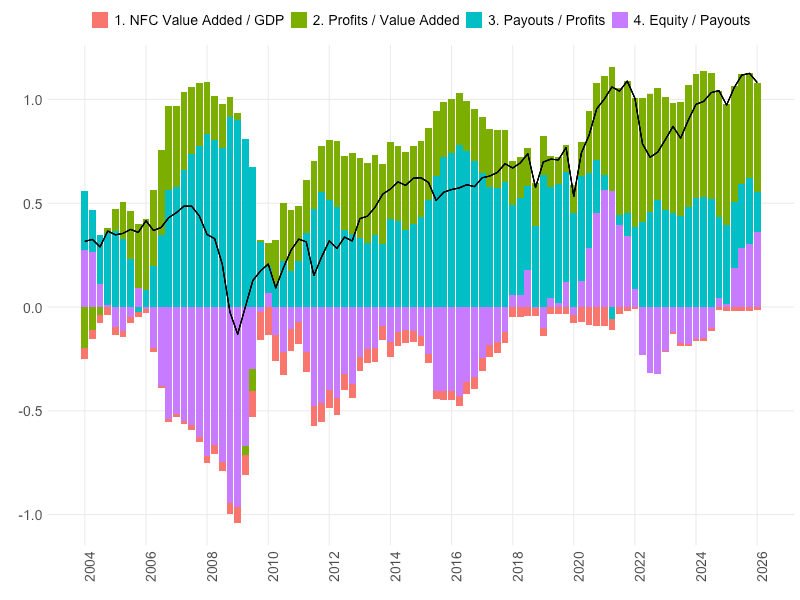

All of these series (except the last one) are combined in the next figure, which is really the whole point of this post. If you take one thing from one I’ve written here, this picture is it.

Equity value relative to GDP and its components, 1947-2026:

For this figure, I’ve converted the values to logs. This has the big advantage of converting the multiplicative relationship to an additive one, so that we can visually see the contribution made by each of them. But it can make interpreting the figure a bit tricky. Here, zero is the average value over the full period; positive one is a value about 2.7 times greater than the average, while negative one is a value about one-third of the average. The black line similarly describes the deviation of the equity-GDP ratio from its full-period average; the heights of the bars correspond to the contribution each term makes to that deviation. The data is quarterly; for all the terms except equity, I use rolling one-year averages.

As we can see, the log of the equity-GDP ratio is currently about 1.1 above its long-run average, corresponding to a value nearly three times greater. (2.2 today, versus a long run average of 0.85.) Just over half of this (0.53) is explained by higher profits relative to value added, 0.19 is explained by higher payouts relative to profits, and 0.36 is explained by the valuation term.

So already we can see that a simple explanation of today’s high equity values is going to be incomplete. Relative to the long-run average, we have three distinct factors each of which explains a significant share of today’s higher values.

Another thing that jumps out from the figure is that the previous historical peaks in equity values reflect quite different mixes of these components.

In the 1960s, profits as a share of value added were, for a while, well above average, though not as high as today; but the fraction of those profits flowing out to shareholders was much lower. Thus the much lower ratio of equity to GDP, despite comparable valuation ratios.

In the late 1990s, profits as a share of value added were much lower — less than 5 percent at the height of the tech bubble, compared with 10 percent in the 1960s and 15 percent today. But the fraction of profits paid out to shareholders was historically high, averaging over 100 percent for the 1998-2000 period. It’s worth noting in this context, also, that the collapse of equity value in the 1970s reflected a fall in shareholder payouts much more than in profitability; this is perhaps important context for the shareholder revolt that followed.

The big takeaway from this decomposition is that we should be cautious about assuming the stock market is overvalued — that we’re in a bubble, that this is another bout of irrational exuberance — simply because equity prices are high relative to the historical norm. Shareholders have it better than the historical norm, too. Corporations are more profitable. And more of those profits are flowing out to them. A bit of exuberance might be rational, under the circumstances.

On the other hand: If we focus on just the past 20 years, as in the figure below, the picture looks a bit different.

Yes, both profits and payouts are high relative to their long-run averages; but those shifts mostly came earlier, while the big rise in equity prices is more recent.Apart from the relatively brief collapse in profits during the Great Recession, almost all the variation in equity prices over the past two decades comes from the valuation term, rather than changes in the underlying payments to shareholders.

This is even more true over the past two years — equity values have increased sharply while profits have been stable and aggregate payments to shareholders have fallen, as dividend growth has stalled and net equity issue has turned positive.As a share of GDP, the net payments flowing from corporations to shareholders today are very close to where they were a decade ago; but corporate equity is worth 60 percent more. It’s hard to avoid the conclusion that either equity was undervalued in the mid-2010s, or it is overvalued now.

So which side do we focus on? Over the long run, most — tho not all — of the increase in the value of wealth in the form of corporate equity, is explained by what we might call fundamentals — the flow of payments to owners of that wealth. Over the short to medium run, on the other hand, almost all of the increase in the value of equity comes from valuation, and whatever financial-market dynamics drive that. Or as the old saying goes, in the short run the market is a voting machine, but in the long run it’s a weighing machine.

*

I want to say a bit more about the profits and payouts parts of the picture.

That high stock prices reflect to some extent a high level of corporate profits seems to be reasonably well understood, at least based on recent coverage in the Financial Times. This of course does not mean that high stock prices are justified, or sustainable; it just shifts the question to how justified or sustainable the high profits are.

This goes double to the extent that high valuations are based on an expectation of further increases in profits, as this recent FT piece suggests:

Wall Street’s expectations for company profit growth are rising at the fastest pace since the post-pandemic rebound, fuelling concern that an “earnings bubble” could be forming in the estimates that have underpinned the US stock market’s rally.

Analysts are now forecasting a 25 per cent increase in S&P 500 company earnings for the coming year, according to Bloomberg data, boosted by a resilient US economy and the AI boom.

However, just ahead of the second-quarter earnings season, some investors are growing concerned about the speed at which analysts’ estimates are rising…

This Alphaville piece goes further, saying that “supernormal profits are unsustainable, because they always are.” I don’t know about that. I don’t know if there’s any reason to think the profit share is stationary, to use the statistics jargon — apart from a dip in 2008-2009, profits as a share of value added have been greater than their long-run average in every year of this century, and seem to be getting farther from it. Capital really has won some lasting victories in the class war.

