More methodenstreit. I finally read the Romer piece on the trouble with macro. Some good stuff in there. I’m glad to see someone of his stature making the point that the Solow residual is simply the part of output growth that is not explained by a production function. It has no business being dressed up as “total factor productivity” and treated as a real thing in the world. Probably the most interesting part of the piece was the discussion of identification, though I’m not sure how much it supports his larger argument about macro. The impossibility of extracting causal relationships from statistical data would seem to strengthen the argument for sticking with strong theoretical priors. And I found it a bit odd that his modus ponens for reality-based macro was accepting that the Fed brought down output and (eventually) inflation in the early 1980s by reducing the money supply — the mechanisms and efficacy of conventional monetary policy are not exactly settled questions. (Funnily enough, Krugman’s companion piece makes just the opposite accusation of orthodoxy — that they assumed an increase in the money supply would raise inflation.) Unlike Brian Romanchuk, I think Romer has some real insights into the methodology of economics. There’s also of course some broadsides against the policy views of various rightwing economists. I’m sympathetic to both parts but not sure they don’t add up to less than their sum.

David Glasner’s interesting comment on Romer makes in passing a point that’s bugged me for years — that you can’t talk about transitions from one intertemporal equilibrium to another, there’s only the one. Or equivalently, you can’t have a model with rational expectations and then talk about what happens if there’s a “shock.” To say there is a shock in one period, is just to say that expectations in the previous period were wrong. Glasner:

the Lucas Critique applies even to micro-founded models, those models being strictly valid only in equilibrium settings and being unable to predict the adjustment of economies in the transition between equilibrium states. All models are subject to the Lucas Critique.

Here’s another take on the state of macro, from the estimable Marc Lavoie. I have to admit, I don’t care for way it’s framed around “the crisis”. It’s not like DSGE models were any more useful before 2008.

Steve Keen has his own view of where macro should go. I almost gave up on reading this piece, given Forbes’ decision to ban on adblockers (Ghostery reports 48 different trackers in their “ad-light” site) and to split the article up over six pages. But I persevered and … I’m afraid I don’t see any value in what Keen proposes. Perhaps I’ll leave it at that. Roger Farmer doesn’t see the value either.

In my opinion, the way forward, certainly for people like me — or, dear reader, like you — who have zero influence on the direction of the economics profession, is to forget about finding the right model for “the economy” in the abstract, and focus more on quantitative description of concrete historical developments. I expressed this opinion in a bunch of tweets, storified here.

The Gosplan of capitalism. Schumpeter described banks as capitalism’s equivalent of the Soviet planning agency — a bank loan can be thought of as an order allocating part of society’s collective resources to a particular project. This applies even more to the central banks that set the overall terms of bank lending, but this conscious direction of the economy has been hidden behind layers of ideological obfuscation about the natural rate, policy rules and so on. As DeLong says, central banks are central planners that dare not speak their name. This silence is getting harder to maintain, though. Every day there seems to be a new news story about central banks intervening in some new credit market or administering some new price. Via Ben Bernanke, here is the Bank of Japan announcing it will start targeting the yield of 10-year Japanese government bonds, instead of limiting itself to the very short end where central banks have traditionally operated. (Although as he notes, they “muddle the message somewhat” by also announcing quantities of bonds to be purchased.) Bernanke adds:

there is a U.S. precedent for the BOJ’s new strategy: The Federal Reserve targeted long-term yields during and immediately after World War II, in an effort to hold down the costs of war finance.

And in the FT, here is the Bank of England announcing it will begin buying corporate bonds, an unambiguous step toward direct allocation of credit:

The bank will conduct three “reverse auctions” this week, each aimed at buying the bonds from particular sectors. Tuesday’s auction focuses on utilities and industries. Individual companies include automaker Rolls-Royce, oil major Royal Dutch Shell and utilities such as Thames Water.

Inflation or socialism. That interventions taken in the heat of a crisis to stabilize financial markets can end up being steps toward “a more or less comprehensive socialization of investment,” may be more visible to libertarians, who are inclined to see central banks as a kind of socialism already. At any rate, Scott Sumner has been making some provocative posts lately about a choice between “inflation or socialism”. Personally I don’t have much use for NGDP targeting — Sumner’s idée fixe — or the analysis that underlies it, but I do think he is onto something important here. To translate the argument into Keynes’ terms, the problem is that the minimum return acceptable to wealth owners may be, under current conditions, too high to justify the level of investment consistent with the minimum level of growth and employment acceptable to the rest of society. Bridging this gap requires the state to increasingly take responsibility for investment, either directly or via credit policy. That’s the socialism horn of the dilemma. Or you can get inflation, which, in effect, forces wealthholders to accept a lower return; or put it more positively, as Sumner does, makes it more attractive to hold wealth in forms that finance productive investment. The only hitch is that the wealthy — or at least their political representatives — seem to hate inflation even more than they hate socialism.

The corporate superorganism. One more for the “finance-as-socialism” files. Here’s an interesting working paper from Jose Azar on the rise of cross-ownership of US corporations, thanks in part to index funds and other passive investment vehicles.

