“Probably more uninformed statements have been made on public-sector debt and deficits,” says Willem Buiter, “than on any other subject in macroeconomics. Proof by repeated assertion has frequently appeared to be an acceptable substitute for proof by deduction or proof by induction.”

It’s hard to disagree.

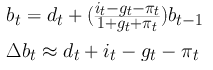

But at least we know where an informed discussion starts. It starts from the least controversial equation of macroeconomics, the law of motion of public debt:

b is the ratio of public debt to GDP, d is the ratio of primary deficit to GDP, i is the nominal interest rate, g is the real growth rate of GDP, and pi is inflation. In principle this is true by definition. (In practice things aren’t alway so simple.) The first thing you realize, looking at this equation, is that contrary to the slack-jawed bleating of conventional opinion, there’s no necessary connection between the evolution of public debt and government spending and taxes. Interest rates, growth rates and inflation are, in principle, just as important as the primary balance. Which naturally invites the question, which have been more important in practice?

There have been various efforts to answer this question for different countries in different periods, but until recently there wasn’t any systematic effort to answer it for a broad sample of countries over a long period. I was thinking of trying to do such an exercise myself. But it looks like that’s not necessary. As Tom M. points out in comments, the IMF has just undertaken such an exercise. Using the new Historical Public Debt Database, they’ve decomposed the debt-GDP ratios of 174 countries, from 1880 to the present, into the four components of the law of motion. (Plus a fifth, discussed below.) It’s an impressive project. Ands far as one can tell from this brief presentation, they did it right. Admittedly it’s a laconic 25-page powerpoint, but there’s not even the hint of a suggestion that microfoundations or welfare analysis would contribute anything. The question is just, how much has each of the components contributed to shifts in debt-GDP ratios historically?

As I’ve noted here before, the critical issue is the relationship between g and i, or (g + pi) and i as I’ve written it here. On this point, the IMF study gives ammunition to both sides.

From roughly 1895 to 1920, and from 1935 to 1980, nominal growth rates (g + pi) generally exceeded nominal interest rates. From 1880 to 1895, from 1920 to 1935, and from 1980 to the present, interest mostly exceeded growth. It’s impossible, looking at this picture, to say one relationship or the other is normal. Lernerian-Keynesians will say, why can’t the conditions of the postwar decades be reproduced by any government that chooses to; while the orthodox (Marxists and neoclassicals equally) will say the postwar decades were anomalous for various reasons — financial repression, limited international mobility of capital, exceptionally strong growth. The historical evidence doesn’t clearly resolve the question either way.

Given the unstable relationship between g and i, it’s not surprising there’s no consistent pattern in episodes of long-term reduction in debt-GDP ratios. I had hoped such episodes would turn out to be always, or almost always, the result of faster growth, lower interest rates, and higher inflation. This is basically true for the postwar decades, when the biggest debt reductions happened. Since 1980, though, it seems that countries that have reduced their debt-GDP ratios have done it the hard way, by taxing more than they spent. Over the whole period since 1880, periods of major (at least 10 percent of GDP) debt reduction has involved primary surpluses and g > r in about equal measure.

Another interesting point is how much the law of motion turns out to have exceptions. The IMF’s version of the equation above includes an additional term on the right side: SFA, or stock-flow adjustment, meaning the discrepancy between the flow of debt implied by the other terms of the equation and the stock of debt actually observed. This discrepancy turns out to be often quite large. This could reflect a lot of factors; but for recent episodes of rising debt-GDP ratios (in which SFA seems to play a central role) the obvious interpretation is that it reflects the assumption by the government of the banking system’s debts, which is often not reflected in official deficit statistics but may be large relative to the stock of debt. The extreme case is Ireland, where the government guarantee of the financial system resulted in the government assuming bank liabilities equal to 45 percent of GDP. To the extent this is an important factor in rising public debt generally — and again, the IMF study supports it — it suggests another reason why concern with balancing the long-term budget by “reforming” Medicare, etc., is misplaced. One financial crisis can cancel out decades of fiscal rectitude; so if you’re concerned about what the debt-GDP ratio will be in 2075, you should spend less time thinking about public spending and taxes, and much more time thinking about effective regulation of the financial sector.

The bottom line is, the dynamics of public debt are complicated. But as always, intractable theoretical controversies become more manageable, or at least more meaningful, when they’re posed as concrete historical questions. Good on the IMF for doing this.

JW: You could probably write about watching grass grow, and make it interesting.

Please clarify something for me… You write: "…the obvious interpretation is that it reflects the assumption by the government of the banking system's debts…"

I'm thinking TARP and QE (except QE doesn't add to the public debt, so just TARP). Of TARP, Wikipedia says the government purchased "assets and equity from financial institutions".

The government did not assume the *debt* of those financial institutions; it assumed the *risk*. Methinks debt is a liability, not an asset. The government purchased the troubled assets, but left the troubled liabilities festering in the private sector.

