TLDR: The value of corporate equity relative to GDP is at a historical high. But this does not necessarily mean there’s a bubble: profits and shareholder payouts are also very high relative to historical values.

I first started thinking about economics thirty years ago, during the (first) tech boom.

This was the era of “irrational exuberance,” the phrase coined by the recently deceased Alan Greenspan and made famous by Robert Shiller. I wrote a review of Shiller’s book of that title for In These Times — one of my first published articles.My first paper in graduate school was a replication of a paper by Brad DeLong and Larry Summers1, which argued that seemingly excessive stock valuations could be explained by rational investors extrapolating recent earnings growth into the future.

All of which is seeming at least a little bit relevant today.

Between the start of 1995 and the end of 1999, the price-earnings ratio for the S&P 500, as measured by Shiller, more than doubled, from 20 to nearly 44. Then over the next three years, it fell back nearly as far. Today, price-earnings ratios by the same metric are just shy of 40, not far from the peak of the first tech boom. Everything old is new again, it seems. (Except that, as Paul Krugman notes, people generally liked the products of the first internet companies.) So the obvious question is whether this is also a bubble — whether the second half of the late-1990s story will get a rerun as well.

There are many people out there with highly specialized expertise whose whole job is to think about stock valuations. I am not one of those people! If you are looking for investment advice, you have come to the wrong blog.

But I do think I have something to add.

Most of what makes financial-analyst jobs hard has to do with specific companies and specific markets. Things get easier when we are looking at the stock market as a whole. (And that is where my own background in heterodox macro is more likely to help.) When we are talking about corporate equity in the aggregate, rather than individual securities, some arithmetic comes into play that helpfully limits the space of possibilities.

One way to think of a share is that it gives a claim on future payments by the corporation that issued it. This is not all that a share is — as Arjun and I stress in Against Money, it’s important to keep sight of financial assets’ existence as concrete objects with their own specific properties, and not reduce them to simply a future cashflow. But certainly the cashflow it gives claim to is one very important property of a share.

Again, the value of share is not reducible to present value of expected (in either the statistical and/or psychological sense) future payments. But those should act as an anchor. Unless we have good reason to think there is a change on value market participants put on future payments, we should expect share prices to vary roughly in proportion to them. And even if we think valuation of shares can vary indefinitely with respect to payments they give claim to, it’s worth knowing how much of current share prices would have to be explained in these terms, and how much can be explained by variation in the payments.

In the rest of this post, I am going to look at the US nonfinancial corporate sector. This means excluding the 20-25% of corporate equity issued by financial businesses, and including closely-held corporations as well as those listed on public exchanges. This is mainly because that’s the universe for which it’s easiest to get consistent data. But I also think it’s a reasonable thing to be interested in substantively.

*

If we look at nonfinancial corporate equity over the 80 years since World War II, here is what we see:

The figure shows the total value of nonfinancial corporate equity,as a share of potential GDP. (I am skeptical of potential as a measure of actual economic potential, but here it is just functioning as a trend, to smooth out short-term changes in the denominator.) This, I would argue, is the most straightforward measure of the value of the stock market in broad social terms — how much claim wealth in this form gives on social labor and its products.This is also, of course, the metric used by Piketty.

As the figure shows, stock market value in that sense has had three long upswings. The first peaked in the late 1960s at 0.9, the second in 2000 at 1.6, and the third is ongoing, with the ratio currently at 2.3. (The data in this post is drawn from the Fed’s Financial Accounts, and goes through the first quarter of 2026.) Over the long run, there is a clear upward trend, especially over the past 15 years. (The dotted line shows the post-WWII average.) By this metric, the current stock market boom has now run well ahead of the late 1990s one.

How should we think about this?

Logically, the value of corporate equity relative to GDP must reflect a combination of four factors: value added in the corporate sector as a share of GDP; corporate profits as a share of their value added; payouts to shareholders as a percentage of profits; and the value placed by markets on each dollar of payouts.

In other words, if corporate stock is worth more relative to GDP, that can be either because more of GDP is now happening in the corporate sector; or because more of the income from that activity is going to profits; or because more of those profits are being paid out to shareholders (rather than retained in the firm); or because financial markets place a greater value on each dollar of payment. Or of course some combination of those.

As with any accounting identity applied historically, it is useful insofar as it corresponds to (1) categories in the relevant data, and (2) distinct causal factors we believe to be at work.

For the first term, we are, again, using all nonfinancial corporate equity, which includes closely held as well as publicly-traded corporations, and the BEA’s estimate of potential GDP. (Both are in current dollars.) Value added is defined, as usual, as sales less the cost of non-labor inputs. Profits are after tax (and of course also after depreciation); conceptually, these are the funds potentially available for distribution to shareholders.2

Payouts I am defining as dividends less net new equity issues. That share repurchases are conceptually equivalent to dividends is not, I think, too controversial at this point (though it creates a lot of headaches). We are also adding shares retired through cash acquisitions, and subtracting shares issued whether in IPOs or otherwise. This might seem odd at the level of an individual firm, but at the aggregate level these other flows seem clearly equivalent to buybacks and dividends. If firm A buys up all the shares in firm B for cash, that is a payment from the corporate sector to shareholders, just as if firm A were buying back its own shares. Similarly, new shares issued are a reduction in the aggregate payments from the corporate sector to shareholders just as a reduction in dividend payments would be.

It might sound strange to define IPOs (whichgenerally are quite exciting for stock market participants) as equivalent to dividend reductions (which generally are not.) But this is where the aggregate perspective matters. Shareholders as a whole already own all the equity of the corporate sector as a whole. An IPO is a payment from shareholders to the corporate sector, exactly like buyback is a payment from the corporate sector to shareholders, without in either case any change in aggregate ownership rights. Or looking at it from another point of view, new corporations are in general competing with existing firms;the profits flowing out to shareholders of the new firm are to a first approximation deductions from the profits flowing to claimants on existing firms. Nice for the shareholders in the new firm, if it succeeds; but no use to shareholders as a class.

Finally, the valuation term asks, in effect, what is the market price of a dollar of income from the corporate sector. It’s analogous to the price-earnings or price-dividend ratios one sees at the level of individual corporations or indexes, though not identical given the nonstandard (but, I would argue, appropriate) way I have defined payouts. Here it also functions as the residual term, reflecting any change in the value of equity not explained by the other factors.

The figures below show the values of each of these terms over the past 80 years. What do we see?

We will start with the first term, corporate value added as a share of GDP. This shows how much of economic activity takes place in the corporate sector, and is potentially available for shareholders.

As it turns out, the corporate value added term does not do anything interesting. Yes, it is modestly lower (around 50 percent) after 2000 than its average in the earlier decades (53 percent), suggesting that all else equal, we might expect the value of corporate equity to be slightly lower relative to GDP in the 21st than in the 20th century. But this change is very small compared with the movements in the other terms. This factor might be important if we were comparing the US to other countries, but it is not part of the story here.

Next, profits:

Profits as a share of value added shows much more variation, falling by half in the 1980s, then rising in this century, in two big jumps — one after 2000 and the second over the past five or so years. While the corporate share of GDP doesn’t vary by even 10 percent over the whole period, profits as a share of value added are fully three times greater today than they were for much of the 1980s.

The third term is payouts.

Payouts (as I’ve defined them) also show large variation, rising from a bit under 40 percent of profits in the early decades to over 80 percent in more recent ones. The timing here is a bit different — though there is plenty of short-term variation, the long-run shift happens in a single big jump in the early 1980s. (This was the topic of an essay in my dissertation, which I never managed to publish as an academic article but did turn into a report for the Roosevelt Institute.) This term gets relatively little attention in discussion of stock prices, but it seems to me that it is as fundamental as profits to any discussion of long-term trends in the value of corporate equity.

