Minimum wages are good for poor people. Here is an important paper from Arin Dube on the impact of minimum wage increases on family income. Using a variety of approaches, he asks what the record of minimum wage changes tells us about how the effects of the minimum at different points in the income distribution. The core finding is that, in his preferred specification, the elasticity of income at the 10th percentile with respect to the minimum wage is around 0.4 – that is, a one percent increase in the minimum wage will raise income for poor families by close to half a percent. This is, to my mind, a really big number – it suggests that pay at most low-wage jobs is tightly linked to the minimum wage, and that criticism of minimum wages as being badly targeted at low income households is off the mark. Tho to be fair, he also finds that minimum wage increases don’t do much for the very bottom of the distribution, where there is not much wage income to begin with. But beyond whatever this ammo this gives for minimum wage supporters, this is a great example of how you should approach this kind of question as a social scientist. The paper gets out of the box of qualitative debates about job loss that have dominated this debate and makes a positive, quantitative claim about what minimum wages actually do.

Why prefund? I’m still trying to finish this interminable paper on state and local government balance sheets. But one of the big things I’ve learned is that the biggest constraint these governments face is not the terms on which they can borrow, but the extent to which they are required to prefund future expenses. The idea that pensions should be fully funded has a solid basis for private employers but it’s not at all clear that the same arguments apply for governments. It’s good to see that some professionals in state and local finance have come to the same conclusion. Here is a new paper from the Haas Institute on exactly this question. It makes a strong case that the requirement to fully fund public employee pensions is costly and unnecessary, and is an important factor in local government budget crises.

Privilege: still exorbitant. Here’s a nice analysis of the international role of the dollar. This is the same argument I tried to make in my Roosevelt Institute piece on trade policy last summer. The Economist says it better:

Unlike other aspects of American hegemony, the dollar has grown more important as the world has globalised, not less. … As economies opened their capital markets in the 1980s and 1990s, global capital flows surged. Yet most governments sought exchange-rate stability amid the sloshing tides of money. They managed their exchange rates using massive piles of foreign-exchange reserves … Global reserves have grown from under $1trn in the 1980s to more than $10trn today.

Dollar-denominated assets account for much of those reserves. Governments worry more about big swings in the dollar than in other currencies; trade is often conducted in dollar terms; and firms and governments owe roughly $10trn in dollar-denominated debt. … the dollar is, on some measures, more central to the global system now than it was immediately after the second world war. …

America wields enormous financial power as a result. It can wreak havoc by withholding supplies of dollars in a crisis. When the Federal Reserve tweaks monetary policy, the effects ripple across the global economy. Hélène Rey of the London Business School argues that, despite their reserve holdings, many economies have lost full control over their domestic monetary policy, because of the effect of Fed policy on global appetite for risk.

… During the heyday of Bretton Woods, Valéry Giscard d’Estaing, a French finance minister (later president), complained about the “exorbitant privilege” enjoyed by the issuer of the world’s reserve currency. America’s return on its foreign assets is markedly higher than the return foreign investors earn on their American assets… That flow of investment income allows America to run persistent current-account deficits—to buy more than it produces year after year, decade after decade.

Exactly right. You can have free capital mobility, or you can have a balanced trade for the US. But you can’t have both, as long as the world depends on dollar reserves.

