Greece doesn’t need a new currency, it needs control over its central bank.

The Greek crisis is not fundamentally about Greek government debt. Nor in its current acute current form, is it about the balance of payments between Greece and the rest of the world. Rather, it is about the Greek banking system, and the withdrawal of support for it by the central bank. The solution accordingly is for Greece to regain control of its central bank.

I can’t properly establish the premise here. Suffice to say:

(1) On the one hand, the direct economic consequences of default are probably nil. (Recall that Greece in some sense already defaulted, less than five years ago.) Even if default resulted in a complete loss of access to foreign credit, Greece today has neither a trade deficit nor a primary fiscal deficit to be financed. And with respect to the fiscal deficit, if the Greek central bank behaved like central banks in other developed countries, financing a deficit domestically would not be a problem. And with respect to the external balance, the evidence, both historical and contemporary, suggests that financial markets do not in fact punish defaulters. (And why should they? — the extinction of unserviceable debt almost by definition makes a government a better credit risk post-default, and capitalists are no more capable of putting principle ahead of profit in this case than in others). The costs of default, rather, are the punishment imposed by the creditors, in this case by the ECB. The actual cost of default is being paid already — in the form of shuttered Greek banks, the result of the refusal of the Bank of Greece to extend them the liquidity they need to honor depositors’ withdrawal requests. [1]

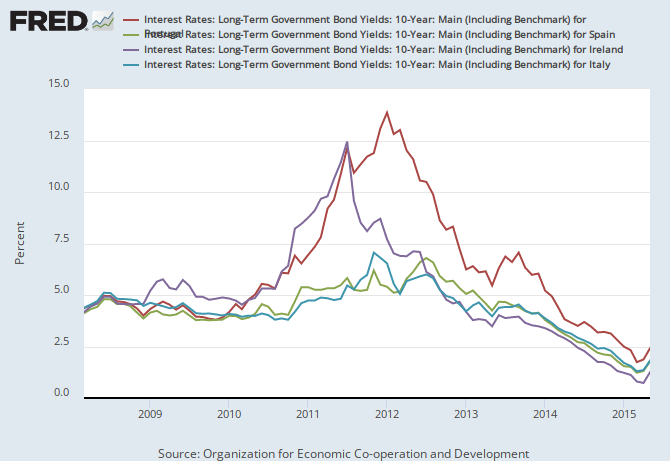

(2) On the other hand, Greece’s dependence on its official creditors is not, as most people imagine, simply the result of an unwillingness of the private sector to hold Greek government debt, but also of the ECB’s decision to forbid — on what authority, I don’t know — the Greek government from issuing more short-term debt. [2] This although Greek T-bills, held in large part by the private sector, currently carry interest rates between 2 and 3 percent — half what Greece is being charged by the ECB. And of course, it’s not so many years since other European countries were facing fiscal crises — in 2011-2012 rates on Portugal’s sovereign debt hit 14 percent, Ireland’s 12, and Spain and Italy were over 7 percent and headed upwards. At these rates these countries’ debt ratios — not much lower than Greece’s — would have ballooned out of control and they also would have faced default. Why didn’t that happen? Not because of fiscal surpluses, delivered through brutal austerity — fiscal adjustments in those countries were all much milder than in Greece. Rather, because the ECB intervened to support their sovereign debt markets, and announced an open-ended willingness to do “whatever it takes” to preserve their ability to borrow within the euro system. This public commitment was sufficient to convince private investors to hold these countries’ debt, at rates not much above Germany’s. Needless to say, no similar commitment has been made for Greek sovereign debt. Quite the opposite.

{kind=link}

So to both questions — why is failure to reach agreement with its official creditors so devastating for Greece; and why is the Greek government in hock to those creditors in the first place? — the answer is, the policies of the central bank. And specifically its refusal to fulfill the normally overriding duties of a central bank, stabilization of the banking system and of the market for government debt, a refusal in the service of a political agenda. The problem so posed, the solution is clear: Greece must regain control of its central bank.

Now, most people assume this means it must leave the euro and (re)introduce its own currency. I don’t think this is necessarily the case. It’s not widely realized, but the old national central banks did not cease to exist when the euro was created. [1] In fact, not only do they continue to operate, they perform almost all the day to day operation of central banking in the euro area, with, on paper, a substantial degree of autonomy from the central authorities in Brussels. So what’s required is not “exit,” not a radical step by the Greek government. Rather simply a change in personnel at the Bank of Greece. The BoG only needs to halt what is in effect a politically motivated strike, and return to performing the usual functions of a central bank.