The probability that two randomly selected firms in the same industry from the S&P 1500 have a common shareholder with at least 5% stakes in both firms increased from less than 20% in 1999Q4 to around 90% in 2014Q4 (Figure 1).1 Thus, while there has been some degree of overlap for many decades, and overlap started increasing around 2000, the ubiquity of common ownership of large blocks of stock is a relatively recent phenomenon. The increase in common ownership coincided with the period of fastest growth in corporate profits and the fastest decline in the labor share since the end of World War II…

A common element of theories of the firm boundaries is that … either firms are separately owned, or they combine. In stock market economies, however, the forces of portfolio diversification lead to … blurring firm boundaries… In the limit, when all shareholders hold market portfolios, the ownership of the firms becomes exactly identical. From the point of view of the shareholders, these firms should act “in unison” to maximize the same objective function… In this situation the firms have in some sense become branches of a larger corporate superorganism.

The same assumptions that generate the “efficiency” of market outcomes imply that public ownership could be just as efficient — or more so in the case of monopolies.

The present paper provides a precise efficiency rationale for … consumer and employee representation at firms… Consumer and employee representation can reduce the markdown of wages relative to the marginal product of labor and therefore bring the economy closer to a competitive outcome. Moreover, this provides an efficiency rationale for wealth inequality reduction –reducing inequality makes control, ownership, consumption, and labor supply more aligned… In the limit, when agents are homogeneous and all firms are commonly owned, … stakeholder representation leads to a Pareto efficient outcome … even though there is no competition in the economy.

As Azar notes, cross-ownership of firms was a major concern for progressives in the early 20th century, expressed through things like the Pujo committee. But cross-ownership also has been a central theme of Marxists like Hilferding and Lenin. Azar’s “corporate superorganism” is basically Hilferding’s finance capital, with index funds playing the role of big banks. The logic runs the same way today as 100 years ago. If production is already organized as a collective enterprise run by professional managers in the interest of the capitalist class as a whole, why can’t it just as easily be managed in a broader social interest?

Global pivot? Gavyn Davies suggests that there has been a global turn toward more expansionary fiscal policy, with the average rich country fiscal balances shifting about 1.5 points toward deficit between 2013 and 2016. As he says,

This seems an obvious path at a time when governments can finance public investment programmes at less than zero real rates of interest. Even those who believe that government programmes tend to be inefficient and wasteful would have a hard time arguing that the real returns on public transport, housing, health and education are actually negative.

I don’t know about that last bit, though — they don’t seem to find it that hard.