That is one natural way to look at profits — as a distributional variable. But there’s another way of looking at them, from the demand side.

We know, as readers of Keynes, that an increase in investment automatically creates an equal quantity of additional saving. If, furthermore, there’s little or no incremental saving out of wage income (a reasonable assumption, in my opinion) and if the fiscal balance and trade balance don’t change significantly (perhaps less reasonable, but we’ll go with it) then this additional saving must take the form of an increase in profits. This relationship is often known as the Kalecki-Levy profits identity, and is one bit of heterodox economics that has established a foothold in finance and the businesspress. The same identity says that an increase in the fiscal deficit or trade surplus should similarly lead to an equal increase in aggregate profits.

Exploring the math of this and the extent to which it is a reasonable first approximation of real-world dynamics would be an interesting exercise for another post. But it raises another point which I think is very relevant for thinking about the current situation: Even if the AI companies themselves are not particularly (or at all) profitable, AI-related investment spending is probably an important factor in raising aggregate profits. Just like the California gold rush generated plenty of profits for somebody, even if the vast majority of prospectors themselves went broke.

Or as this recent FT piece puts it:

The AI boom is lifting the fortunes of hundreds of formerly drab industrial, utility and mining companies as investors turn to the “picks and shovels” needed to build and power vast data centres. …

The companies benefiting include Caterpillar, best known for construction equipment but now supplying generators for data centres, 150-year-old German engineering company Hochtief, which will enter the Dax later this month, and Nucor, a steel supplier that has credited “white hot” AI demand for a “tsunami of earnings power”. …

The vast amounts of electricity needed for AI training are also fuelling demand for specialised power management, high-voltage electronics and cooling technologies. This has led to big interest in traditional suppliers of electrical equipment…

You could think of it like this: As long as there is strong investment demand and easy financing for it, the profits will be there …. but not necessarily for the companies carrying out the investment and getting the financing.

And this, perhaps, is the point where the macro perspective needs to give way to the micro one. Because it may be that, yes, in the aggregate, an ease in financing brings forth additional investment, which generates enough profits to justify the initial financing. But debt must be paid back not in the aggregate, but by the specific companies that incurred it. If the investment is one place and the profits are somewhere else, then at some point somebody’s survival constraint is going to be violated.

And I think I will end this post here.

I very much want to discuss the payouts piece of the equation, which in my mind is as important as profits, and much less discussed. But this post is already too long, and has taken much too long to write. So the payouts piece should be along, well, if not this month, then next month, or soon.

This is the edited transcript of a talk I delivered on March 5 at the Heilbroner Center for the Study of Capitalism at the New School for Social Research in New York, at the invitation of Julia Ott. The talk is an attempt to explain what Against Money (my forthcoming book with Arjun Jayadev) is about, and why it matters. Earlier attempts can be found here and here. You can listen to the full recording of this talk, including some quite interesting questions from the audience, here:

Since we are at the Heilbroner Center, I thought I would begin with Robert Heilbroner.

Heilbroner is best known for his book, The Worldly Philosophers, a popular history of economic thought. There’s an interesting discussion in the introduction to later editions of the book about his struggle to come up with a title for it.

He did not want a title that included the word economist — he understood that a book about economists would have, at best, limited appeal. His initial thought was to call it “The Money Philosophers.” But after considering that, he decided that it didn’t really fit his subjects, because, money, for the most part, was not a major concern for them.

I think he was right to have those misgivings, and to instead choose the title he did. Because money, perhaps surprisingly, plays a rather small part in the history of economic thought.

The dominant view on money among economists, which you can find in almost unchanged from the 18th century down to any contemporary textbook, is that money is neutral. There is a real economy, a concrete existing world of labor, of technology, of human needs and of resources that can meet them, which all exists prior to and independently of money. It’s in this real world that relative values are established, and where the possibilities for production exist prior to any sort of measurement in terms of money. Things would be exchanged in the same proportions in the absence of money, or with any other difference form or quantity of money. Money is at best a numeraire,a mild convenience to help us describe relative values and simplify exchange that would happen on essentially the same terms without it.

Going back to 1752, we find David Hume writing:

Money is nothing but the representation of labour and commodities, and serves only as a method of rating or estimating them. Where coin is in greater plenty; as a greater quantity of it is required to represent the same quantity of goods; it can have no effect, either good or bad…

What we have here is the idea, first, that there is a quantity of goods already existing in the world before we measure it or rate it with money, and second, that the use of money to coordinate the exchange of goods, to measure the quantity of goods, has no effect on that quantity, either good or bad.

Now Hume himself went on to complicate this argument in interesting ways. But for many economists down to the present, this is where the story stops.

Variations on this are the central throughline in economic thought around money. Coming down to our century, we find Lawrence Meyer, who was recently a member of the Fed’s Federal Open Market Committee, saying,

Monetary policy cannot influence real variables, such as output and employment. This is often referred to as the principle of neutrality of money. Money growth is solely the determinant of inflation in the long run. Price stability, in some form, is the direct, unequivocal, and singular long-term objective of monetary policy.

Again we see the same notion that control over money or credit cannot affect real outcomes, such as output or employment. At most, it can affect the measurement of those outcomes in terms of prices, that is, inflation.

I could multiply many similar quotes from the centuries in between these two. The great exceptionis, of course, Keynes.

If you got an economics education in the Keynesian tradition, as Arjun Jayadev and I did at the University of Massachusetts, then you probably spent a great deal of time thinking about money. You might even have imagined yourself as a money philosopher, or on the path to being one, or at least you were interested in what the money philosophers had to say. And you will have seen, more or less clearly, that there’s an important connection between the organization of money, the form of money, and real outcomes in the economy.

As Keynes himself put it in a 1932 article, which was arguably the opening salvo of the Keynesian revolution, the theory he was looking for was

a theory of an economy in which money plays a part of its own and affects motives and decisions and is one of the operative factors in the situation so that the course of events cannot be predicted, either in the long period or in the short, without a knowledge of the behavior of money.

The Keynesian vision is one where the operation of money is central in driving real outcomes, that money plays an active organizing role in the economy, and that one can’t understand real outcomes without an understanding of money.