Finally, the valuation term shows a lot of short- and medium-term variation but, perhaps surprisingly, no long run trend. Today’s ratio of around 40 is close to what we see in the 1950s and 1960s.

Again, what we are measuring with this last term is the ratio of equity value to shareholder payouts, including net share repurchases. The big spikes in the early 1970s and in 2000 are because those years saw exceptionally high new equity issues, which means very low payouts by my metric, and therefore very high ratios of equity value to payouts.

It is more common to talk about equity in relation to earnings, on the implicit assumption that profits are of equal value to shareholders whether they are paid out or not. I’ve shown this latter ratio below. But personally, I do not think that that is a good assumption. Shareholders evidently care a great deal about payouts — why else would companies pay dividends and make share repurchases? I think it is important to distinguish between corporations and the shareholders who exercise claims on them — the former are not simply the personal property of the latter. From this point of view, it is more natural to talk about valuation in terms of the price shareholders place on the income they actually get from corporations, as opposed to the underlying profits.

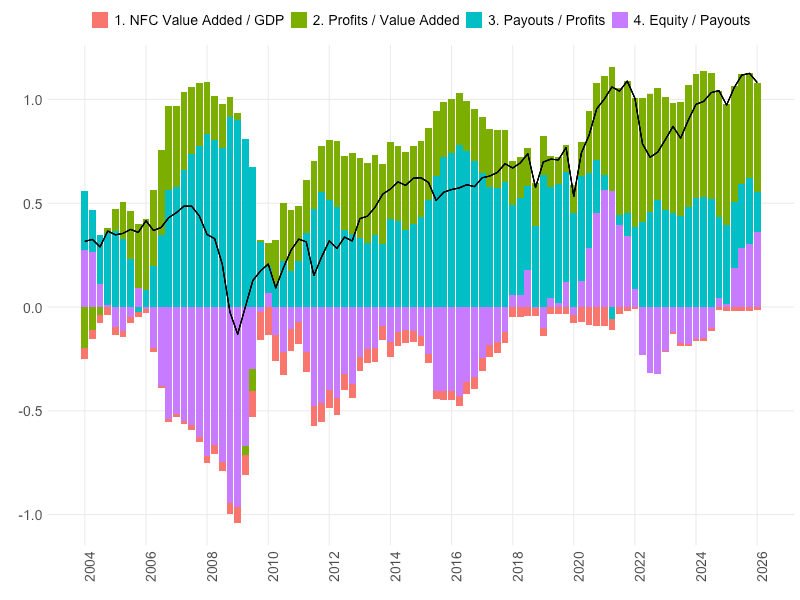

All of these series (except the last one) are combined in the next figure, which is really the whole point of this post. If you take one thing from one I’ve written here, this picture is it.

Equity value relative to GDP and its components, 1947-2026:

For this figure, I’ve converted the values to logs. This has the big advantage of converting the multiplicative relationship to an additive one, so that we can visually see the contribution made by each of them. But it can make interpreting the figure a bit tricky. Here, zero is the average value over the full period; positive one is a value about 2.7 times greater than the average, while negative one is a value about one-third of the average. The black line similarly describes the deviation of the equity-GDP ratio from its full-period average; the heights of the bars correspond to the contribution each term makes to that deviation. The data is quarterly; for all the terms except equity, I use rolling one-year averages.

As we can see, the log of the equity-GDP ratio is currently about 1.1 above its long-run average, corresponding to a value nearly three times greater. (2.2 today, versus a long run average of 0.85.) Just over half of this (0.53) is explained by higher profits relative to value added, 0.19 is explained by higher payouts relative to profits, and 0.36 is explained by the valuation term.

So already we can see that a simple explanation of today’s high equity values is going to be incomplete. Relative to the long-run average, we have three distinct factors each of which explains a significant share of today’s higher values.

Another thing that jumps out from the figure is that the previous historical peaks in equity values reflect quite different mixes of these components.

In the 1960s, profits as a share of value added were, for a while, well above average, though not as high as today; but the fraction of those profits flowing out to shareholders was much lower. Thus the much lower ratio of equity to GDP, despite comparable valuation ratios.

In the late 1990s, profits as a share of value added were much lower — less than 5 percent at the height of the tech bubble, compared with 10 percent in the 1960s and 15 percent today. But the fraction of profits paid out to shareholders was historically high, averaging over 100 percent for the 1998-2000 period. It’s worth noting in this context, also, that the collapse of equity value in the 1970s reflected a fall in shareholder payouts much more than in profitability; this is perhaps important context for the shareholder revolt that followed.

The big takeaway from this decomposition is that we should be cautious about assuming the stock market is overvalued — that we’re in a bubble, that this is another bout of irrational exuberance — simply because equity prices are high relative to the historical norm. Shareholders have it better than the historical norm, too. Corporations are more profitable. And more of those profits are flowing out to them. A bit of exuberance might be rational, under the circumstances.

On the other hand: If we focus on just the past 20 years, as in the figure below, the picture looks a bit different.

Yes, both profits and payouts are high relative to their long-run averages; but those shifts mostly came earlier, while the big rise in equity prices is more recent.Apart from the relatively brief collapse in profits during the Great Recession, almost all the variation in equity prices over the past two decades comes from the valuation term, rather than changes in the underlying payments to shareholders.

This is even more true over the past two years — equity values have increased sharply while profits have been stable and aggregate payments to shareholders have fallen, as dividend growth has stalled and net equity issue has turned positive.As a share of GDP, the net payments flowing from corporations to shareholders today are very close to where they were a decade ago; but corporate equity is worth 60 percent more. It’s hard to avoid the conclusion that either equity was undervalued in the mid-2010s, or it is overvalued now.

So which side do we focus on? Over the long run, most — tho not all — of the increase in the value of wealth in the form of corporate equity, is explained by what we might call fundamentals — the flow of payments to owners of that wealth. Over the short to medium run, on the other hand, almost all of the increase in the value of equity comes from valuation, and whatever financial-market dynamics drive that. Or as the old saying goes, in the short run the market is a voting machine, but in the long run it’s a weighing machine.

*

I want to say a bit more about the profits and payouts parts of the picture.

That high stock prices reflect to some extent a high level of corporate profits seems to be reasonably well understood, at least based on recent coverage in the Financial Times. This of course does not mean that high stock prices are justified, or sustainable; it just shifts the question to how justified or sustainable the high profits are.

This goes double to the extent that high valuations are based on an expectation of further increases in profits, as this recent FT piece suggests:

Wall Street’s expectations for company profit growth are rising at the fastest pace since the post-pandemic rebound, fuelling concern that an “earnings bubble” could be forming in the estimates that have underpinned the US stock market’s rally.

Analysts are now forecasting a 25 per cent increase in S&P 500 company earnings for the coming year, according to Bloomberg data, boosted by a resilient US economy and the AI boom.

However, just ahead of the second-quarter earnings season, some investors are growing concerned about the speed at which analysts’ estimates are rising…

This Alphaville piece goes further, saying that “supernormal profits are unsustainable, because they always are.” I don’t know about that. I don’t know if there’s any reason to think the profit share is stationary, to use the statistics jargon — apart from a dip in 2008-2009, profits as a share of value added have been greater than their long-run average in every year of this century, and seem to be getting farther from it. Capital really has won some lasting victories in the class war.

That is one natural way to look at profits — as a distributional variable. But there’s another way of looking at them, from the demand side.