If the government had borrowed money and used that money to pay off debt for debtors, there would have been a transfer of debt from the private sector to the public. But they did not do this. Therefore, it is incorrect to say that the government "assumed" anybody's debt.

This is an important point for me. But I am a nontechnical person dealing with technical terms. I would appreciate any guidance you can offer.

Art

Arthurian-

Thanks!

In that line, I was thinking of countries like Ireland, more than the US. I've clarified this in the post.

On the specific issue, it's true that the Fed purchased assets rather than assuming debt, but to make those purchases, it had to emit liabilities — initially by selling off its stock of treasuries, then, when they ran low, creating new reserves. So TARP and its relatives did add to the stock of federal debt held by the public, and to the liabilities of the Fed — that's what all those excess reserves are. But you're right, that didn't affect the headline debt numbers, since US national accounts treat the monetary authority separately from the federal government. The same interventions would have meant a big increase in the federal debt if they had been conducted by the Treasury, or if the national accounts considered the Fed part of the federal government. I'm not sure what is standard practice internationally.

Thank you, JW. Makes sense, now that you lay it out for me.

"TARP and its relatives did add to the stock of federal debt held by the public, and to the liabilities of the Fed"

Understood. So I think I can say that TARP and friends (a) did increase total debt; and (b) did not transfer debt out of the private sector. (A) is the reason people are unhappy with government. (B) is the reason the effort has not succeeded.

Let me use the 'repeated assertion' technique and say (again) that if you fail to look at US Federal debt in the context of Non-Federal debt, you miss the *whole* story. If I may pass along a link, it is this brief criticism of Reinhart and Rogoff's "Growth in a Time of Debt". The graph at the end of the post — showing debt considered and debt not considered by Reinhart and Rogoff — is what I want you to see.

On a different topic… The first graph in your post (Interest-Growth Differential, from the IMF PDF) looks like the discovery of a new business cycle. Those fat recession bars affect my judgment. But looking at it as a cycle has implications for your Lernerian-Keynesians and the others.

Thanks again for the clarification.

1895 to 1920 inflationary period

1935 to 1980 inflationary period

1880 to 1895 deflationary period

1920 to 1935 deflationary period

1980 to 2007 disinflationary period

One could think in real terms, of θ (real GNP) and r (i – π), as I recall our friend Olivier Blanchard insisted on doing, taking no notice of the forced anomaly of "real debt". Then, the question of whether g or i is larger, might seem a somewhat mysterious matter of exogenous conditions and potential.

Nominal values suggest monetary policy might have something to do with it, no? Even without a committment to functional finance, it ought to be fairly obvious that a low, stable but positive rate of inflation would be a necessary condition for maintaining stable financial intermediation and taking up all available investment opportunities with a positive net present value in real terms.

Deflation, with cash offering a positive real rate of return, screws financial intermediation, and will prevent taking up many investment opportunities with a small positive net present value in real terms, because such investments will have a negative return in nominal terms.

An alternative way of expressing this would be that deflation, by screwing up financial intermediation, makes it impossible to give firms an optimal capital structure, and therefore, incentive structure.

The implication of a slow, prolonged disinflation would be that a 'Greenspan put' can be fatally corrupting, and lead to either taking up investment opportunities with a negative net present value, or even to a crowding out of genuine net positive rate of return investments by ponzi schemes.

In all cases, the marketable national debt of a sovereign with a central bank, would bear a "risk-free" rate, somewhat detached from real rates of return on investment.

I don't see any plausible argument or scenario, in which the nominal rate of return on sovereign debt could be elevated by competing opportunities for private investment returns, absent bad monetary policy.

Well, this is certainly a more intelligent conversation than the cat fight between Krugman and the MMTers. I think this post pretty much sums up what we know and don't know. Let me add my two-cents worth on what might be at stake politically.

If you take the MMT position seriously, it gives us permission to adopt a permanent role of deficit denial. This has, in fact, been the role of the left in public debates over the last two decades, against the Ben Friedmanites, e.g. But if you take the alternative position, (that primary fiscal supluses are at some point necessary), then the left has to engage that debate on the basis of advocating for the working class(es?) around the distributional burden of debt servicing. One advantage here would be that we would probably be able to find some common ground with the Krugmans of the world, if we basically accept the 'jobs now, deficits later' paradigm (from a short-run Keynesian, long-run classical/Marxian perspective, not a long-run neoclassical perspective). So a lot is at stake.

Hi Tom.

Thanks! and thanks for the link. I think the MMT people definitely have some good points, but it's hard not to agree to Krugman about their tone. They're not doing themselves any favors by presenting their position in a purely logical-deductive way, as if the absence of a financial constraint on government budgets could be deduced from first principles. In the real world it seems clear that even governments that borrow only in their own currency can face financial constraints to different degrees depending on the economic and institutional context.