Of course, Keynes was not by any means the first person to think this way, to think that the world of money and the concrete organization of production cannot be separated. There’s a kind of samizdat tradition, “the army of cranks and brave heretics” that Keynes acknowledges as his predecessors, who have made similar arguments.

One very interesting early figure in this tradition is John Law. John Law is remembered today as a sort of con artist, or as an early example of the dangers of trying to manipulate real outcomes by the use of money, because of his proposals adopted by the French government to set up a bank that would issue paper currency backed by land in the New World and other proposals for financial reform, and for what we might even today call industrial policy.

These proposals were not successful. Their failure contributed to the problems of the French monarchy in the 18th century. But the interesting thing about him is that he was not just a monetary reformer, that he was a genuine theorist. Joseph Schumpeter even puts him in “the front rank of monetary theorists of all time.”

Law’s proposals were motivated by a vision of money, as he put it, as not being merely “the value that is exchanged” but “the value in exchange” — the activity that happens through the use of money creates new value that does not exist prior to it. Coming from a background in Scotland, he writes about a situation where there is both vacant land and idle labor. They can’t be put together, they can’t be used productively, in the absence of money — to provide coordination, as we would say today.

The existence of coordination problems, creates the possibility that money is not just a yardstick for exchanges that would have happened regardless, but opens up new possibilities for cooperation — that there can be new value created by money that did not exist in the world prior to it. This is the opposite of the argument made by Hume and others and in principle opens up the possibility of creating real wealth, of transforming the real world through the manipulation of money.

We can trace a line forward from Law to Alexander Hamilton, a more successful advocate for financial reform in the context of a program of national development. Hamilton is not usually thought of as an economic theorist, but his writing in the “Report on Manufactures” and other proposals for developing American industry drew importantly on a vision of a more elastic and flexible monetary system.

Interestingly, one suggestion that Hamilton made for increasing the supply of “monied Capital” was for the federal government to permanently maintain a large debt. Anticipating contemporary heterodox economists, he argued that rather than crowding out private investment, federal borrowing would in effect crowd it in, because government debt was a close substitute for money — a source rather than a use of liquidity, as we might say.

We can follow this line on to Henry Thornton and the anti-bullionists in the early 19th century, who saw a flexible system of bank money as better suited than a rigid gold standard for promoting real economic activity. And then on to Thomas Tooke, who Karl Marx considered “the last English economist of any value,” and toWalter Bagehot and American monetary economists like Allyn Young, and then on to Schumpeter and of course Keynes himself and his successors.

What do these heterodox thinkers on money have in common?

From our point of view, first, they all see money not as a distinct object existing in a definite quantity, but as one end of a continuum of financial instruments or arrangements. They see money as a subset of credit. Schumpeter says that when thinking about money we “should not start from the coin,” we should not start from the discrete object that we call money. Rather we should, as all of these thinkers did to one degree or another, imagine a whole system of credit arrangements, some of which can be classified for various purposes as money. He distinguishes a “money theory of credit,” which most economists hold, from a “credit theory of money,” which is what he prefers. The starting point, the atomic unit, is the promise, not the exchange.

Second, and this is a central theme of our book, these thinkers all saw the interest rate as the price of money, rather than the price of savings. An important part of John Law’s argument for his financial reforms was that it would allow a lower rate of interest by making money more abundant. Walter Bagehot insisted that interest was the price of money, not of saving as orthodoxy has it.

The liquidity theory of interest is arguably the analytic keystone of Keynes’ General Theory. This question of whether the interest rate represents a real constraint, a trade-off between stuff today and stuff tomorrow, the price of savings or loanable funds, versus whether it is a fundamentally financial price set in financial markets as the price of money or liquidity, is athrough line in debates over money.

More broadly, there is the idea of money as a facilitator or enabler of economic activity, as a vehicle for transformation of the real world, versus the idea of money as a passive measuring rod or numeraire. Connected with this is the idea that money requires some form of active management. The orthodox view of money, along with seeing it as fundamentally or at least ideally neutral, has always looked for some kind of automatic rule to regulate credit and money.

Going back to Hume again at the beginning of this tradition, he at some points argued that banks should not exist. He wrote that the best bank would be one that took coins and kept them locked up until their owner came back for them, without creating credit in any form.

That is the extreme version of this position, but in less extreme forms there’s a constant attraction to the idea that bank credit should reproduce some natural logic of exchange, and not have any independent effect on economic activity. We can see it in the 19th century in the form of the real bills doctrine and of the gold standard — two different approaches to creating an automatic mechanism for regulating the creation of money and credit. Later in the century there were ideas of strictly capping the amount of paper money that could be produced, or separating the lending and payments functions of banks — an idea that constantly recurs in right-wing ideas for monetary reform. Behind this there was often the idea of an “ideal circulation,” where whatever the concrete form that money took, it should mimic the behavior of a pure metallic currency.

Then in the 20th century we get Milton Friedman’s idea that central banks should follow a strict money supply growth rule — an updated version of the cap on banknote issuance imposed on the Bank of England in the 1840s. And more recently we have the Taylor rule and similar rules that are supposed to guide the behavior of central banks. Some right-wing legislators have even proposed writing the Taylor rule into law, so the Federal Reserve would no longer have any choice about monetary policy.

What all these rules have in common is the idea that there is some kind of autopilot that you can put the management of money and credit on, so that it no longer involves any active choices, public or private — so that money will manage itself.

This goes with the idea that even if money is not always neutral in practice, that it ought to be neutral. It goes with the the idea that there is some set of natural outcomes dictated by the real material choices facing us, by the problem of scarce means and alternative ends that Lionel Robbins defined as the problem of economics, that there is an objective best solution to the trade-offs facing us as a society —and if money is telling us to do something else or allowing us to do something else, that is a problem. We need to make money automatic so that we can return to this genuine non-monetary set of trade-offs that we are trying to solve.

In other words, when we think of money as neutral, that implies a specific kind of views about social reality in general. If we think of money as a transparent window onto a pre-existing world of goods, a pre-existing set of relative values, a pre-existing set of opportunities and resources facing us,then we are going to see the world itself as fundamentally money-like. We are going to see the existence of prices, the division of social reality into discrete commodities with ownership rights attached to them, as a basic fact about the world, which money is simply revealing to us.