We know, as readers of Keynes, that an increase in investment automatically creates an equal quantity of additional saving. If, furthermore, there’s little or no incremental saving out of wage income (a reasonable assumption, in my opinion) and if the fiscal balance and trade balance don’t change significantly (perhaps less reasonable, but we’ll go with it) then this additional saving must take the form of an increase in profits. This relationship is often known as the Kalecki-Levy profits identity, and is one bit of heterodox economics that has established a foothold in finance and the businesspress. The same identity says that an increase in the fiscal deficit or trade surplus should similarly lead to an equal increase in aggregate profits.

Exploring the math of this and the extent to which it is a reasonable first approximation of real-world dynamics would be an interesting exercise for another post. But it raises another point which I think is very relevant for thinking about the current situation: Even if the AI companies themselves are not particularly (or at all) profitable, AI-related investment spending is probably an important factor in raising aggregate profits. Just like the California gold rush generated plenty of profits for somebody, even if the vast majority of prospectors themselves went broke.

Or as this recent FT piece puts it:

The AI boom is lifting the fortunes of hundreds of formerly drab industrial, utility and mining companies as investors turn to the “picks and shovels” needed to build and power vast data centres. …

The companies benefiting include Caterpillar, best known for construction equipment but now supplying generators for data centres, 150-year-old German engineering company Hochtief, which will enter the Dax later this month, and Nucor, a steel supplier that has credited “white hot” AI demand for a “tsunami of earnings power”. …

The vast amounts of electricity needed for AI training are also fuelling demand for specialised power management, high-voltage electronics and cooling technologies. This has led to big interest in traditional suppliers of electrical equipment…

You could think of it like this: As long as there is strong investment demand and easy financing for it, the profits will be there …. but not necessarily for the companies carrying out the investment and getting the financing.

And this, perhaps, is the point where the macro perspective needs to give way to the micro one. Because it may be that, yes, in the aggregate, an ease in financing brings forth additional investment, which generates enough profits to justify the initial financing. But debt must be paid back not in the aggregate, but by the specific companies that incurred it. If the investment is one place and the profits are somewhere else, then at some point somebody’s survival constraint is going to be violated.

And I think I will end this post here.

I very much want to discuss the payouts piece of the equation, which in my mind is as important as profits, and much less discussed. But this post is already too long, and has taken much too long to write. So the payouts piece should be along, well, if not this month, then next month, or soon.

The following is a somewhat expanded version of testimony I presented on June 23 before the New York City Commission on Government Efficiency.

My name is Josh Mason. I am an associate professor and chair of the economics department at John Jay College, CUNY, and a senior fellow at the Groundwork Collaborative. It’s a pleasure to address the Committeeon Government Efficiency, several of whose members I worked with back in my days as the Policy Director of the New York Working Families Party.

I am here today to speak in opposition to any measure to create stricter rules for the use of City reserve funds, or to enshrine limits on reserve-fund withdrawals in the New York City Charter. I believe that the City needs greater short-term flexibility in budgeting, not less.

Economics suggests two broad principles for thinking about the City budget position.

First, over the long run, growth city expenditure needs to match growth in revenue. Unlike the federal government, the city cannot run deficits indefinitely, nor can it use long-run debt to fund current expenditure.

Second, over the short run, adjustments in response to unexpected shocks to revenue or program costs should fall on those areas of spending with the greatest intertemporal substitutability. In other words, when faced with a mismatch between current revenues and current expenditure, the adjustment required in order to bring them into balance should as much as possible fall on those budget items for which a dollar of spending next year is a close substitute for a dollar of spending this year.

The first of these principles, presumably, is accepted by everyone here. The second one is less familiar. But it is also implicitly accepted by everyone when it comes to periods of a year or less.

New York City, like many governments has very large short-term fluctuations in revenue. Between quarters, the average change in tax receipts is 13 percent; the average change in total receipts is 10 percent. It is not unusual to see total City revenues fall by 10 percent from one quarter to the next, or to see tax revenues fall by as much as 15 percent over a quarter, as they did between the first and second quarters of this fiscal year. 3 (See Figure 1.)

Figure 1. Source: New York City Comptroller, New York City Quarterly Cash Report; and author’s analysis

No one believes that short-term variation in the timing of city receipts should lead to city departments cutting (or increasing) spending by 10 or 15 percent, simply because relatively little tax revenue comes in the second quarter compared with the first. Everyone, I think, agrees that these short-term fluctuations should be entirely absorbed on the city’s balance sheet via short-term borrowing or changes in the city’s cash holdings.

That is not controversial. But what I would add is that, economically, there is no sharp line separating periods of less than a year from periods of more than a year. The same logic that tells us that variations in revenue or program costs over the course of the year should be entirely absorbed on the balance sheet, suggests that variation over a period of few years should also be primarily absorbed in this way.

It is true that the timing of tax revenue means there are greater fluctuations in revenue from quarter to quarter than from year to year. But the city still faces substantial variation in revenue from year to year, much of which is temporary. In recent years, we’ve seen city revenues increase by over 10 percent in some years, by as little as 1.5 percent in other years. It is far preferable to see spending rise steadily at the average rate of revenue growth, than to have big increases in spending in some years and cuts in real terms (which a 1.5 percent growth in spending would be) in other years, in an effort to achieve balance in each fiscal year. Variation in revenue from year to year is often temporary, and reverses the next year; and even if slower revenue growth turns out to be persistent, a gradual adjustment to the new situation is almost always preferable to an abrupt one.

Again, this principle is well understood at the level of practical budgeting. That is the reason that the city has reserve funds in the first place. And it is why, historically, the city has often used surpluses to prepay future years’ expenses rather to increase spending. 4

The items in the city budget that are most intertemporally elastic — most substitutable between one year and the next — are fund contributions. A dollar contributed to the fund next year is almost as good as a dollar contributed this year. 5 If we were to contribute nothing to a given fund this year, and double the contribution next year, the overall funding position would be almost the same. In general, if the total contributions over some period are unchanged, there is very little economic cost to shifting those contributions around in time.

This is much less true of other city expenditures. If we were to shutter the city’s libraries this year, and double library spending next year, the overall value of library services provided to the public would be far less than with a stable level of spending. Additional hours of libraries open next year are a very poor substitute for hours the libraries are closed this year. The same goes for fire and police services, education, and most other public services.

In principle, capital expenditures are more substitutable — a major road improvement, say, is almost as valuable if it is carried next year as this year. But in practice, the process by which projects are approved makes them hard to shift around in time — a project that has passed all the necessary hurdles to go forward in one year cannot necessarily be deferred to a later year or advanced to an earlier one. So in practice, the least costly way to address unexpected changes in City revenues or program costs is via contributions to or withdrawals from the city’s reserve funds — a category in which I would include the Retiree Health Benefit Trust and the Budget Stabilization Account as well as the Revenue Stabilization Fund and General Reserve.

The proposals to mandate contributions to the reserve funds and limit withdrawals from them would reduce this flexibility, and create greater instability in other categories of city spending. Perversely, they would force the burden of adjustment onto budget items that have less intertemporal substitutability. This is the opposite of what we should be trying to achieve. The budget needs more short-term flexibility, not less.

A number of these proposals involve formulas that are intended to allow flexibility when economic conditions warrant it, but not otherwise. For example, a recent proposal from the Comptroller’s office suggests that except in the event of natural disasters or similar catastrophic events, withdrawals from reserves should be permitted only once there have been two quarters of declining employment in the city. 6

Since the idea of tying withdrawals to economic conditions may seem appealing, I want to explain why it is not a workable solution in practice. There are four reasons, in my view, why hard rules based on economic data are not a practical solution.

