Krugman is puzzled by the European Central Bank:

I’ve been hearing various attempts to explain the ECB’s utterly bizarre refusal to cut interest rates… The most popular story seems to be that the ECB wants to “hold politicians’ feet to the fire”, letting them know that they won’t get relief unless they do what’s necessary (whatever that is). This really doesn’t make any sense. If we’re talking about enforcing austerity and wage cuts in the periphery, how much more incentive do these economies need?

He is certainly right that if the goal is resolving the crisis, or even price stability, then refusing further rate cuts is mighty strange. But who says those are the goals? His final question is meant to be rhetorical, but it really isn’t. Because the more austerity you want, the more enforcement you need.

I met someone the other day with a fairly senior position at the Greek tax authority; her salary had just been cut by 40 percent. When, outside of an apocalyptic crisis, do you see pay cuts like that? Which, for you or me or Paul Krugman, is an argument to End This Depression Now. But if you are someone who sees pay cuts as the goal, then it could be an argument for not quite yet.

It’s a tenet of liberalism — and a premise of the conversation Krugman is part of — that there are conflicting opinions, but not conflicting interests. But sometimes, when people seem to keep doing things with the wrong outcome, it’s because that’s the outcome they actually want. Paranoid? Conspiracy theory? Maybe. On the other hand, here’s Deutsches Bundsbank president Jens Weidmann:

Relieving stress in the sovereign bond markets eases imminent funding pain but blurs the signal to sovereigns about the precarious state of public finances and the urgent need to act. Macroeconomic imbalances and unsustainable public and private debt in some member states lie at the heart of the sovereign debt crisis. It may appeal to politicians to abstain from unpopular decisions and try to solve problems through monetary accommodation. However, it is up to monetary policymakers to fend off these pressures.

That seems pretty clear. From the perspective of the central banker, resolving the crisis too painlessly would be bad, because that would allow governments to “avoid unpopular decisions.” And it’s true: If there’s something you really want governments to do, but you don’t think they will make the necessary decisions except in a crisis, then it is perfectly rational to prolong the crisis until you see the right decisions being made.

So, what kind of decision are we talking about, exactly? Krugman professes bafflement — “whatever that is” — but it’s not really such a mystery. Here’s an editorial in the FT on the occasion of last summer’s ECB intervention to support the market for Italy’s public debt:

Structural reform is the quid pro quo for the European Central Bank’s purchases last week of Italian government bonds, an action that bought Italy breathing space by driving down yields. … As the government belatedly recognises, boosting Italy’s growth prospects requires a liberalisation of rigid labour markets and a bracing dose of competition in the economy’s sheltered service sectors. This is where the unions and professional bodies must play their part. Susanna Camusso, leader of the CGIL, Italy’s biggest trade union, is threatening to call a general strike to block the proposed labour law reforms. She would be better advised to co-operate with the government and employers… The government’s austerity measures are sure to curtail economic growth in the short run. Only if long overdue structural reforms take root will the pain be worthwhile.

A couple of things worth noting here. First the explicit language of the quid pro quo — the ECB was not just doing what was needed to stabilize the Italian bond market, but offering stabilization as a bargaining chip in order to achieve its other goals. If ECB was selling expansionary policy last year, why be surprised they’re not giving it away for free today? Note also the suggestion that a sacrifice of short-term output is potentially worthwhile — this isn’t some flimflam about expansionary austerity, but an acknowledgement that expansion is being give up to achieve some other goal. And third, that other goal: Everything mentioned is labor market reform, it’s all about concessions by labor (including professionals). No mention of more efficient public services, better regulation of the financial system, or anything like that.

The FT editorialist is accurately presenting the ECB’s view. My old teacher Jerry Epstein has a good summary at TripleCrisis of the conditions for intervention; among other things, the ECB demanded “full liberalisation of local public services…. particularly… the provision of local services through large scale privatizations”; “reform [of] the collective wage bargaining system … to tailor wages and working conditions to firms’ specific needs…”; “thorough review of the rules regulating the hiring and dismissal of employees”; and cuts to private as well as public pensions, “making more stringent the eligibility criteria for seniority pensions” and raising the retirement age of women in the private sector. Privatization, weaker unions, more employer control over hiring and firing, skimpier pensions. This is well beyond what we normally think of as the remit of a central bank.