When we see money as a distinct institution, as a distinct social technology of coordination, then we can see the rest of the world as being different from that. We can see all the ways in which the process of production, all the ways we organize our society are different from what happens in markets and different from what is mediated by money. We can see the world not as a set of existing commodities that need to be allocated to their best use to satisfy human needs but as an open-ended collective project of transforming the material world.

This second view is what Keynes called the monetary production paradigm.

In the 1932 article that I earlier suggested could mark the beginning of the Keynesian revolution, Keynes distinguished a real exchange view of the economy from a monetary production view. The real exchange view he associated with the traditional view of money as neutral — it’s a vision of a world in which fundamentally the economic problem is barter. So for instance Paul Samuelson’s famous textbook, the most influential economics textbook of the 20th century, says that we can reduce essentially all economic problems to problems of barter.

In this world, the economic process is fundamentally about exchanging real things. Production is just a special case of exchange. You put in yourcapital, I put in my labor, we get a definite amount of output out that we divide in proportion to what we put in, on terms that we all knew and agreed on in advance.

The real exchange view of production was perfectly expressed by Keynes’ Swedish contemporary Knut Wicksell, the originator ofthe modern approach to monetary policy. He described economic growth as being like wine aging in barrels. We’d like to drink the wine today, because that would be nice; but on the other hand if we leave it to age in the barrel for longer it will improve in quality. The wine is already there, we know how much there is and how much better it will be next year. All the possibilities are defined in advance. We just have to decide what pace of drinking it will bring us the most pleasure.

A monetary production view of the world, on the other hand, is one in which the economic process is a one of collectively transforming the world. This is an active process that structured and mediated by money, and organized around the accumulation of money.In this view of the world, production is a cooperative human activity whose possibilities are not knowable in advance.

In this monetary-production paradigm, the fundamental constraint is not scarcity; the economic problem is not allocation. The fundamental constraint is coordination. When we stop imagining the world in terms of discrete commodities being combined in different ways, and start imagining it in terms of human beings cooperating (or not) to do things together,the problem becomes: How do we coordinate the activity of all these different people? What does it take to allow cooperation on a larger scale, between people who don’t have pre-existing relationships?

That is the problem that economic life is seeking to solve. And in particular, we argue, it is the problem that money helps solve. By its nature, this is not a problem that we can know where the opportunities are in advance. This uncertainty about the possibilities of the future is a fundamental component of Keynes’ vision, and is linked to the centrality that money has in his vision.

So far all of this has been pretty abstract. Let’s turn now to some of the implications of these questions for the real world. Because, after all, these debates are only interesting insofar as they help us become masters of the happenings of real life. They’re interesting insofar as they give us some ability to intervene in the world around us. The reason that Arjun and I wrote this book is that we came to feel that many of the concrete problems that we were interested in, and that other people are interested in, require a different view of money to make sense of them.

Let me give an example. The two of us wrote a number of papers some years ago, which were in some ways the starting point of this book, about the rise in household debt between 1980 and 2007. Between 1980 and 2007, household debt in the United States rose from roughly 50 percent of GDP to 100 percent of GDP. This was something you were very aware of if you were beginning your life as an economist in the 2000s, and it became even more interesting in the wake of the financial crisis of 2007–2009, which the rise in household debt seemed like one of the underlying causes of.

In general, when people talk about rising household debt they attribute it to rising household borrowing. Much of the time, people don’t even realize that those are two different things. There are articles where the title of the article is something like “explaining the rise in U.S. household debt” and then the first sentence of the article is, “why are U.S. households borrowing more than before?” Or even, “why are households saving less than before?” But these are different questions!

Of course it is true that insofar as someone borrows more money, their debt will rise; and if their income is unchanged their debt to income ratio will rise. This might in principle involve dis-saving, if the debt is financing increased consumption. In reality, though, it almost certainly doesn’t, since the great majority of debt is incurred to finance ownership of an asset.

Setting aside the dissaving claim — which is almost always wrong, though you hear it very often — it is true that an increase in borrowing implies an increase in debt. But your debt-income ratio can change for other reasons as well.

Think about two people who buy houses: If one person buys a larger house, or a house in a more expensive area, or if they make a smaller down payment, then they will certainly owe more money over time than the other person. But if one person buys a house when the prevailing interest rate is low and the other buys an identical house with an identical downpayment when interest rates are high, and they each devote an identical part of their income to paying their mortgage down, then over time the debt of the person who bought when interest rates were low will be lower than the debt of the person who bought when interest rates were high. If you are fortunate enough to buy a house with a low mortgage rate then over time your debt will be lower than somebody who wasn’t so fortunate.

This is even more true in the aggregate. If you see households devoting a certain share of their income to purchasing the services of homes that they live in that they own, those same payments are going to result in in more debt when interest rates are high and less debt when interest rates are low.

We also know that if you’re looking at a debt to income ratio, then as a ratio that has a denominator as well as a numerator. A more rapid increase in incomes — either what we call real incomes or incomes that rise because of inflation — will reduce that ratio of debt to income. And we know that if debt is written off, if the borrower defaults, then the debt ratio will also come down.

All of these are factors that influence the level of debt independent of what we think of as the real flows of expenditure and the income. So what Arjun and I did — which is very simple once you think of doing it — is take various periods of time and see how much of the change in debt income ratios over each period is due to changes in borrowing behavior and how much is due to these other factors. We called the other factors, the ones independent of current expenditure and income, Fisher dynamics, for Irving Fisher.

Fisher, incidentally, is an interesting figure in this context. On the one hand he was a very important advocate of this sort of neutral-money real-exchange vision we are criticizing. But he also in the 1930s wrote very persuasive account of the Great Depression in terms of financial factors — “The Debt Deflation Theory of Great Depressions” — where he explained the depth of the Depression by the fact that debt burdens rose even as borrowing fell, because prices and nominal incomes fell much faster than interest rates

Our point was that this dynamic is not unique to the Great Depression. Any time you have higher or lower inflation, or higher or lower interest rates, that is going to affect debt burdens exactly the way it did in the Depression. And what we found is that if you’re looking at this rise in household debt to income ratios between 1980 and 2007, essentially all of it is explained by these other factors, these Fisher dynamics, and none of it is explained by increased borrowing. If you compare the period of rising household debt after 1980 to the previous two decades of more or less constant debt-income ratios, people were actually borrowing more in the earlier period than in the later period.