First (as the Comptroller’s proposal acknowledges, but other similar proposals do not), reliable macroeconomic data is often unavailable in real time; most economic data is subjectto substantial revisions which can dramatically change the initial numbers.

For local employment, the final data are not released until a full year after the period which it covers, and are often quite different from the initial data.For example, in 2025, the jobs data as initially released showed a respectable gain of 50,000 jobs over the year. But the numbers have been subsequently revised downward and the most recent numbers show no job growth over the year at all. (See figure 2.)

Figure 2. Source: Bureau of Labor Statistics, State and Metro Area Employment, Hours, and Earnings; and author’s analysis

This does not mean that we should not use the most current economic data, of course. But data whose final value is not available until a year after the fact, and where the initial release may be very different from the revised value, needs to be used cautiously and weighed alongside other evidence on the state of the economy. It is not a suitable basis for imposing hard rules on the city budget.

Second, while national economic data is available sooner than for local areas, these are also unsuitable for budget rules, since business cycle dynamics in New York City can be quite different from national dynamics. For example, the 1990 recession was quite mild at the national level — employment fell by only about 1 percent and had fully recovered within two years of the end of the recession. But in New York, it was much more severe, with fully 10 percent of jobs lost and employment not returning to pre-recession levels until a decade later. This was also the case for the 2000 recession. The 2007-2009 recession, on the other hand, was milder in New York City, with employment returning to pre-recession levels two years after the recession ended, compared with five years nationally. So a rule based on national economic data may be a poor fit for local conditions.

Figure 3. Source: Federal Reserve Bank of St. Louis

A rule based on recessions, which has also been suggested as a trigger for drawing down reserve funds, combines both of these problems. The National Bureau for Economic Research often does not announce recession turning points until a year or more after the fact, and the timing of downturns may be significantly different at the local and national levels.

Third, even if we had reliable data, economic indicators do not move in sync, and it is not always obvious which is the appropriate one to use.

For New York City, as for most local governments, the single most important source of revenue is the property tax,which in recent years accounts for between 40 and 50 percent of all City tax revenue. Property tax receipts depend on property values, and these can move quite differently from employment or output. For example, while the 2007-2009 recession was, as noted, fairly mild in New York in terms of employment, home prices saw a steep and lasting fall — average New York home prices were lower in 2017 than they had been a decade earlier in 2007. (See Figure 3.) Given the city’s reliance on property taxes, this is arguably more important than employment conditions. A rule based on employment would not necessarily give a good sense of the economic conditions that are most relevant for the city budget position.

Finally, in practice, data-based rules create arbitrary cutoffs and thresholds. The nature of rules is to impose hard binaries — either withdrawals from the reserve funds are permitted or they are not. But in practice, economic conditions may be quite similar in periods when the threshold is not quite reached as in periods when it is, and whatever indicator is used as the basis of a rule will, in reality, only be one of many pieces of information relevant to economic and budget conditions. Policymakers in the moment can weigh various considerations to decide whether it is appropriate to draw down or to add to reserves; a predefined rule does not allow this flexibility.

More generally, advocates of rules for city reserve funds need to grapple with the full implications of such rules. The city will, inevitably, face unforeseen changes in its revenues and in the cost of the services it provides. The impact of these changes must be absorbed somewhere in the budget. Given the city’s limited ability to control its revenue, especially in the short run, shocks that are not absorbed in the balance sheet will in general, be absorbed by changes to the level of city services provided.Ensuring a steady rate of contributions to the employee retiree health benefit fund sounds like a good thing, in isolation. But, obviously, stable contributions to the fund do nothing to reduce instability in city revenues or program costs. So a rule imposing a more stable path of contributions to the fund necessarily imposes more instability elsewhere in the city’s budget. And cutbacks to funding for the school system, or for public safety, will have persistent costs that cannot be made good in future years in the way that a shortfall in fund contributions can be.

A myopic focus on stabilizing contributions to city trust funds (which is of course desirable in isolation) can blind us to the very large costs of instability in the provision of public services. It is certainly true that the City, unlike the federal government and even more than the State, is constrained in its ability to issue debt, and cannot fund ongoing deficits through new borrowing. Nor, of course, can the city’s financial assets be spent down indefinitely. In this sense, it is absolutely correct that public expenditures must be managed so as to keep them in line with revenue growth over time. It is unfortunate, however, that the idea of responsibility has been narrowed to mean only a focus only on financial outcomes, and not on the no less critical responsibility for consistent provision of the public services that New York’s residents and businesses depend on.

Even short-term reductions in the provision of education, public safety, transportation, health and other services can have lasting effects. Among other things, public services are directly relevant to decisions by both families and businesses about whether to move to, or remain in, the City, and thus have important consequences for the City’s future tax base. When faced with a tradeoff between consistent contribution to city reserve funds and consistent provision of public services, the former has no better a priori claim to be considered the “responsible” course than the latter.

A related mistake, in my view, is the idea that policymakers will systematically err on the side of overspending unless restrained by hard budgetary rules. Both common sense and history suggest that while this sort of error certainly occurs, there is no reason to think it is any more common than the opposite error, of excessive resort to spending cuts to close budget gaps and insufficient use of balance-sheet flexibility.

There is no reason to assume policymakers will systematically err on the side of irresponsibly drawing down reserves; it is just as plausible that they will underutilize them. This is clearly the case at the state level, where the State made no drawdownsfrom the Tax Stabilization Fund or Rainy Day Reserve Fund in either the 2000 or 2007-2009 recessions despite substantial falls in tax revenue, instead resorting to other, more costly measures to close the state budget gap.7 In general, there is no reason to think that today’s policymakers, who would impose this rule, are any more likely to strike the right balance between the balance-sheet position and public service provision than the future policymakers who would be bound by it. The one thing we know for sure is that future policymakers will be better informed about future economic and budget conditions than we are today.

To be clear, I think the existence of city reserve funds is a very good thing. Given the constraints on city borrowing, adequate reserve funds are essential to maintaining stable provision of city services in the face of unexpected shocks.It is appropriate for the City to contribute more to these funds in years when revenues are usually high, while drawing them down in years when revenue growth is weaker. And it may well be that the ideal funding of city reserves is greater than it has been historically.

There is nothing wrong with thinking about guidelines or targets for reserve funds. What I urge you to reject, however, is enshrining a hard limit on the use of reserves in the City Charter. The goal of maintaining reserves should be to provide future administrations with greater flexibility, not less, in responding to future challenges.

(I had a long conversation yesterday with Eric Levitz of Vox about the New York City rent freeze and the economics of rent regulation. I have posted the interview below just as it appeared there, for my archives and in case people want to read it without dealing with the paywall.)

An economist makes the case for Zohran Mamdani’s rent freeze

A new look at an issue that frequently divides voter and experts.

As America’s housing crisis deepens, policymakers are increasingly turning to an old idea for improving affordability: making large rent increases illegal.

In recent years. Oregon,Washington, and California have enacted statewide rent controls. In 2024, the Biden administration floated a nationwide cap on rent increases for large buildings. And last month, New York’s Rent Guidelines Board approved a two-year rent freeze on the city’s roughly 1 million stabilized units, fulfilling one of Mayor Zohran Mamdani’s signature campaign promises.

While rent control has long had some appeal to voters, it has historically provoked consternation among economists. In one 2012 survey, just 2 percent of economists agreed with the statement that local rent regulations “had a positive impact over the past three decades on the amount and quality of broadly affordable rental housing.”