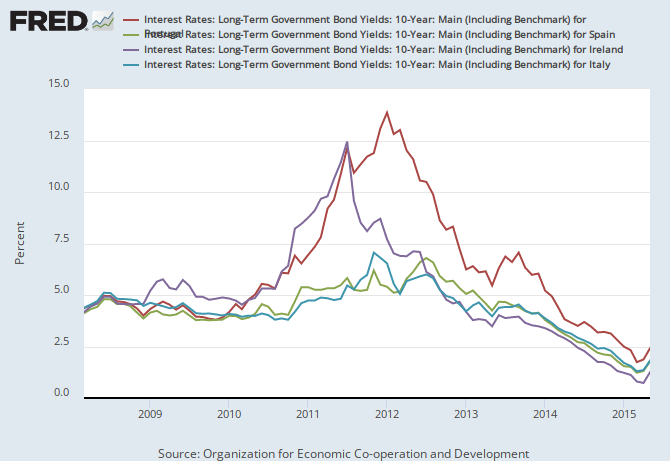

Greece: still a catastrophe. Over at Alphaville, Matthew Klein makes a strong case that Greece’s experience in the euro has been uniquely catastrophic – no modern balance of payments crisis elsewhere has led to anything like as large and as sustained a fall in output and employment. Martin Sandbu objects, arguing that the Greek catastrophe is the result of austerity, not of the single currency per se. Which is true, but also, it seems to me, misses the point. The problem with the euro — as Klein more or less says — isn’t mainly that it precludes devaluation, but that it surrenders authority over the basic tools of macroeconomic policy to a foreign authority — an authority, as it turns out, that has been happy to see Greece burn pour encourager les autres.

The myth of capital strike. I was more on Team Streeck than Team Tooze in their great LRB showdown. But this followup post by Tooze is very smart. Mostly he’s just trying to bring some much-needed order to a complicated set of debates about the role of private finance, credit markets, central banks and the state. But he also scores, I think, a stronger point against Streeck than in the LRB review: Streeck exaggerates the threat of capital strike in modern “managed-money” economies. As Tooze says:

Greece, Spain, Portugal, Ireland even Italy and France all experienced bond market attacks. But this is because they were left by the ECB in a situation which was as though they had borrowed their entire sovereign debt in a foreign currency with no central bank support. … That peculiarity is the result of deliberate political construction. To generalize and reify it into a general theory of capitalist democracy in crisis is highly misleading.

I think Tooze is right: behind the apparent power of the bondholders there’s always either a hostile central bank, or else other, stronger countries.

Things are speeding up here at the end. From Credit Suisse, here is an interesting discussion of longevity of firms in the S&P 500.

There is a general sense that the rate of change is accelerating and that corporate longevity is shrinking. This assertion appears frequently in the business press. Our research shows a more nuanced picture. Indeed, a common measure of corporate longevity, turnover of the companies in the S&P 500, shows that longevity has lengthened in recent years.

A hell of a way to run a railroad. For New Yorkers who are bored of the things they are mad about and want something new to be mad about: The Port Authority capital plan approved this week includes $1.5 billion for Cuomo’s pointless LaGuardia AirTrain. Of course it would be too much to ask that we extend the existing transit system, we have to create a special new system for airport travelers only. But Cuomo’s plan is useless even for them.

Strikes: still declining. Various people have been sharing a graph of strikes “involving 1000 or more workers” on Facebook. I expressed some doubts about this – it’s obviously true that the US has seen a drastic decline in strikes and in worker militance in general, but how well is this captured by a series that only includes the largest strikes? Andrew Bossie replies, showing that for the earlier period where we have more comprehensive strike data, it matches the 1000+ series pretty well. Fair enough.

Welfare is not only for whites. Here is a useful corrective from Matt Bruenig to claims that the welfare state disproportionately serves white Americans. I assume the idea behind these arguments is to disarm claim that welfare is just for “them.” But the politics could cut other way – it’s equally easy to see “welfare goes to whites” as a move to advance the idea that racial justice and economic justice are unrelated, even conflicting, goals. Anyway, whatever it rhetorical uses, we still need a clear and honest assessment of how things work. Which Matt as usual provides.

TPP is dead … or is it? My collaborator Arjun Jayadev has a nice piece in The Hindu (circulation 1.4 million, not far off the New York Times) on the legacy of the late, unlamented Trans-Pacific Partnership. It can be hard to rememebr, amid the shrieks and shudders and foul smells coming from the Oval Office, how destructive and, in its own way, insane, was the pre-Trump liberal consensus for free trade and endless war.

Just give people nice things is a sound basis for policy. “When we decided peoples’ houses shouldn’t burn down, we didn’t provide savings accounts for private fire insurance, we hired firefighters and built fire stations. If the broad left takes power again, enough with too-clever-by-half social engineering. Help people and take credit.”

{kind=link}