The difference is that the interest rates facing households were much lower in the 1960s and 1970s than they were after the Volcker shock. The Volcker shock raised interest rates for households, and they stayed high for longer than the policy rate did. And during the 60s and 70s compared with the 1980 to 2007 period as a whole, inflation was significantly higher. (Real income growth was also a bit higher in the earlier period but that plays a smaller role.)

So what we have here is not a story about real behavior. It’s not a story about borrowing, about income and expenditure. All of these stories that we heard from both the left and the right about why household debt had risen — it’s because people have grown impatient, their time preferences shifted or they are competing over status or it’s inequality — none of this is relevant, because people were not in fact borrowing more.

Stepping back here, we can think of a set of monetary variables that scale up or scale down the weight of claims inherited from the past. Both interest rates and inflation function to change the value of claims in the form of debt inherited from the past, relative to incomes being generated today; and by the same token interest rates change the value of promises about future payment relative to incomes today. In an environment of abundant credit and low interest rates a promise about something you can deliver in the future, or an income you will receive in the future, is more valuable — it gives you a greater claim on income today. In an environment of low interest rates, what you will do, or can promise to do, in the future matters more; in an environment of high interest rates, and low inflation, what you did do in the past, the income you did receive, matters more.

This monetary rescaling of claims inherited from the past and claims generated by promises about the future, relative to income in the present — this is something that is constantly going on, in addition to whatever real activity people are carrying out. And many of the monetary outcomes that we’re interested in — like debt-income ratios — are fundamentally driven by this rescaling process and not by real activity.

So these historical changes in household debt are a concrete application of the larger perspective that we’re trying to develop in this book.

Another important application is the interest rate. How we think about the interest rate is central to a lot of the debates between different perspectives in economics, or maybe more precisely, it’s where the differences between them become visible, become unavoidable.

One way I think about it: Imagine trying to lay a flat map over globe. You can do itif your map is of just a little portion of the globe — we all know we have flat maps of various places that all exist on a sphere in reality, and they work okay.But if you try to put your flat map over the whole globe it’s not going to work — either you’re going to have to crumple it up somewhere or it’s going to rip somewhere. The interest rate then is one of the sites where the flat map of this vision of the economy as a process of market exchange rips, when we try to fit it over a world of active transformative production through human cooperation into an unknown future.

The way that you’re taught to think about the interest rate, if you get an economics education, is that it’s the price of savings, or loanable funds — it’s a trade-off between using the pot of resources that currently exist for consumption or for making the pot bigger in the future. We think, so much stuff was produced, some people have it, and if they don’t need it right now they can lend it to somebody else who’s going to use it to carry out production, which will mean more stuff in the future. In this view the interest rate is the price of consumption today in terms of consumption tomorrow.

Interest, in this view, is a fundamentally non-monetary phenomenon: It’s a question of the real trade-offs imposed by people’s material needs and the material production they’re capable of.

This is a long-standing view — we can go back 200 years to Nassau Senior describing interest and profit as the reward for abstinence. By “abstinence” he means the deferring of enjoyment. The term has a nice moralizing religious tone to it, but the fundamental point is that the interest rate is the return on consuming later rather than earlier. We can find exactly the same thing in, let’s say, Gregory Mankiw’s textbook today. To quote:

Saving and investment can be interpreted in terms of supply and demand. In this case, the ‘good’ is loanable funds, and its ‘price’ is the interest rate. Saving is the supply of loanable funds…Investment is the demand for loanable funds— investors borrow from the public directly by selling bonds or indirectly by borrowing from banks.

Here, again, we have a certain amount of stuff — it already exists— and you can either use it now, or defer your enjoyment of it by lending it to somebody else who will use it productively. One striking thing about Mankiw’s formulation is that he makes a point of saying that it’s a matter of indifference whether this happens through banks or not.

So in this vision, the interest rate is a trade-off between goods today and goods tomorrow, or goods used in consumption and goods used in production. But the fundamental problem, as soon as we start thinking about this in a real-world setting, is that it doesn’t seem to match up at all with the interest rate as we actually observe it.

One of the first things you learn if you get a Keynes-flavored economics education, but also something that anyone who deals with this stuff practically realizes, is that when you go to the bank to get a loan, the bank is not making that loan out of anybody’s savings. A bank makes a loan by creating two offsetting IOUs. There is the bank’s IOU you to you, which we call a deposit, and your IOU to the bank, which we call a loan. The deposit is newly created in the process of making the loan — it’s what used to be called fountain pen money, it’s ledger money, it consists of two offsetting entries in a ledger. Nobody’s savings are involved. Nobody else needs to defer their consumption to allow you and I to write IOUs to each other.

There’s a very nice explainer from the Bank of England on how banks create money which you can look up online, that lays this out very clearly. I assign it to my undergraduates every year. It’s not a secret that loans, in the real world, do not involve somebody taking some goods that they have in their possession and bringing them to some kind of central clearing house where somebody else can check out the goods to use in some production process. When you get a loan, you’re not receiving a bag of cash that someone else brought into the bank. You’re getting a deposit, which is just a record kept by the bank. Fundamentally, a loan is the creation out of thin air of two offsetting promises of money payment.

Now of course when you receive your promise from the bank — in other words, your deposit — you will normally use that to acquire title to some goods and services, or authority over somebody else’s labor. But the loan itself did not require anyone to have already decided to let you use those goods. It did not require anyone’s prior act of saving.

Of course anybody can write an IOU. You and I could sit down and write promises to each other, just as you and the bank do when you get a loan. The key thing about the bank, here, is that its promise is more credible than yours. If I ask for your bicycle and promise to give you something of equal value down the road, you probably won’t agree. But I can make that same promise to bank, and the bank can then make that promise to you. And that’s fine.

This is why Hyman Minsky, the great theorist of finance, said that the defining function of banks isnot intermediation, but acceptance. You can’t get a claim on labor, on real resources, simply by promising you’ll do something useful with them. But a bank might accept your promise, and then the promise that it makes to you in return can can be transferred on to other people in return for a claim on real resources, which you can use to create new forms of production that otherwise wouldn’t exist. And this is the other side of the Keynesian vision — the fact that banks can create money by lending allows for the reorganization of productive activity in new ways that wouldn’t be possible otherwise.