The reasoning behind such skepticism is simple: When you make it less profitable to provide rental housing, people produce less of it. As a result, rent control reduces the supply of housing — and thus tends to make cities less affordable in the long run.

But this orthodoxy may soon be overturned – or so argues J.W. Mason, chair of the economics department at New York’s John Jay College of Criminal Justice and a senior fellow at Groundwork Collaborative, a progressive think tank.

In Mason’s view, the evidence that rent regulations discourage construction has been widely overstated: When designed well — and paired with zoning reforms — rent controls can protect tenants from displacement without reducing the long-term supply of housing.

We spoke this week about the case for (and against) rent control in general and New York City’s policies in particular. Our conversation has been edited for clarity and concision.

Among mainstream economists, conventional wisdom holds that rent control measures are misguided, partly on the grounds that they reduce the long-term supply of housing. In your view, what does that analysis get wrong?

When we talk about rent regulation, we’re typically talking about markets where there are already very substantial constraints on housing supply. Nobody is trying to pass rent regulation in exurban Texas or the Atlanta suburbs, where you have a lot of new housing construction.

Where it’s relatively easy to build housing, rents are going to be closely tied to the cost of building and operating new housing because, if you charge a lot more than that, then you create an opportunity for competitors.

The markets where you have rent regulation are markets like New York City, San Francisco, and a lot of European cities — places where there’s already really hard constraints on the capacity to build new housing. And in cases like that, where supply is already constrained by land use rules or just by an absolute scarcity of buildable land or by other factors, you’re not going to get any additional limitation on supply from rent regulation.

In that context, owners of existing housing collect rents in the broad, economic sense — income that doesn’t derive from any contribution they’ve made to production, but merely from others’ inability to build. Under those conditions, the only thing rent regulation does is redistribute some of that economic rent from property owners to tenants.

Most critics of rent control oppose restrictive zoning too. So, I think they might say that we should focus on ending the conditions that allow landlords to extract economic rents in the first place, rather than on redistributing them.

There’s an argument that, if we could achieve deep supply-side improvements in housing, we wouldn’t need rent regulation to the extent that we currently do. And I think that’s a perfectly reasonable argument. But it does not do any good for tenants who are facing displacement today. The fact that you have a different long-term goal does not remove the need for dealing with the short-term problem.

And there are good reasons to think that rent regulation is desirable, even if we think the real problem is on the supply side. For one, I think the politics of dealing with supply issues are much easier if you also have rent regulation. A lot of opposition to addressing supply-side problems is a perception that if you get new development, then that’s going to lead to displacement of people in the areas where development is taking place.

We can debate how true that is. But it’s a very deeply held perception. So, to the extent that you can offer real security to existing tenants, you remove one of the big sources of public opposition to supply-side measures: You don’t need to oppose removing restrictions on new housing because you are locked in. You are safe. Your landlord cannot kick you out to get somebody higher-paying in.

And honestly, I think that politics is very clear here in New York. I think that you would not have gotten the City of Yes land-use reforms, or the zoning reforms that passed on the ballot initiatives this past year, or a progressive like Zohran Mamdani coming out in favor of supply-side measures to increase housing production, if we had not strengthened the rent laws back in 2019.

Putting the politics to one side, do you think there is any tension between restricting rents and increasing construction? Say a city rolls back some of its restrictions on homebuilding, and new construction stops being effectively capped by zoning rules. If that city adopts rent controls, will that reduce the supply of housing at the margin? Or is that supposed tradeoff entirely illusory, in your view?

There’s no deterrent effect to many rent regulations, including those in New York City. Obviously, you can hypothetically imagine a much more rigorous form of rent control that could discourage new construction. I’m not going to say that it is impossible for that to happen. I think that we’re just very far from that point.

This is largely because new construction is typically exempt from rent control. In New York City, you are only required to comply with rent regulations if your building is more than 50 years old. And developers aren’t deciding whether to build based on how much rent a project will yield 50 years in the future.

The longevity of housing just makes it different from other goods. People often say, “If you impose a hard cap on milk prices, people will find it less worthwhile to produce milk. And we’re going to have shortages of milk in the stores.” We can debate whether that’s always true. But it’s a reasonable argument, since milk is consumed shortly after it’s produced. So your decision to produce more milk really is based on the price that you can get for that milk today.

But housing is at the opposite extreme. The median building in New York is 80 years old. When that housing was first produced, the price it’s going for today was not a factor.

Now, I should add that in New York City, the buildings with the highest rates of rent regulation are actually newer buildings. But that’s because developers voluntarily opt into the rent regulation system, as a condition of getting tax subsidies. At that point, clearly you’re not having a negative effect on supply when this is a voluntary decision.

Is that necessarily true? In theory, the tax subsidies are supposed to encourage housing investment. And developers weigh the benefit of those subsidies against their costs: If you accept them, you need to provide some units at below-market rates. So, if New York City makes providing rent-stabilized units less profitable — by freezing rents — then don’t the subsidies become less valuable? And wouldn’t that theoretically make investors slightly less inclined to fund new housing, all else equal?

Well, we’re seeing more new housing constructed in New York City right now than we’ve seen in many decades. So clearly something is working. And maybe what’s working is just that incomes are rising, that demand for housing in the city is rising.

But in my opinion, the tax abatements are badly structured. I really would not support housing development that way. But a huge fraction of new housing that gets built in the city uses these tax credits. So I think clearly they’re attractive to developers. Clearly, it’s a worthwhile trade-off from their point of view.

For critics of rent control, one study looms especially large: In 2018, a team of Stanford economists examined the impact of San Francisco’s rent control expansion in the 1990s. And they found that the policy led to a 15 percent reduction in the rental housing supply, which pushed up rents in the city by 5.1 percent. But in my understanding, you think the implications of that research are widely misinterpreted.

Yeah. I think that’s really a study about poor regulatory design. What it shows is: If you impose strict rent regulations but you don’t restrict people’s ability to convert rental properties to other uses, that may encourage landlords to convert rental housing into condos.

In the study, rental housing supply did not fall because of a decline in new construction. It fell because of condo conversions. And that distinction is important. If you have rental housing that’s converted to condos, that’s not reducing the overall supply of housing, but only that of rental housing. And it’s not necessarily increasing the cost of housing: It may be increasing market rents in the unregulated sector, but decreasing the cost of condos for condo buyers.

In any case, a well-designed rent regulation, like New York City’s 2019 reforms, can simply disallow people from moving housing out of the rental market in that way.

Many have argued that rent stabilization in general and New York City’s 2019 reforms in particular have negatively impacted the quality of the housing stock. Specifically, the argument is that landlords respond to rent restrictions by cutting back on maintenance. Is that a serious risk?

Of all of the concerns that you’ve raised, that is the most legitimate. I don’t think that we’re really seeing that yet. If anything, we’re seeing a reduction in a number of units that seem to have severe maintenance problems in New York. But you know, some people think we should not just have a rent freeze here, but a rent rollback. So, you roll back rents by five, 10, 15, 20, 25 percent, you’ll eventually reach a point at which you have real problems with building owners not doing basic maintenance and buildings falling into disrepair.

I’m not sure what the number is. Clearly there is a number where that happens. But I think we’re a very long way away from that. The vast majority of buildings are renting for much more than their operating and maintenance costs. The Rent Guidelines Board does studies. They suggest that the median margin is on the order of 40 or 50 percent.

As you’ve written, there is a minority of stabilized buildings in which maintenance and operating costs already exceed their total rents. But you attribute that primarily to the poverty of such buildings’ tenants, rather than to excessive restrictions on market rents?