Now, I cannot exclude the possibility that if Greece takes steps to neutralize the creditors’ main weapon, they will retaliate in other ways, which will result in the eventual exit of Greece from the euro. (Though “exit” is not as black and white as people suppose. [2]) But this would be a political choice by the creditors, not in any way a result of economic logic. We should not speak of exit in that case, but embargo.

Here is my proposal:

1. The Greek government takes control of the Bank of Greece. It replaces the BoG’s current leadership — holdovers from the old conservative government, appointed at the 11th hour when Syriza was on the brink of power — with suitably qualified people who support the program of Greece’s elected government. The argument is made that the central bank has abused its mandate, and failed in its fundamental duty to maintain the integrity of the banking system, in order to advance a political agenda.

Either legislation could be passed explicitly subordinating the BoG to the elected government, or use could be made of existing provisions for removal of central bank officials for cause. The latter may not be feasible and we don’t want to get bogged down in formalities. Central bankers have critical public function and if they won’t do it, they must be replaced with others who will. Whatever the law may say.

2. The new Bank of Greece leadership commit publicly to maintain the integrity of the Greek payments system, to protect deposits in Greek banks and to prevent bank runs — the same commitment the ECB has repeatedly made for banks elsewhere in Europe. The Greek government asserts its rights to license banks and resolve bank failures. Capital controls are imposed. Greek banks reopen.

3. If necessary, the BoG resumes Emergency Liquidity Assistance (ELA) or equivalent loans to Greek banks. While the promise to do this is important, it probably won’t be necessary to actually resume ELA on any significant scale because:

– removing the previous threats to withdraw support from Greek banks will end the bank run and probably lead to the voluntary return of deposits to Greek banks.

– capital controls and, if necessary, continued limits on cash withdrawals, block any channels for deposits to leave the Greek banking system.

– resumption of Greek payments to public employees, pensioners, etc., to be soon followed by resumed economic growth, will automatically increase the deposit base of Greek banks.

4. The Greek government resumes spending at a level consistent with domestic needs, including full pay for civil servants, full payment of pensions, etc. Taxes similarly are set according to macroeconomic and distribution objectives. The resulting fiscal deficit is funded by issue of new debt to domestic purchasers. This new debt will be senior to existing debt to the public creditors.

It may be that this debt will end up being held by the banks, but that is no big deal. Greek government debt currently accounts for less than 6 percent of the assets of Greek banks, the lowest of many major European country and barely half the euro-area average. And in the absence of capital flight, bank assets and deposits will increase in line, so there is no need for any additional financing from the Bank of Greece. Even more: If resolution of the crisis leads to a repatriation of Greek savings abroad, then the increase in deposit liabilities of Greek banks will be balanced by increased reserves at (or rather reduced liabilities to) the Bank of Greece. The BoG in turn will acquire a more positive Target balance, or if it’s ejected from Target (see below), an equivalent increase in foreign exchange holdings.

5. The interest rate on the new debt needs to be comfortably less than the expected nominal growth rate of the Greek economy. I see no reason why this will not be true of market rates — there are already private holders of Greek T-bills with yields between 2 and 3 percent, and the combination of a Greek central bank committed to stabilizing the market for Greek public debt, and capital controls preventing Greek banks and wealth holders from acquiring foreign assets, should tend to push rates down from current levels. But if necessary, the Greek central bank will have sufficient hard and soft tools to get Greek banks to hold the new debt at acceptable rates.

6. The official creditors are offered a take-it-or-leave-it swap of existing loans for new debt. (I think this kind of forced restructuring is preferable to outright repudiation for various reasons.) The new debt will have a combination of writedown of face value of the current debt, maturity extensions and reduced interest rates so as to keep annual payments at some reasonable level. I think it might be better to avoid an explicit reduction of face value and simply offer, let’s say, 30 year bonds paying 2%, of equal face value to the current debt. It would be best if the new bonds were “Greek-denominated.” Perhaps it’s sufficient to say that the new bonds are issued under Greek law.