If you’re a business owner, say, you can now expand your business, because the bank’s promise is more credible than your promise. You as a business owner cannot hire workers simply by saying this business is going to be successful and I’ll give you a share in it — well,if you’re in Silicon Valley sometimes you can, but most businesses can’t. The bank’s promise is more credible — unlike yours, it will be accepted by workers as payment. You can use this loan created out of thin air to carry out new activities, to create things that did not exist before.

The problem for the orthodox view is that banks exist. Banks exist and, to anyone taking a naive look at capitalism, they seem rather important. Trading money claims is evidently pretty central to the way that we organize our activity.

Central banks also exist, and influence the terms on which banks make loans, even though they themselves don’t do any saving or investing. If you believe the story in the Mankiw textbook that the supply of savings is being traded against the demand for investment and that’s what determines the interest rate — well, a central bank is neither providing loanable funds nor is it using loanable funds for investment, and it doesn’t restrict the terms on which anyone is allowed to make private contracts. So how could it influence the price of loanable funds?

Wheres if we think of the interest rate as being a combination of the price of liquidity — flexibility — and a conventional price set in asset markets, then it is much easier to see the critical role of banks, and why central banks are able to influence it. This is something we spend a lot of time on in the book.

Now, once common way of reconciling the idea of a savings-determined “real” interest rate with the monetary interest rate we see in the real-world financial system is through the notion of a “natural interest rate”. This is the idea that, ok, there is here on Earth an interest rate that is set within the banking system that has to do with the terms on which promises of money payments are made. But there’s another interest rate that exists in some more abstract world, which we can’t see directly, but somehow corresponds to the way goods today trade off against goods tomorrow, or the way they would trade off if markets functioned perfectly. This second interest rate is what’s called the natural rate. The actual rate might not always follow it. But it should.

As an aside, I should say that this sort of transformation of a descriptive claim, that is supposed to be a statement about how things actually work, into a prescriptive claim about how things should work, is very common in economics.

We can find a very nice statement of this view from Milton Friedman on the natural rate of interest and its cousin the natural rate of unemployment, where he describes them as the rates that would be

ground out by the Walrasian system of general equilibrium equations, provided there is embedded in them the actual structural characteristics of the labor and commodity markets, including market imperfections, stochastic variability of demands and supplies, the cost of information about job vacancies and mobility, and so on.

In other words, if we could somehow make a perfect model of the economy, then we could calculate what the natural rate would be, and that’s the thing we should be trying to achieve with our policy influencing the interest rate. Obviously, as soon as you start thinking about it, this doesn’t make sense on multiple levels. But it’s a very attractive formulation precisely because it papers over this gap between a theoretical and ideological vision of interest that sees it as a real trade-off between the present and future, and the actual concrete reality of interest that is determined in financial markets on the basis of liquidity and convention.

So again, if you come more recently, you look at Jerome Powell talking about monetary policy in a changing economy, a speech he gave a few years ago. There he introduces the idea of r*, the natural rate of interest, by saying, “in conventional models of the economy, major economic quantities such as inflation, unemployment, and the growth rate fluctuate around values that are considered normal, natural, or desired.”

I think that’s a very nice illustration of the thinking here, because normal, natural, and desired are three different things, and this r* is conflating them all together.Which is it? Is it normal, as in typical or average? Is it natural? (What would it mean for an interest rate to be artificial?) Or is it desired? In fact, it’s whatever the central bank wants. But the slippage between these different concepts is essential to the function of ideas like the natural rate.

Think of the transmission in a car: You’ve got a clutch, because the engine is turning at one speed, and the wheels are turning at a different speed. If they just join up, you’re going to shatter your drive shaft. So you have two discs that can turn independently of each other, but also exert some force on each other, so you get a smooth connection between two systems that are behaving in different ways. In this case r* is the clutch between theory that’s going one way and the reality, which the central bank has to acknowledge is going in a different way. The ambiguity of the term is itself normal, natural, and desired.

So then Powell continues, these natural values are “operationalized as views on the longer-run normal values of the growth rate of GDP, the unemployment rate, and the federal funds rate, which depend on fundamental structural features of the economy.” Here again there is a conflation between the things that the central bank is trying to do, things that are the sort of normal, average, expected, long-run outcomes, and things that are in some sense determined by some set of non-monetary fundamentals independent of monetary activity. And again, you get a controlled slippage between these different concepts.

There’s another nice version of this from a group of economists associated with the European Central Bank. They say, at its most basic level, the interest rate is the price of time, the remuneration for postponing spending into the future. So this, again, this is Nassau Senior.

It’s abstinence. It’s the price of waiting for your enjoyment. So this sounds like something that should be purely non-monetary.

This is r*. And then the ECB economists say, “while unobservable, r* provides a useful guidepost for monetary policy as it captures the level of interest rates which monetary policy can be considered neutral.”

I just love the idea of an unobservable guidepost. It’s a perfect encapsulation of how the natural rate concept functions.

Because, of course, what’s really going on here is the central bank sets the interest rate at a level that they think will achieve their macroeconomic objectives, whatever they are. Inflation is too high. We need a higher interest rate. Unemployment is too high. We need a lower interest rate. Maybe we’re concerned about the exchange rate. Maybe we’re concerned about the state of financial markets. Whatever they’re most worried about, they choose an interest rate that they hope will help.

And then after the fact, they can say, well, we wrote down a model in which this would be the interest rate, so therefore it is the natural interest rate. There’s no genuine content there — r* and the associated models are just a way of describing whatever you’re doing as conforming to a natural outcome that is dictated by the fundamentals out of your control, as opposed to a conscious political choice that prioritizes some outcomes above others. This sort of ideological construct is fundamental in depoliticizing one of the main sites of economic management in modern economies.

And this is an important part of the story that we’re trying to tell in this book. The problem, if you believe in a more egalitarian, democratic, or socialist vision of the economy, is not simply, is not even mainly, that right now the world is organized through markets, and we’re going to have to come up with some better economic system to replace markets. The reality is the world is not primarily organized through markets. What we have, very often, are imaginary market outcomes being claimed as the unobservable guideposts so that people with authority claim to be following them. We have an ideological system that allows processes of power and planning to present themselves as somehow representing or standing in for market outcomes.