I think that’s generally the case. There’s a sector of nonprofit-owned buildings, which tend to be the ones with the lowest rents and the lowest-income tenants. And in many cases, those buildings do face real problems with maintenance and upkeep. But they’re often not increasing rents even by the regulated amount, since tenants in these places simply can’t afford to pay more. In those cases, I think at some point you need either targeted subsidies or a change in ownership. But this is a very small fringe of buildings.

To name one last criticism of rent control: Some economists argue that it promotes an inefficient allocation of housing. The argument being: If you let people pay a below-market rent — on the condition that they don’t move — then you’re encouraging them to stay in place. And this leads to things like, for example, empty-nesters continuing to occupy three-bedroom apartments, which would have more utility for younger families.

I think we should recognize that there is a legitimate social interest in saying: Somebody who’s lived in an apartment for 15 years has a right to remain there, even if their landlord decides they could get a higher income by renting to somebody else. I think that’s a perfectly reasonable social goal.

And I think doing that actually makes the housing market more flexible and efficient. Why? Because it means that there’s less pressure to become a homeowner in order to get that security. Right now, in most markets, if you want security of tenure, the only way to get it is through ownership.

And ownership really locks you in. The transaction costs from buying and selling a house are very large. And obviously, in many cases, you get a financial risk, since a house is your main form of savings. If you sell at the wrong time, you lose a lot of money. So we get people who are locked into houses. They don’t have the same degree of geographic mobility. They can’t move to where the job opportunities are better. They stay in a big house even after their children are grown, which would really be better used by a younger family. If we give more security of tenure to renters, more people will choose to rent, and we’ll have actually, I think, a more flexible and efficient housing market.

Last week, the Rent Guidelines Board voted for a freeze on the rent for New York City’s one million rent-regulated apartments, fulfilling one of Mayor Mamdani’s defining campaign promises.

There has been plenty of discussion of the decision, both supportive and critical. But there’s one aspect of it, of particular interest to me, that has not been mentioned: Two out of the mayor’s six appointees to the board are recent graduates of the John Jay MA program in economics, where I teach.

I’m very proud of Sina Sinai and Lauren Melodia, who I know carefully studied the evidence and considered the full range of options before voting for the freeze. Lauren is also doing important work as the Director of Economic and Fiscal Policy at the Center for New York City Affairs, where she is producing a great deal of valuable research, most recently on working conditions in childcare. She’s recently been joined by David Lee, another John Jay graduate, who formerly worked as Legislative Director for New York Assemblymember Ron Kim and is now writing about fiscal policy at the Center.

Meanwhile on the rent regulation front, Anisha Steephen, a current student at John Jay, just released a major report from the Roosevelt Institute on rent regulation as financial regulation, which I hope to be writing more about soon.

This is what studentsfrom the John Jay economics program do. For a small program that’s existed for less than ten years, we have an impressive number of students out in the world contributing to progressive political projects.

Also in the housing space, consider Paul Williams. After finishing his MA with us a few years ago, he established the Center for Public Enterprise, where he now has a dozen staff, and has done as much as anyone to make the case that local government can be a major investor in housing, as well as in energy and other areas. This is a critical part of the both-and approach — boost supply and protect tenants — that defines the Mamdani agenda on housing.

Other current and former John Jay MA students include policy staff for socialist elected officials like State Senator Julia Salazar and former Representative Jamaal Bowman; the legislative director for the UAW; the chief of staff for former New York City Councilmember Carlina Rivera and State Senator Kristen Gonzalez; and analysts and researchers at various government agencies, including several at the Bureau of labor Statistics. Journalists like Aída Chavez (of The Intercept and The Nation) and Kate Aronoff (of The New Republic, and author of A Planet to Win: Why We Need a Green New Deal) were also students here. Jack Gross, founder of the outstanding web journal Phenomenal World, and Nathan Tankus, of the essential newsletter Notes on the Crises, were also briefly students here. (Neither got degrees, but the work and the community matter more than the credential.)

Why am I sharing this? Is it just to brag? Well, partially. I am very proud of what we’ve done with this program over the past decade, and of the students who have passed through it. And to update Hillel, if you don’t talk about your own work, who will talk about it?

But there’s also a more specific and timely reason: For the next two weeks, we are still accepting applications for Fall 2026. And I suspect that readers of this blog must know a few young (or not so young) people interested in studying heterodox economics at a public university in New York City.

If you do know someone who might fit that description, here is the pitch.

Unlike most economics programs, John Jay is unapologetically committed to a progressive, policy-oriented approach, and to the heterodox traditions of Marxian, Keynesian and feminist economics. Our students and faculty see the study of economics both as an end in itself and as a way of contributing to the most pressing struggles in our society.

While many of ours students take up roles in politics, advocacy, journalism and policy research (like on the Rent Guidelines Board) many others continue on to PhD programs. In one recent year, we had an entering class of 15 and eight students who went on to PhD programs, a proportion I suspect very few other MA programs in the country could match, even at much more prestigious institutions.

John Jay College is located at 59th St. and 10th Ave., near Columbus Circle in the heart of Manhattan. All classes in the MA program meet in person one day a week in the evening. Most students take three classes per semester and finish the program in two years, but there is no penalty for going at a different pace.

For anyone who has lived in New York State for at least one year as of September, full-time tuition is $5,545 per semester. This is pro-rated for those taking fewer classes, so the total cost for the program is approximately $22,000 regardless of the time over which it is completed. (This is less than a quarter the tuition at many comparable programs.) For non-resident full time students tuition is somewhat higher, but still cheap compared with most graduate programs.

There’s an online application here. Only the statement of purpose and transcript is required by July 15; recommendation letters can come in later.

There is no requirement to have previously studied economics; our students come from a wide range of backgrounds and many have undergraduate degrees in the humanities, physical sciences or other fields. We are less interested in what classes people have taken than in their intellectual curiosity, a willingness to work hard, and a commitment to using economics training to help change the world.

Does coming to John Jay guarantee that you’ll play a leading role in building municipal socialism? Obviously not. But based on our track record, it does seem to improve the odds.

The other day, Laura and I were standing on the subway platform, on our way to see Boots Riley’s I Love Boosters8, when a young man walked up to us. Well, up to me. “Are you the author of this book,” he asked; he had a copy of Against Money. I said that I was, and asked him if he’d read much of it. Two chapters in so far, he said; he used to follow me on Twitter; he had a pen if I could sign it.

I feel like this is an experience authors of academic books don’t get to have very often. Though I suppose it’s more likely than most places in Park Slope.

I had another nice experience at a reading at Pilsen Community Books in Chicago, a lovely little collectively-owned bookstore I had never been to before. Not a lot of people showed up, but Gabe Winant and I had a good discussion with those who were there. One person in the audience introduced himself as an organizer for UNITE-HERE. We had a good conversation about what motivates workers to join unions, which, today, is practically a matter of defying a totalitarian surveillance state. It’s not mainly about pay, we agreed, it’s about self-respect; or as an organizer I worked with years ago put it, it’s the one’s chance in someone’s life to say “Fuck you” to their boss.

Anyway the discussion went on and toward the end of it a young man in the back asked the question people always ask: ok, but what can I do? What is there to do? I had some answers; Gabe had some better ones, but still not fully satisfactory. Afterwards the young man came up to talk to us. So did the union organizer: What do you do for a living, he asked him. “Oh, well, I just quit my old job” the young guy said. “So, how would you like to work in a hotel?” Afterward they were adjourning to a coffee shop nearby. If the event results in that guy becoming a salt for HERE, then I would say it was an evening well spent.

There are some other responses to Against Money that I am also eager to share.

