“Probably more uninformed statements have been made on public-sector debt and deficits,” says Willem Buiter, “than on any other subject in macroeconomics. Proof by repeated assertion has frequently appeared to be an acceptable substitute for proof by deduction or proof by induction.”

It’s hard to disagree.

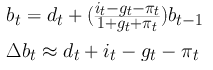

But at least we know where an informed discussion starts. It starts from the least controversial equation of macroeconomics, the law of motion of public debt:

b is the ratio of public debt to GDP, d is the ratio of primary deficit to GDP, i is the nominal interest rate, g is the real growth rate of GDP, and pi is inflation. In principle this is true by definition. (In practice things aren’t alway so simple.) The first thing you realize, looking at this equation, is that contrary to the slack-jawed bleating of conventional opinion, there’s no necessary connection between the evolution of public debt and government spending and taxes. Interest rates, growth rates and inflation are, in principle, just as important as the primary balance. Which naturally invites the question, which have been more important in practice?

There have been various efforts to answer this question for different countries in different periods, but until recently there wasn’t any systematic effort to answer it for a broad sample of countries over a long period. I was thinking of trying to do such an exercise myself. But it looks like that’s not necessary. As Tom M. points out in comments, the IMF has just undertaken such an exercise. Using the new Historical Public Debt Database, they’ve decomposed the debt-GDP ratios of 174 countries, from 1880 to the present, into the four components of the law of motion. (Plus a fifth, discussed below.) It’s an impressive project. Ands far as one can tell from this brief presentation, they did it right. Admittedly it’s a laconic 25-page powerpoint, but there’s not even the hint of a suggestion that microfoundations or welfare analysis would contribute anything. The question is just, how much has each of the components contributed to shifts in debt-GDP ratios historically?

As I’ve noted here before, the critical issue is the relationship between g and i, or (g + pi) and i as I’ve written it here. On this point, the IMF study gives ammunition to both sides.

From roughly 1895 to 1920, and from 1935 to 1980, nominal growth rates (g + pi) generally exceeded nominal interest rates. From 1880 to 1895, from 1920 to 1935, and from 1980 to the present, interest mostly exceeded growth. It’s impossible, looking at this picture, to say one relationship or the other is normal. Lernerian-Keynesians will say, why can’t the conditions of the postwar decades be reproduced by any government that chooses to; while the orthodox (Marxists and neoclassicals equally) will say the postwar decades were anomalous for various reasons — financial repression, limited international mobility of capital, exceptionally strong growth. The historical evidence doesn’t clearly resolve the question either way.

Given the unstable relationship between g and i, it’s not surprising there’s no consistent pattern in episodes of long-term reduction in debt-GDP ratios. I had hoped such episodes would turn out to be always, or almost always, the result of faster growth, lower interest rates, and higher inflation. This is basically true for the postwar decades, when the biggest debt reductions happened. Since 1980, though, it seems that countries that have reduced their debt-GDP ratios have done it the hard way, by taxing more than they spent. Over the whole period since 1880, periods of major (at least 10 percent of GDP) debt reduction has involved primary surpluses and g > r in about equal measure.

Another interesting point is how much the law of motion turns out to have exceptions. The IMF’s version of the equation above includes an additional term on the right side: SFA, or stock-flow adjustment, meaning the discrepancy between the flow of debt implied by the other terms of the equation and the stock of debt actually observed. This discrepancy turns out to be often quite large. This could reflect a lot of factors; but for recent episodes of rising debt-GDP ratios (in which SFA seems to play a central role) the obvious interpretation is that it reflects the assumption by the government of the banking system’s debts, which is often not reflected in official deficit statistics but may be large relative to the stock of debt. The extreme case is Ireland, where the government guarantee of the financial system resulted in the government assuming bank liabilities equal to 45 percent of GDP. To the extent this is an important factor in rising public debt generally — and again, the IMF study supports it — it suggests another reason why concern with balancing the long-term budget by “reforming” Medicare, etc., is misplaced. One financial crisis can cancel out decades of fiscal rectitude; so if you’re concerned about what the debt-GDP ratio will be in 2075, you should spend less time thinking about public spending and taxes, and much more time thinking about effective regulation of the financial sector.

The bottom line is, the dynamics of public debt are complicated. But as always, intractable theoretical controversies become more manageable, or at least more meaningful, when they’re posed as concrete historical questions. Good on the IMF for doing this.