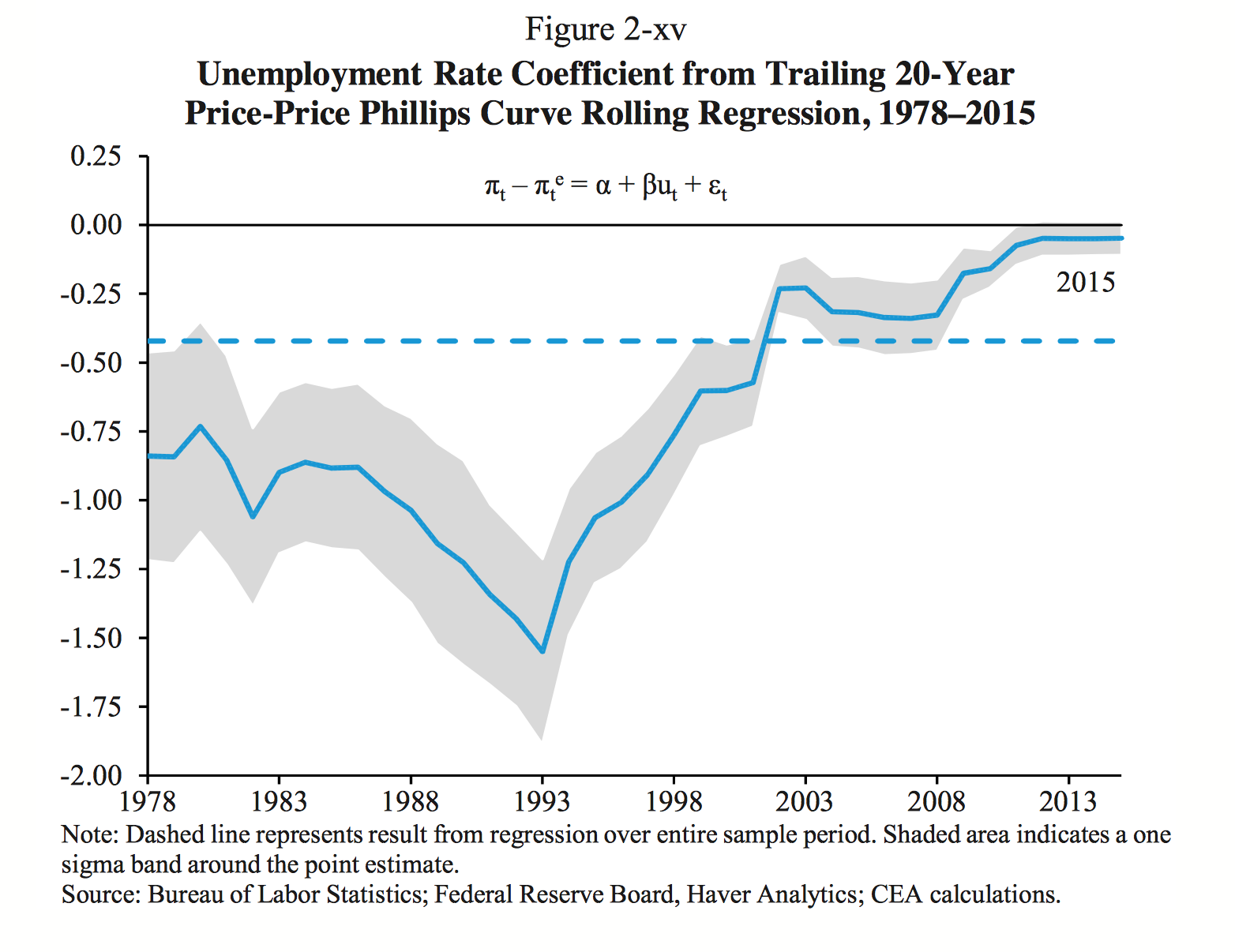

Taylor rule toy. The Atlanta Fed has a cool new gadget that lets you calculate the interest rate under various versions of the Taylor Rule. It will definitely be useful in the classroom. Besides the obvious pedagogical value, it also dramatizes a larger point — that macroeconomic variables like “inflation” aren’t objects simply existing in the world, but depend on all kinds of non-obvious choices about measurement and definition.

The new royalists. DeLong summarizes the current debates about monetary policy:

1. Do we accept economic performance that all of our predecessors would have characterized as grossly subpar—having assigned the Federal Reserve and other independent central banks a mission and then kept from them the policy tools they need to successfully accomplish it?

2. Do we return the task of managing the business cycle to the political branches of government—so that they don’t just occasionally joggle the elbows of the technocratic professionals but actually take on a co-leading or a leading role?

3. Or do we extend the Federal Reserve’s toolkit in a structured way to give it the tools it needs?

This is a useful framework, as is the discussion that precedes it. But what jumped out to me is how he reflexively rejects option two. When it comes to the core questions of economic policy — growth, employment, the competing claims of labor and capital — the democratically accountable, branches of government must play no role. This is all the more striking given his frank assessment of the performance of the technocrats who have been running the show for the past 30 years: “they—or, rather, we, for I am certainly one of the mainstream economists in the roughly consensus—were very, tragically, dismally and grossly wrong.”

I think the idea that monetary policy is a matter of neutral, technical expertise was always a dodge, a cover for class interests. The cover has gotten threadbare in the past decade, as the range and visibility of central bank interventions has grown. But it’s striking how many people still seem to believe in a kind of constitutional monarchy when it comes to central banks. They can see people who call for epistocracy — rule by knowers — rather than democracy as slightly sinister clowns (which they are). And they can simultaneously see central bank independence as essential to good government, without feeling any cognitive dissonance.

Did extending unemployment insurance reduce employment? Arin Dube, Ethan Kaplan, Chris Boone and Lucas Goodman have a new paper on “Unemployment Insurance Generosity and Aggregate Employment.” From the abstract:

We estimate the impact of unemployment insurance (UI) extensions on aggregate employment during the Great Recession. Using a border discontinuity design, we compare employment dynamics in border counties of states with longer maximum UI benefit duration to contiguous counties in states with shorter durations between 2007 and 2014. … We find no statistically significant impact of increasing unemployment insurance generosity on aggregate employment. … Our point estimates vary in sign, but are uniformly small in magnitude and most are estimated with sufficient precision to rule out substantial impacts of the policy…. We can reject negative impacts on the employment-to-population ratio … in excess of 0.5 percentage points from the policy expansion.

Media advisory with synopsis is here.

On other blogs, other wonders

Larry Summers: Low laborforce participation is mainly about weak demand, not demographics or other supply-side factors.

Nancy Folbre on Greg Mankiw’s claims that the one percent deserves whatever it gets.

At Crooked Timber, John Quiggin makes some familiar — but correct and important! — points about privatization of public services.

In the Baffler, Sam Kriss has some fun with the new atheists. I hadn’t encountered Kierkegaard’s parable of the madman who tells everyone who will listen “the world is round!” but it fits perfectly.

A valuable article in the Washington Post on cobalt mining in Africa. Tracing out commodity chains is something we really need more of.

Buzzfeed on Blue Apron. The reality of the robot future is often, as here, just that production has been reorganized to make workers less visible.

At Vox, Rachelle Sampson has a piece on corporate short-termism. Supports my sense that this is an area where there may be space to move left in a Clinton administration.

Sven Beckert has edited a new collection of essays on the relationship between slavery and the development of American capitalism. Should be worth looking at — his Empire of Cotton is magnificent.

At Dissent, here’s an interesting review of Jefferson Cowie’s and Robert Gordon’s very different but complementary books on the decline of American growth.

{kind=link}