7. The Greek government must be prepared for declarations from the creditors that its actions are illegal, and for possible retaliation. Rhetorically, it may be helpful to emphasize that Greece remains sovereign and Greek law continues to control the Greek central bank and private banks; that the ECB (and its agents at the Bank of Greece) have abused their authority to advance a political agenda; and that the wellbeing of the Greek people must take priority over treaty obligations. But framing may not make much difference here and anyway these kinds of tactical-political questions are for the Syriza leadership and not for an American sympathizer.

What concrete form will creditor retaliation take? One possibility is they will stop deposits in Greek banks from being used to make payments elsewhere in Europe, by shutting off Bank of Greece access to Target2, the settlement system that currently clears balances between national central banks within the eurosystem. [3] Concretely, lack of access to Target2 needn’t be crippling. Payments within Greece won’t be affected, domestic interbank settlement can use accounts at the Bank of Greece just the same as now. Foreign payments will be made using deposits at banks in the exporting country, just as trade payments outside the euro area are already made. Since Greece currently has a small trade surplus, there is no need for anyone outside of Greece to accept a Greek bank deposit in payment. And even if foreign borrowing is desired, the resulting funds can take the form of deposits at a bank in the lending country — again, just as already happens for loan transactions outside the euro area. In effect, by cutting off Target2 the ECB will just be helping Greece enforce its capital controls.

Now one potential issue is the foreign obligations of private Greek units. Can they be paid with deposits in Greek banks? Let’s be clear that a negative answer requires a change in the law by the other euro countries — they are the ones that will redenominate, not Greece. But to be safe, Greece should pass a law clarifying that euro-denominated deposits at Greek banks are legal tender for all existing payment obligations by Greek households or businesses. And it would be good to have a sense of the scale of such obligations.

Assuming Greece loses access to Target2, its export earnings, going forward, will take the form of deposits in non-Greek banks or equivalent claims on non-Greek financial institutions. Which leads to…

8. It is critical to ensure that Greek export earnings are available to finance Greek imports. Many discussions of Greek default focus on what are, to my mind, non- or minor problems, while ignoring this major one. [4] If payment for Greek exports takes the form of deposits in foreign banks, as will presumably be the case of Target2 access is shut off, steps must be taken to ensure that those deposits are available for import payments rather being used to finance private acquisition of foreign assets.

Given Greece’s overall near-zero trade balance, access to foreign loans should not be necessary to finance continued imports. But this assumes that export earnings are available to finance imports. There is a danger that exporters will seek to evade capital controls by holding export earnings abroad, manipulating invoices if necessary to disguise noncompliance with the law. This is a serious problem in subsaharan Africa and elsewhere — individuals involved in foreign trade overstate the value of imports and understate the value of exports in order to retain foreign earnings abroad for their personal use. This kind of capital flight can leave a country that notionally has a positive trade balance nonetheless dependent on foreign borrowing to finance its imports. (Ireland is a recent example within the euro area.) The Greek government needs to have enforcement mechanisms to ensure that export earnings are used to finance imports and not to accumulate foreign assets. This should be straightforward where foreign sales are easily visible to regulators, as in tourism or refining, but may be challenging in the case of shipping.

Other European countries will presumably not be cooperative with Greece’s efforts to enforce capital controls. This is a reality that has to be planned for, but it also should be called what it is: Collusion with criminals to steal goods and services from Greece.

9. The government may need to ration foreign exchange. If capital controls are ineffective, or, in the first year or two, if seasonal variation in Greek exports swamps the overall balance, Greek export earnings may be insufficient to pay for current imports for some period, and foreign credit may not be available. This need not be a crisis. But it does mean that the government should be prepared to allocate scarce foreign exchange to particular sectors. The mechanisms to do this are already implicit in the imposition of capital controls. And the centralized allocation of foreign exchange is consistent with….

10. In the long run Greece should learn from the model of Korea and similar late industrializers. (This, also, is the argument for nationalizing the banks, rather than the fact that the “true” value of their assets, in some sense, leaves them insolvent.) Little if any boost to Greece’s net exports should be expected from devaluation. The goal rather must be to channel savings and foreign exchange to sectors that are not currently competitive, but that plausibly might become so. Centralized allocation of credit and foreign exchange is needed to transform the industrial structure, rather than passively following current comparative advantage.

[1] Those requests themselves are largely the result of the hysterical fear-mongering by the BoG and its masters in Greece, the exact opposite of the normal efforts of central bankers to prevent panics. In any case, the rules of the eurosystem give the ECB/BoG almost unlimited discretion with respect to liquidity assistance, so they can’t claim this decision is forced on them.