So what Krugman presents as a vague, speculative story about the ECB’s motives — that they want to hold politicians’ feet to the fire — is, on the contrary, exactly what they say they are doing.

It’s true that the conditions imposed by the ECB on Italy and Greece were in the context of programs relating specifically to those countries’ public debt, while here we are talking about a rate cut. But there’s no fundamental difference — cutting rates and buying bonds are two ways of describing the same basic policy. If there’s conditions for one, we should expect conditions for the other, and in fact we find the same “quid pro quo” language is being used now as then.

Here’s a banker in the FT:

The future of Europe will therefore be determined by the interests of the ECB. Self-preservation suggests that it will prevent complete collapse. If necessary, it will overrule Germany to do this, as the longer-term refinancing operations and government bond purchase programme suggest. But self-preservation and preventing collapse do not amount to genuine cyclical relief and policy stimulus. Indeed, the ECB appears to believe that in addition to price stability it has a mandate to impose structural reform. To this extent, cyclical pain is part of its agenda.

Again, there’s nothing irrational about this. If you really believe that structural reform is vital, and that democratic governments won’t carry it out except under the pressure of a crisis, then what would be irrational would be to relieve the crisis before the reforms are carried out. In this context, an “irrational” moralism can be an advantage. While one can take a hard line in negotiations and still be ready to blink if the costs of non-agreement get too high, it’s best if the other side believes that you’ll blow it all up if you don’t get what you want. Fiat justitia et pereat mundus, says Martin Wolf, is a dangerous motto. Yes; but it’s a strong negotiating position.

But this invites a question: Why does the ECB regard labor market liberalization (aka structural reform) as part of its mandate? Or perhaps more precisely, when the ECB negotiates with national governments, on whose behalf is it negotiating?

The answer the ECB itself might give is, society as a whole. After all, this is the consensus view of central banks’ role. Elected governments are subject to time inconsistency, or are captured by rent seekers, or just don’t work, so an “independent” body is needed to take the long view. It’s never been clear why this should apply only to monetary policy, and in fact there’s a well-established liberal view that the independent central bank model should be extended to other areas of policy. Alan Blinder:

We have drawn the line in the wrong place, leaving too many policy decisions in the realm of politics and too few in the realm of technocracy. … the argument for the Fed’s independence applies just as forcefully to many other areas of government policy. Many policy decisions require complex technical judgments and have consequences that stretch into the distant future. Think of decisions on health policy (should we spend more on cancer or aids research?), tax policy (should we reduce taxes on capital gains?), or environmental policy (how should we cope with damage to the ozone layer?). Yet in such cases, elected politicians make the key decisions. Why should monetary policy be different? … The justification for central bank independence is valid. Perhaps the model should be extended to other arenas. … The tax system would surely be simpler, fairer, and more efficient if … left to an independent technical body like the Federal Reserve rather than to congressional committees.

I’m sure there are plenty of people at the ECB who think along the same lines as the former Fed Vice-Chair. Indeed, that central banks want what’s best for everyone is practically an axiom of modern economics. Still, it’s funny, isn’t it, that “structural reform” so consistently turns out to mean lower wages?

Martin Wolf’s stuff on the European crisis has been essential. But it has one blind spot: The only conflicts he sees are between nations. What perplexes him is “the riddle of German self-interest.” But maybe the answer to the riddle is that national interests are not the only ones in play.

It’s hard not to think here of Perry Anderson’s thesis, developed (alongside other themes) in The New Old World, that the EU project is fundamentally a response by European elites to their inability to roll back social democracy at the national level. The new supra-national institutions of the EU have allowed them to bypass political cultures that remain stubbornly (if incompletely) egalitarian and solidaristic. In Alain Supiot’s summary:

In Anderson’s view, the European project has engendered neither a federation nor an intergovernmental organization; rather it is the most fully realized form of Hayek’s ultraliberal ‘catallaxy’. … Like a secular version of faith in divine providence, belief in the spontaneous order of the markets entails a desire to protect it from the untimely interventions of people seeking ‘a just distribution’ which, according to Hayek, is nothing more than ‘an atavism, based on primordial emotions’. Hence the need to ‘dethrone the political’ by means of constitutional steps which create ‘a functioning market in which nobody can conclusively determine how well-off particular groups or individuals will be’. In other words, it is necessary to put the division of labour and the distribution of its fruits beyond the reach of the electorate. This is the dream that the European institutions have turned into a reality. Beneath the chaste veil of what is conventionally known as the EU’s ‘democratic deficit’ lies a denial of democracy.