Another area where I think this comes through very clearly is in the history of the corporation. We wrote a lot on this which we were, unfortunately, not able to fit into this book — it will be in another book. But it’s a good illustration of the larger vision we are trying to develop.

If you look at the way people talk about our economy, almost across the political spectrum, they will describe it as a market economy. We have all kinds of outcomes that are dictated by markets, decisions about production are guided by prices, the economy is organized through market exchange.

And, at least among economists, the way we talk about production implicitly treats it as just a special kind of market.

This is certainly the way economic textbooks approach production. We talk about labor markets, and capital markets. We imagine production as a process where someone purchases a certain amount of labor and a certain amount of capital, puts them in a pot, and gets a certain amount of salable output at the other end.

But when you look at how corporations work, it’s very clear that they are not organized as markets. They’re not internally structured through money payments — yes, of course, workers have to paid a wage to show up, but once they are there there isn’t some kind of market for their services. The boss just tells them what to do. Nor are corporations organized internally around the pursuit of profit, though that obviously guides how they relate to the outside world.

Now, historically, we can find cases of businesses whose internal structures are more market-like. Some of the first large corporations were organized through what were called inside contractors. You would you hire a skilled craftsman, artisan, who comes and works in the physical space, but is responsible for hiring their own assistants, buying their own materials, working them up and then selling them on tothe next inside contractor.

That turned out to be not a very good of organizing a corporation, even when they were they producing the sort of thing — clothing, say — that could in principle be made by independent artisans. It didn’t work at all for large-scale industrial production. It’s obviously not the way corporations are organized today. We would argue that a central through-line of the history of the corporation is a fundamental conflict between the organization of production in large-scale, ongoing, socially embedded forms, and the logic of money and markets that surrounds them, and that the claims upon them by wealth holders continue to be exercised through.

If we go back to what many people would consider the first modern corporation, the East India Corporation, we find right at its beginning the first conflict between shareholders and managers. The original structure had been a kind of pooling of resources between a number of independent merchants for joint operations in the East for 20 years, after which they would sell any remaining assets, divide up the profits, and dissolve the corporation. That was the legal form.

But the East India Corporation turned out to be very successful at its mix of trade and piracy. People have argued that this hybrid of trade and warfare was really Europe’s specialty, the one thing it did better than the rest of the Old World. In any case, East India Company was very successful at it. But — and this is the key thing — it required a big investment in forts, soldiers, local political alliances. Things that can’t just be sold off and divided among the partners.

So after 20 years, this is a very successful enterprise, and the people running it would like to keep operating it and believe they can do so profitably. And now the shareholders are saying, it’s time to divide everything up. But of course, if you sell off the forts and so on, they’re no longer of any value. And so there was a long conflict —legal, political —that ended with the managers winning, the shareholders losing, and the corporation being allowed to continue operating.

Losing the legal fight turned out to be good news for the shareholders. The companycontinued paying out large dividends. It never once raised any funds in the stock market. It continued operating and paying dividends for hundreds of years out of its own profits.

There are two interesting things about this story, to me.

First of all, right from the beginning, we have a conflict between an ongoing process of production which has real material benefits, and the claims by the elite against that process, which they would like to exercise in the form of money. If you operate forts and you have ships and you have your local allies, then you can carry out trading and trading-slash-piracy activities that you can’t do without those things. But once you’ve laid out money to build a fort, you own a fort. It remains a fort. You can’t turn it back into money. And you, as a wealth owner, put your money out to get more money. You don’t want to be master of a fort. You want a liquid financial claim that you can trade.

The other point is that the financial side of the operation is not about pooling money. It’s not about raising capital.

The East India Company, again, continues having shareholders, continues paying dividends in order to satisfy their claims, despite never raising funds from the stock market over the next 200 years of their existence. Whatever the stock market is doing here, it’s not a system for getting real resources into the corporation.

We can find this same principle down through the history of the corporation. When in the beginning of the 20th century we see the generalization of the corporate form, it’s not a process where large-scale investment required raising more funds. The problem that the corporation is solving is that you have large-scale enterprises with long-lived specialized fixed assets, on the one hand, and wealth owners, on the other hand, with claims on those enterprises — often the owners of smaller enterprises that merge into one larger one, or the heirs of the founder — who don’t want an interest in this particular company. They want money. And so the function of the corporate form is to allow the conversion of ownership rights into money — to enable payments that will satisfy these claimants, so that their authority over the production process can be pooled, their smaller interests can be assembled into a larger whole.

This is not a system for raising funds for investment. It’s a system for consolidating authority. It’s a system for reconciling the need for large-scale, long-lived organizational production, on the one hand, with the desire of the wealthy to hold their wealth in a more money-like form, on the other. As William Lazonick says, the corporation is not a vehicle for raising funds for investment, it’s a vehicle for distributing money to the wealthy. The origin of the corporation as we know it is as a vehicle for moving funds out of productive enterprises to asset-owners.

We can see this same conflict in the shareholder revolution of the 1980s, where people like Michael Jensen argued that the existing managers of corporations were too focused on the survival and growth of the enterprise as such. Managers were too interested in the particular productive process that they were stewards of, as opposed to generating money payments to shareholders, to finance.

What we see again and again is thatproduction depends on ongoing relationships — many of them, obviously, hierarchical, others based around cooperation, or on what David Graeber calls baseline communism, or on people’s intrinsic motivation to do their work well. But not on arm’s-length market relationships.

Our argument is that, yes, under capitalism, money expands itself by being committed to production. But there is a fundamental conflict between the logic of production and the logic of money.

Through the whole history of capitalism we have this conflict. Owners of money want more money. So they commit their money — their claim on society — to some particular enterprise, which they hope will return more money to them in the future. But in the meantime, the participants in that enterprise want to operate it, expand it, according to its own particular logic. Almost everyone here has probably encountered Marx’s formula M-C-P-C-M’. But the point that Arjun and I are trying to call attention to, is, how, or whether, C’ turns back into M’ is a tricky political question.

From the point of view ofparticular enterprise, the conversion back to money appears as a kind of imposition, a demand from outside. The enterprise can reproduce itself on its own terms with a claim on certain use values for which it produces other use values in return.