[2] You can think of a continuum from current membership, to the situation of Cyprus with capital controls, to Andorra which prints its own euro currency but does not have shares in the ECB, to Montenegro which uses the euros as domestic currency without any formal participation, to Denmark which has its own currency but clears balances with euro-area central banks through a Target2 account at the ECB.

[3] The best discussions of Target2 I know of are by Philippine Cour-Thimann.

[4] Here as so often, the political authorities step in to do what “market forces” supposedly ought to be doing but aren’t.

[5] Don’t believe the stories you will hear that this is somehow a necessary or automatic reaction to replacement of BoG leadership. It is not. Countries that are not in the euro at all are still permitted to participate in Target2.

[6] When I was debating this stuff with the very smart Nathan Tankus a few days ago, he brought up the possibility that foreign ATM cards wouldn’t work in Greece, and of an adverse ruling from the European Court of Justice. Oh no!

Shouldn’t even be commenting, your post is way over my head, but…

1. Are you sure Greek T-bills are currently earning just 2-3 percent? The Bank of Greece web site is showing yields north of 8 percent and up to the 20s. Nothing has been below 8 percent all year. 3-5 year yields touched the 2-3 percent range last year, but only for a few months, for most of the year yields were at least twice as high. What am I missing?

2. Are you certain Greece has no primary fiscal deficit? Greece is known for funny accounting. Is the budget still balanced since Syriza took over, what with all the turmoil, cratering economy, possible slumping tax receipts?

3. Are you certain there is no trade deficit? I read there was funny accounting there, too, with cash flows that were just transitioning through Greece being counted as landing in Greece. But I can’t remember where I read that, so maybe I am all wet.

4. Assuming the Greek primary budget is balanced, that’s under austerity. Syriza wants to end austerity and run an expansionary fiscal policy. Can they do that on their primary budget without borrowing hugely? Where will the money come from for that?

5. If they use Greek government bonds to borrow to fund expansionary fiscal policy, can they really do that at low interest rates? If they borrow to raise wages and expand pensions–that’s Syriza’s program– couldn’t that look to lenders like the same policy that led to default?

5. I’m raising all this because Tsipras et al don’t quite look like people who are sitting pretty atop a primary budget surplus and positive trade balance. With the posturing, the negotiations psychodrama, and now the incoherent referendum, they seem like desperate people caught between a rock and a hard place. Maybe the dilemma is that, regardless of existing debt, they still need to borrow a lot of money from Germany to fund their expansionary program, because the Greek economy and primary budget and domestic borrowing resource just can’t handle it. Otherwise, it’s hard to see why Greece doesn’t just cut the Gordian knot and default or restructure as you suggest.

6. The Korean/East Asian development model works great, but it was financed with some kind of austerian means: big trade surpluses, wage restraints, crackdowns on unions, high forced savings rates. Can Syriza really go there given its politics and program?

I like this very much

But controlling this cross border

Payments flow …..

Like collecting elite taxes…..

There’s lots to be said

For revolutionary power

I’m sure you know what happens if the capitalists turn against the state

The petite bourgeois are sure to follow in part

Hell

FDR in the 100 days

Had more control then Syriza has today

Not to be discouraged however

Keeping the euro as the unit of account

And at least in some currency

Along side a scrip

Strikes me as very doable

But really the fist step is a loud

No !

I don’t disagree but it’s important to understand what a trivial part of the problem scrip is. Money is bank deposits. Physical currency is just a device for debiting one deposit and crediting another one. We already use lots of paper instruments besides official currency for this purpose.

The idea of credit money really matters here. Our monetary analysis has to start from the banking system and not from the idea of money tokens of some kind. To “use” or “be in” a particular currency is just shorthand for a set of possible relationships between bank balance sheets.

But really the fist step is a loud

No !

That it is, comrade.

Yes. My idea, which I don’t think has really gotten across here, is to stop thinking about what the Greek government is permitted to do under the current rules and recognize that this is economic warfare. The goal has to be to deprive the other side of its weapons, the most important of which right now is the Bank of Greece.

Where does this lead? Depends on how the creditors respond. But it’s always a good idea to try to think of proposals that can be both a concrete solution to an immediate problem, and a first step toward a more radical transformation.