Jerry Epstein puts it more bluntly. The ECB’s insistence on structural reform “represents a cynical raw power calculus to destroy worker and citizen protections without any real belief in the underlying neo-liberal economics they use to justify it.” (If you prefer your political economy in audiovisual form, he has a video talking about this stuff.)

This kind of language makes people uncomfortable. Rather than acknowledge that the behavior of people in power could represent a particular interest — let alone that of the top against the bottom, or capital against labor — much better to throw your hands up and profess bafflement: their choices are “bizarre,” a “riddle.” This isn’t, let’s be clear, a personal failing. If you or I occupied the same kind of positions as Krugman or Wolf, we’d be subject to the same constraints. And I anyway don’t want to find myself talking to no one but a handful of grumpy old Marxists.

But on the other hand, as Doug Henwood likes to quote our late friend Bob Fitch, “vulgar Marxism explains 90 percent of what happens in the world.” And then, I keep looking back through FT articles on the crisis, and finding stuff like this:

The central bank has long called for eurozone economies to press ahead with structural reforms. That the ‘E’ in EMU, or Economic and Monetary Union, has not occurred is a complaint often voiced by ECB officials. On this score, the central bank has managed to win an important concession in forcing Italy to sign up to liberalising its economy. Some may see this as a pyrrhic victory for the damage that the bond purchases have done to the central bank’s independence. But there was a significant threat to stability if the central bank did not act. …That Mr Trichet, always among the more politically savvy of central bankers, managed to get some concessions on structural reform was all that could be hoped for.

One has to wonder: What does it mean for the ECB to “win an important concession” from an elected government? Who is it winning the concession for? And if the problem with the ECB is just an ideological fixation on its inflation-fighting credibility, why would it be willing to sacrifice some of that credibility to advance this other goal?

It’s hard to suppress a lingering suppression that central bankers are, after all, bankers. And then you think, isn’t there an important sense in which finance embodies the interests of the capitalist class as a whole? (In an anodyne way, this is even sort of what its conventional capital-allocation function means) You wonder if the only reason Karl Marx called “the modern executive is a committee for managing the common affairs of the whole bourgeoisie,” is that central banks didn’t yet exist.

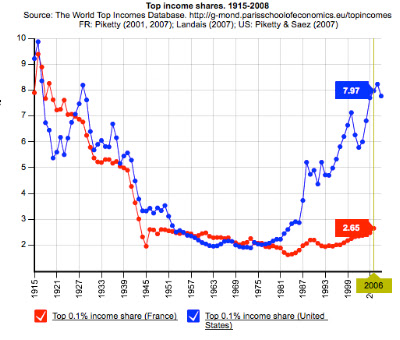

Imagine you’re a European capitalist, or business owner if you prefer the sound of that. You look at the United States and see the promised land. Employment at will — imagine, no laws limiting your ability to fire whoever you want. Private pensions, gone. Unions almost gone, strikes a thing of the past. Meanwhile, in 2002, 95 out of every 1,000 workers in the Euro area — nearly ten percent — was on strike at some point during the year. (In Spain, it was 270 out of every 1,000. In Italy, over 300.) And of course there’s the vastly greater share of income going to your American peers. Look at it from their point of view: Why wouldn’t they want what their American cousins have?

It seems to me that what would really be bizarre, would be if European capitalists did not see the crisis as a once-in-a-lifetime opportunity. They’d be crazy — they’d be betraying their own interests — if, given the ECB’s suddenly increased power vis-a-vis national governments, they didn’t insist that it extract all the concessions it can.

Isn’t that what they’re doing? Moreover, isn’t it what they say they’re doing? When the “Global Head of Market Economics” at the world’s biggest bank says that the ECB should only cut rates “as part of a quid pro quo with governments agreeing to more far-reaching structural reform,” what do you think he means?