Where money is necessary — this is important — is where something new is being done, where there’s a need to organize production in some new way, for coordination between strangers who don’t have a relationship with each other. Money is genuinely productive insofar as the development of our productive capacity requires breaking up existing ways of organizing production, dissolving existing relationships, extinguishing obligations, and starting from square one.

Money should be seen as a specific kind of technology of social coordination. It’s a way of organizing human activity in new ways that it hasn’t been organized before.

One way to think of this is of money as a sort of catalyst. On the one hand, it acts as a social solvent. It breaks up existing relationships, as Marx and Engels famously described in the Communist Manifesto — “all that solid melts into air”. It replaces social ties with the callous cash nexus.

We can all thinkof examples of this. Money is a way of erasing relationships. A money payment replaces some ongoing connection between people. It takes an existing obligation and it extinguishes it. Money is a tool for breaking social ties, for replacing production that’s organized through ties of affinity, of affection, of kinship, of obligation, with arms-length cooperation between strangers, who could walk away from each other and never see each other again. Money says, we are done, we are settled, we owe nothing more to each other.

But that is only the first step. Because after we have broken up these smaller social molecules, these smaller-scale structures of production, after we have broken up the organization of production through a family, a village, a guild, that is not the end of the story.

Money facilitates cooperation among strangers, and it makes strangers out of family and friends. But people do not remain strangers. People who are engaged in cooperative activity of whatever kind form new social ties and new connections. This is partly because, organically, human beings connect to each other, and partly because the activity of production requires it.

Production requires cooperation beyond what you can get through arms-length transactions. It requires intrinsic motivation, it requires trust, it requires people’s desire to do their job well and their loyalty to other people. And it requires, at least in our society, command and hierarchy, which in turn requires some form of legitimacy. People have to know who can give what commands.

All of that involves the creation of social relationships. You can see money as a moment, in which older, smaller-scale forms of cooperation are broken up, creating the possibility for the reassembly of their components into larger forms of cooperation, larger-scale cooperation. The organization of society through money is a temporary stopping point.

What’s interesting is that if you go back to thelate 19th century, the early 20th century, this was something many people perceived as almost inevitable. If you read the next-to-last chapter of Capital,Marx’s vision is essentially this: Having broken up the older forms of small-scale property and small-scale production and reassembled human activity in the form of large-scale cooperation, an extensive division of labor, production based on conscious scientific knowledge — after all that,it will be, he says, “infinitely less violent” to replace that with socialism than it was to break up all of those smaller structures earlier. Does Marx say that we’ll just look out the window one day and say, oh, hey, it’s socialism? No. But it’s not that far off.

Or similarly, you can find Keynes writing in the 1920s saying that the most striking fact about the world that he sees around him is the tendency of large enterprises to socialize themselves. Corporations, having been established to carry out some particular purpose, to produce some concrete use value, becomes oriented towards the production of that use value. They cease to be oriented towards producing profits for their shareholders.

This is, in some sense, the same story that shareholder advocates like Michael Jensen toldin the 70s and 80s. Except that they saw it not as the march of history, but as a problem to be overcome. And this is the point that we come back to in our book. In practice, productive activity is overwhelmingly organized in non-market ways. But acknowledgment of this fact is profoundly threatening to elites, whose claim on society is expressed in terms of money.

This is the point. We don’t see how much of our life is already organized in non-market ways.

We all of us in this room came here for non-market reasons. None of us was paid to be here. None of us came here because a market signal told us to.

There are, obviously, payments that organize the operation of this building. But there is also an activity taking place in this room, in this building, that is not a market outcome, that is not organized through money payments, that doesn’t produce or respond to price changes.

Education is an activity that is particularly resistant to organization through markets and money payments and the pursuit of profit. But it’s not unique. Many of us came here on the MTA, an institution that was set up originally according to the logic of markets and money payments. But that didn’t work for running a transit system. The MTA didn’t become public because of an ideological crusade to socialize it. It became public because it could not simultaneously fulfill its social function while still being operated profitably. So the state had to take it over.

What we see around us is that the organization of production in practice calls for non-market forms — money does not perform the coordinating role that it purports to. But what we also see is that the structures of hierarchy and authority in our society very often justify themselves and legitimate themselves as if they were forms of market coordination. Money and property rights become badges of authority that are worn by the people who in fact issue commands through systems of hierarchy and personal domination.

The great challenge that we face if we wish to transform this system is not that we need to find new ways of non-market coordination. It is to find ways of democratizing the forms of planning and hierarchy that exist. We do not have to ask, well, how do we organize production without markets? — because we already do.

The great challenge is the enormous resources of violence in the hands of money owners,and their willingness to see the existing organization of collective action wrecked rather than allowing it to socialize itself, no matter how strongly the actual needs of production point in that direction.

The problem — the fundamental problem,at this moment it feels clearer than ever — is how to overcome the enormous powers of coercion and violence in the hands of those whose status and authority is expressed through money.

(I wrote this post back in 2015, and for some reason never posted it. The inspiration was a column by Matt Levine, where he wondered what Marx would think of the modern corporation.)

Let’s begin at the beginning.

Capital, for Marx, is not a thing, it’s a social relation, a way of organizing human activity. Or from another point of view, it’s a process. It’s the conversion of a sum of money into a mass of commodities, which are transformed through a production process into a different mass of commodities, which are converted back into a (hopefully greater) sum of money, allowing the process to start again.Capital is a sum of money yielding a return, and it is a mass of commodities used in production, and it is a form of authority over the production process, each in turn.

When we have a single representative enterprise, managed by its owner and financed out of its own retained profits, then there’s no need to worry about where the “capitalist” is in this process. They are the owner of the money, and they are the steward of the means of production, and they are master of the production process. Whatever happens in the circuit of capital, the capitalist is the one who makes it happen.

This is the framework of Volume 1 of Capital. There the capitalist is just the personification of capital. But once credit markets allow capitalists to use loaned funds rather than their own, and even more once we have joint-stock enterprises with salaried managers in charge of the production process, these roles are no longer played by the same individuals. And it is not at all obvious what the relationships are between them, or which of them should be considered the capitalist.This is the subject of part V of Volume 3 of Capital Vol. 3, which explores the relation of ownership of money as such (“interest-bearing capital”) with ownership of capitalist enterprises.