Our first two reviews are out. One, in Jacobin, is by Mona Ali, whose scholarship on international finance and power I’ve long admired. The second is in Reuters, by Jon Sindreu.Jon is someone I’ve interacted with online for a number of years. He’s a journalist professionally; despite (or because of) that, I feel like he is more in tune with Arjun’s and my particular Keynesian vision than almost any economist I know.

Both reviews are insightful and generous and thoughtful – exactly the kinds of reactions to the book I would have hoped for. One thing I particularly appreciated about both of them is that they don’t just respond to what is in the book, but take its core idea— the difference between money -world with its own internal logic, and the world of productive activity that it interacts with but is distinct from — and carry it in new directions. I think it reflects well on the usefulness of this perspective that they are both able to apply it to other questions that we might have discussed in the book but did not.

Both of them highlight global imbalances as an area where the conflation of money payments with material things is especially pervasive. At the aggregate level, “saving” is just an accounting residual, the difference between total incomes generated from production and consumption spending. As Keynes long ago pointed out, saving is never a constraint at the macro level; any change in investment spending (or the government fiscal balance or the trade balance) mechanically generates an equal change in aggregate saving. Mistaking this accounting category for a quasi-physical substance that can move from place to place — a misapprehension that is ubiquitous in discussion of international trade and finance — leads to all sorts of wrong conclusions, like the idea that financial conditions in the United States are a function of our trade balance with China.

Another area Mona’s review points toward is the idea of degrowth. There is a longstanding desire among economists to regard measures like GDP as reflecting in some sense human wellbeing or happiness, an impulse we criticize at length in the book. But there is a somewhat analogous tendency on the part of some environmentalists to see GDP as a measure of physical throughput or real resource use, so that decarbonization and other sustainability goals necessarily imply a lower path for GDP.The original outline for the book had a chapter called “Planet Money and Planet Earth,” which did not make it in. But we would have argued, as Mona suggests, that to think clearly about the economy and the environment, we need to give up on the idea of a single scalar and turn toward more granular, physical measures, like say, to use her example, the area of tree coverage.

Among other things recognizing money as autonomous and self-referential change the way we think about the productive side of the economy. (This is something Arjun and I have written about elsewhere, but also didn’t get into this book; maybe the next one.)

The view that you get from an economics textbook is that output is effectively a homogeneous substance merging from a production function — a certain quantity of labor and capital goes in one side, and a certain amount of stuff comes out the other. This is an example of seeing concrete reality in the image of money, which really is homogenous — the equivalence of one unit of money to any other unit of money is one of its defining characteristics.

But in reality, production consists of all kinds of complicated forms of specialized cooperation between people; changing what people are making or the conditions under which they make it involves frictions which grow more severe the faster the changes must be made. We may be able to ignore this in the case ofgradual, incremental changes in production, and just say that the next unit of spending results in the next most valuable thing that can be produced. In that case, we can describe the system in terms of a level of spending and a corresponding level of aggregate output. But as soon as the changes get larger or faster, the frictions imposed by the real-world heterogeneity and embeddedness of production become impossible to ignore.

As Sindreu highlights in his review, the conflict between the money-like vision of production and its concrete social reality has come more sharply into view in recent years.

Take the Covid 19 pandemic. Governments had no trouble conjuring $11 trillion for fiscal stimulus. Yet most of the money went to keeping the economy humming, with only about a tenth overall going to the health sector. No amount of paper wealth could procure nurses, masks, hospital beds and vaccines in time to make a difference to the virus’ early spread. Consider also the energy shocks of 2022 and this year, U.S. President Donald Trump’s trade spats, the AI revolution and the war in Ukraine. The relevant metrics in these cases have been barrels of oil, critical minerals, computing power and stockpiles of ammunition. A larger GDP helps fund such purchases, but doesn’t necessarily translate into a greater capacity to build or procure them when they’re actually needed.

To me, an interesting aspect of this is the way it challenges the sort of Keynesian macroeconomics that I teach as well as the standard production-function view. The high ground on which retreating Keynesians made their last stand a generation ago was that short-term fluctuations in activity are the result of shifts in the volume of spending, not the productive capacity of the economy. When output falls in a recession or depression, it’s because something has reduced the capacity to make money payments, not the capacity for real production. The alternative, advancing from the freshwater redoubts of Chicago and Minnesota and Rochester, was the “real business cycle” view — that scarcity and allocation are the only economic problems at the macro as well as the micro level, in the short run as well as the long. For people like me, rejecting this view was the starting point for our engagement with macroeconomic theory.

And yet … wasn’t the pandemic downturn a kind of real business cycle? Thanks to the fiscal response (in the US at least), the flow of money payments was not interrupted. The loss of employment and output was precisely due to a sudden loss of capacity for real productive activity.

As Sindreu stresses, the possibility of disruption on either side — in the web of money payments or in the concrete activity of production — reinforces the need to maintain the conceptual distinction between them. The two cases are very different! What is harder to say is whether the pandemic and subsequent disruptions were a one-off; or whether they were a harbinger of future and especially climate related disruptions to the supply side, as Isabella Weber has suggested; or if they should lead us to rethink historical fluctuations as well. It’s not an easy question! For my part, what I still say in the classroom is: “business cycles are always the result of changes in demand … except for the pandemic.”

One more example: the importance of distinguishing between real and financial provision for the future. At an individual level, they are equivalent: If I want to eat in retirement, the way I provide for that is by amassing claims against society in some financial form. But this does not carry over to aggregate level. Many economists, notes Sindreu, think that funded pension schemes, which back promises to retirees with a pot of financial assets, are more sustainable than pay-as-you-go scheme.

but they’re wrong. … If higher measured wealth doesn’t map onto more physical production in the future…, the ageing problem remains unsolved: while an individual retiree may be able to run down assets to boost consumption, society as a whole will still need enough workers to produce the goods and services demanded.

Here as elsewhere, the problem is that from the point of view of the individual participant in the system, the mapping of money payments on real things is an objective fact: If I pay for so much more of this, I will have to accept less of that. But at the level of the system as a whole, it is not.

Of course you don’t need to read Against Money to observe that GDP is as fetishized by degrowth as by growth for its own sake, or to note that employing people to plant trees boosts measured output and employment just as much as employing people to cut them down. You don’t need to read Against Money to understand that a disruption to production like the pandemic is quite different from the financially-mediated falls in demand of other recessions, or to see that the meals eaten by tomorrow’s retirees must be cooked by tomorrow’s workers, regardless of what is in the Social Security trust fund.

What I hope the book contributes, is to show how these points are connected — that there is a larger worldview implicated in them. Our goal was to bring into light the ideas about money-world and its relationship to concrete production and other social domains, that are implicit in various debates but seldom foregrounded.

So, for example, rejecting a hard tradeoff between decarbonization and meeting people’s immediate material needs should change the way you think about global imbalances. Or — to take another example offered by Sindreu — if you see the strong element of conscious planning driving investment data centers in the US and green energy in China, this awareness of finance as planning should put you on guard against attempts to disguise the actions of the Bank of England as the objective judgement of decentralized bond markets.

Based on the range of fascinating questions that both Mona Ali and Jon Sindreu were able to connect to the arguments of the book, I think we had some success with this. The kinds of issues they brought up point in exactly the directions that we hoped conversations around the book might go. Along with the young people and union activists, these are the readers we were hoping for.

A few other bits of Against Money content.

Arjun was on the “This Is Hell” podcast, with Chuck Mertz, which also airs on WNUR 89.3FM Chicago and Lumpen Radio. I’m especially tickled by the latter, since I was friends with Ed Marszewski and the Lumpen crowd back in the 1990s, and used to hang out at the Marszewski family bar in Bridgeport.