Great suggestions. Informative post.

Thank you!

Interesting post J.W. What happens to your scenario if euros issued by the Bank of Greece fall to a discount relative to euros from the rest of the Eurozone?

“”And with respect to the external balance, the evidence, both historical and contemporary, suggests that financial markets do not in fact punish defaulters. (And why should they? — the extinction of unserviceable debt almost by definition makes a government a better credit risk post-default, and capitalists are no more capable of putting principle ahead of profit in this case than in others).”

Important point.

From the Guardian’s live feed:

“The BBC’s Robert Peston reports that the Greek government will hold talks with its central bank, and the country’s major commercial banks, tonight to discuss the situation.”

https://twitter.com/Peston/status/617695781986914304

I don’t disagree with any of your specific steps, but I’m really troubled by the conclusion.

Greece has difficulties collecting taxes. It has always has this difficulty. That means there are three options available to it:

1. Cut spending to depression levels.

2. Try to fool creditors via serial default.

3. Inflation — control interest rates so that even substantial levels of debt can be perpetually rolled over or inflated away.

Greece tried option 2 and then went towards option 1, but option 3 is the only sustainable one for Greece.

Greece must be able to collect an inflation tax. Greece needs inflation and cannot live without it until it sorts out its tax collection issues.

To not understand this is to embrace a lie.

This isn’t a moral judgement of the Greek people. Dysfunctional institutions are very hard to reform as they require tackling powerful entrenched interests. The U.S. health care system is dysfunctional but that is not a moral stain on the American people. The only moral stain here is all the lying about what is and is not possible for the Greek economy.

You cannot pretend that somehow the Greek people can have a stable currency while their government is unable to collect taxes.

And everyone has lied here — the Greek government lied to the EU when it joined, the EU lied to the Greek people, the Greek people gave their elected government impossible constraints and their government lied in promising to end austerity while keeping a stable currency. This last lie was probably the most devastating, because in promising that a stable euro was possible, the Greek people hold two mutually inconsistent beliefs, and because of this they hamstring their government officials who don’t have a political mandate to leave the euro.

It is because of this delusional mandate to stay in the Euro that the Greek government was powerless in negotiations with creditors and the human tragedy of austerity became inevitable. Creditors closed the door to 2. The greek people refused 3. Only option 1 was left.

Now you are saying that hey, they can still stay in the euro! More lies.

It’s sad to see this very slow meandering towards a recognition that Greece simply isn’t ready to have a stable currency.

More human misery will follow until the Greeks acknowledge this fact. There is no shame in having dysfunctional institutions and recognizing that you are not able to reform them. There is a shame in thinking that you can have it both ways.

Good post, J.W.

Modern banking is the problem. and we have become super dependent on it. Yet few “get” it.

All Greece has to really to remain good corporate citizens is pay the banks interest and the funds already lodged to be included, and use today as the cut off point, so no more interest growth.

It is not generally understood that the money credited to Greece [and everyone else] is just fiat money electronically marking up accounts in the central bank. This electronic sum is just a number with NO backing by the issuing bank. But it becomes spendable when it gets into the external account.

What debtors, like Greece are being told to do is drain real resources so that when it gets into the banking system, at which point it reverts to electronic money, it can be applied to mark down the loan sum. Eventually it gets extinguished.

This means the banks never get to spend the capital repayment sums. They only go to extinguish the debt. They win only by getting interest, which they can spend on the baks costs,wages etc.

So Greece would be giving the banks everything financially owed just by paying interest. So why not??

They’ll have to bring funds home though, in order to pay people – or transfer the funds to a Greek beneficial owner, which amounts to the same thing.

Is it such a problem if a portion of Greeks and Greek businesses use foreign banks? It relieves the government of the work of supervising them.

Of course, they may/will try and evade tax this way. Tightening up the tax code to levy corporation tax on the basis of real economic activity rather than nominal transactions would help. Say a hotel chain starts booking their sales overseas and their profits slump. At the point, the government audits them and demands all foreign transaction details. If they don’t provide full disclosure and get found out (which they will, in the modern world of whistle-blowers) then enforce a criminal bankruptcy procedure where the business reverts to the state.

I’ve wondered this too — to what extent can Greece simply make sue of banks located elsewhere? One might even say this is possibility is implicit in the whole idea of the euro. But in practice the financial system is far from completely integrated, so I don’t know.