I was on UpFront on KPFA for a 45-minute interview, which is very generous for radio. (The interview itself starts about 12 minutes in.) Brian Edwards-Tiekert of UpFront is a dream interviewer — he had read the book deeply, summarized its key arguments better than I could, and asked thoughtful questions that connected these more abstract debates to the real world debates that are why we care about them.

Finally, I feel compelled to share this review from Amazon. Not just because it’s our first five-star review (though one might pause to consider how the motivating power of prestige and recognition points to the limits of money as a coordination device). But mainly because verified purchaser MudHen so clearly gets what we were trying to do:

Since everything is priced in money, it is all too easy to think, for example, that an object priced at $50,000 has $50,000 of “value” in it somewhere. The equation of price and value simultaneously reifies money (making it a commodity) and casts a veil over the entire material world. This causes us to confuse money and things. That confusion is the bedrock foundation of modern (marginal utility) economics.

Money-is-credit-is-debt points to an end to capitalism. Eventually the entire world is commodified and money is left just valorizing itself in an M-M1 loop which becomes increasingly divorced from use value. At some point, this becomes so ridiculous that everyone can see the problem: uses values are no longer increasing, while nominal (money) wealth is skyrocketing. The Americans are bonkers for their stock market, which is increasingly just a debt (M-M1) financial loop. As the country falls apart, it will become astonishing “wealthy” — and tens of millions of people will slide into functional poverty.

The penalty for confusing money and things is severe, but this book is hopeful. It may not be a matter of envisioning an alternative to capitalism (the hard problem of Jameson/Fisher), so much as the simple realization that most of our growth today is merely financial (number go up). To improve life for everyone, we will have to look beyond money.

Yes, that’s it. The road to a freer, more democratic and egalitarian society doesn’t involve redistributing money claims, but recognizing and building on the ways in which those claims are already and increasingly irrelevant to the activity through which we meet our collective needs.

In the front window of McNally Jackson, one of my favorite NYC bookstores.

Against Money is now out. It’s been spotted in a number of bookstores, including the Union Square Barnes and Noble, where it turns out to be shelved next to Marx’s Capital in the Business section.

As my friend Suresh said to me the other day, as writers we should think of books as landmarks for a larger body of thought, rather than self-contained arguments in themselves. That is certainly the case with this book. But I am glad to see this piece of the larger project out in the world.

We had two very nice launch events, one at the University of Massachusetts (where both of us went to graduate school) and one at John Jay College, my academic home now. Both events had a great turnout, and I very much appreciated the discussion with Christine Dean, Jerry Epstein and Perry Mehrling at the UMass event, and with Zach Carter at the John Jay one. For me, it was like celebrating the holidays first with your family of origin and then with your own family.

Unfortunately, we were not able to record the John Jay event; there was video of the UMass one, but I am not sure when it will be available. But there are a couple other conversations we’ve had about the book recently that I can share.

First is an episode that Arjun and I did with The Climate Pod back in April. Despite the name (and usual focus) of the podcast, host Ty Benefiel had a lot of sharp and insightful questions about the nature of money and its relationship to the social and material world.

Second is an online roundtable we did with members of the Philosophy, Politics and Economics Society. This was a very nice conversation — I think philosophers and political theorists with a deep interest in moneyare perhaps the ideal readers for the book.

One thing I appreciated about both these conversations — and the two launch events — was the pressure our interlocutors put on us to bring out the real-world implications of our arguments, which the book itself is a bit light on. There is naturally a discussion of climate policy on The Climate Pod, but we also get into the pandemic response, democratizing the Fed, and other more real-world questions.

The book itself is primarily an attempt to get out of the flybottle of economic thinking about money, to borrow a phrase from Wittgenstein. But of course this is not just an academic critique — as Christine Desan observed at the UMass event, economics is not just another discipline, it offers a vision of the world that corresponds to the logic of life under the rule of capital. Or as she put it, “We are all in the flybottle.”

We’ve also recorded interviews with Nathan Robinson of Current Affairs, Brian Edwards-Tiekert of UpFront on KPFA, and Doug Henwood for his show Behind the News. I’ll post the links to those as they come out. As we mentioned to Doug, our original title for our book, at the very start of the project, was The Tyranny of Money. This was a nod to the closing lines of his Wall Street, which describes it as “a first draft for a project aiming to end the rule of money, whose tyranny is sometimes a little hard to see.” Like the fly in the bottle, it’s hard to escape when we can’t see the thing we are trapped in.

Arjun and I did a webinar recently on our book Against Money, organized by Merijn Knibbe. We’re very grateful to him for putting it together, and should have video to share soon.

Even in a friendly setting like this, it can be a challenge to explain what the real-world stakes are in debates over money. But as it happens, there was a Matt Levine column the same day as the webinar, that offers a perfect application of one of the central themes of the book.

To be honest, this is not really surprising. You could even think of our project as backfilling the economic theory behind Levine’s columns, which the textbooks certainly don’t help with. “How Keynes explains last week’s Money Stuff” could be an elevator pitch for the book.

The lead item in this Money Stuff was about a hypothetical algae farming startup, and the financing thereof:

You start a startup with a far-fetched idea like genetically engineering algae to produce clean renewable fuel. You go out to investors to raise money. You say “we are going to genetically engineer algae to produce clean renewable fuel, if we succeed we will make a bajillion dollars, you want in?” The investors think that sounds cool, because it does. But they are responsible investors, they do their due diligence, they ask questions like “is that a thing” and “can you actually produce fuel algae” and “will it be cost-effective?” You do your best to answer their questions.

Do you exaggerate? Oh sure. That is the job of a startup founder. I once wrote, approximately:

What you want, when you invest in a startup, is a founder who combines (1) an insanely ambitious vision with (2) a clear-eyed plan to make it come true and (3) the ability to make people believe in the vision now. “We’ll tinker with [algae] for a while and maybe in a decade or so a fuel-[producing strain of algae] will come out of it”: True, yes, but a bad pitch. The pitch is, like, you put your arm around the shoulder of an investor, you gesture sweepingly into the distance, you close your eyes, she closes her eyes, and you say in mellifluous tones: “Can’t you see the [algae producing clean fuel oil] right now? Aren’t they beautiful? So clean and efficient, look at how nicely they [float in this pond], look at all those [genes], all built in-house, aren’t they amazing? Here, hold out your hand, you can touch the [algae] right now. Let’s go for a [swim].”

Of course, you are a startup founder; you are in essence a salesperson. Back at the lab, the algae scientists and chemical engineers and accountants are looking at your pitchbook in disbelief. “Wait, you’re telling investors that we can produce the fuel oil now? You’re telling them that we’ll have large profits in two years? Did you not read our latest status report?” The scientists and accountants are boring and conservative; it is their job to try to make the dream work in dreary reality. It is your job to sell the dream now.

(The brackets are there because he is repurposing text from an earlier column on AI.)

This is a story about finance, not venture capital specifically. The details would be different if the algae company were getting a loan from a bank, but the fundamental situation would be the same.

I want to make a few points about this.

First, what’s being described here is not a market outcome. Nobody has yet purchased any fuel made from genetically modified algae. To the extent there are market signals here, they point in the wrong direction — at current prices, the cost of producing this fuel would be greater than what it would sell for. Nor has this business shown profits in the past — it’s a startup. Right now, the market is saying this is a value-subtracting activity. Funding it anyway is the opposite of what market signals are saying to do.

Funding the algae project is an explicit decision by someone in authority. It is a decision based on promises. It is based, precisely as Levine says, on dreams.9