In that vein, here are some questions we need to think about:

* The issue you raise, do demand constrains bind in the short run only, or in the long run as well? Shaikh, Dumenil & Levy, and a lot of other very smart Marxists insist demand doesn't bind in the long-run, that it isn't even meaningful to talk about long run aggregate demand. Obviously the mainstream thinks the same. I'm not completely convinced. But if that's right then g is exogenous to fiscal policy (it can still be affected by spending on education, infrastructure etc.) But if you take the Kaleckian view where there is an autonomous investment function and demand matters for growth, then it's possible that deficit spending can pay for itself through higher output not just cyclically but secularly.

* The relationship of i and g, which I've stressed in my posts here. As Bruce Wilder says, this seems to be related to inflationary or deflationay trends in the larger economy. But it is also true that nominal interest rates were quite low from 1945 to 1975 or so, compared to most of the last 30 years.

* The relation of nominal interest rates to inflation. Every textbook, mainstream or alternative, incorporates the Fisher equation that says changes in inflation are passed through one-to-one to nominal interest rates. The only debate is whether this happens based on expected inflation, current inflation, or past inflation with some lag. But if this is true, then assuming debt of finite maturity, a temporary period of higher inflation will leave the debt-GDP ratio unaffected. The only way temporary inflation can permanently reduce the debt burden, is if the Fisher equation doesn't obtain and changes in inflation are not fully passed through to nominal interest rates even with a lag. Pretty much every empirical paper on debt dynamics, including this IMF one, does work with nominal interest rates and real growth rates, implicitly rejecting the Fisher equation and accepting the radical position that interest rates are conventions rather than set by fundamentals. This needs to be developed further.

(continued)

* How public debt relates to other assets in private portfolios. In the orthodox version they're both just claims on future income flows, so they're substitutes and public debt crowds out fixed capital. But in a Minskyan view (which you can also sort of find in mainstream guys like Jean Tirole who've never read Minsky) where the constraint on private asset holdings is liquidity (i.e. capacity to meet cash commitments), rather than willingness to consume later rather than consume now, things aren't so straightforward. Public debt holdings might be a use of liquidity, but they also might be a source of it, in which case public and private debt could be complements rather than substitutes. Something like this is presumably involved in the "flight to safety" that drives up the price of treasuries in crises, but it has implications for the longer term effects of government borrowing on interest rates as well.

* The rest of the world's need for dollars as foreign exchange reserves, and the advantages of meeting incremental reserve demand via additions to the stock of federal debt. This is Jorg Bibow's argument, which I really should do a full post on, because it's very smart.

I'm trying to write something more systematic about these issues. We'll see.

I don't see any plausible argument or scenario, in which the nominal rate of return on sovereign debt could be elevated by competing opportunities for private investment returns, absent bad monetary policy.

This is the crux of it. One of the cruxes, anyway. (Is that a solecism?) The orthodox view is that public debt and private assets are competing for a pool of savings that is fixed by the terms on which people are willing to trade present for future consumption. So abstracting from default risk, they should carry an identical rate of return, which is set by preferences and technology.

Rejecting this view was, arguably, the central contribution of The General Theory — that with respect toe real (nononetary) parameters of the economy, the interest rate is indeterminate — left floating "in the air". Unfortunately, this part of Keynes's argument has mostly been forgotten, and the position you (and I) find completely implausible, is accepted by most "Keynesian" economists as almost self-evidently true.

This discussion quickly gets into some of the deepest questions in political economy, such as the nature of fiat money or the relationship between the rate of profit and the rate of interest. I don't have any good answers. But I have been working on a little model that has the short-run/long-run properties that a classical theory suggests. (Its all in real terms, so can't address the question of inflating away debt.)

Let I/K = d0 – d1 r + d2 u where r is the real interest rate and u is capacity utilization. This is a standard Kalecian device.

Let S/K = s pi rho u where s is the capitalist saving rate, pi is profit share, rho is capital productivity or the potential output/capital ratio. I.e., the Cambridge saving equation. Workers don't save. Obviously, I/K=S/K=g.

Now add the assumption that inflation depends on utilization, through a Phillips curve-like relationship. Normalize so u=1 is full or normal utilization, where inflation stabilizes.

If the monetary authority follows a Taylor rule and sets r in order to stabilize inflation, the long run will be at u=1. (There are other ways to get u=1, such as Shaikh's, but this follows Dumenil/Levy sort of.)

It is easy to show that in the long run, g>r iff s pi rho > (d0 + d2)/(1+d1).

So g>r (as in the Golden Age) is possible. But it depends on the capitalists propensity to accumulate and the normal profit rate, pi rho. One interpretation of what's going on is that neoliberalism is basically a low-accumulation environment, making g<r more likely.

Either way, this model helps me understand why the real interest rate can't be chosen at will, as the MMT crowd sometimes (Galbraith) asserts. (It also concedes they could be right!)

It looks like a good platform for attacking the problem of debt dynamics, but I'm still at it. Hope I haven't overstayed my welcome….

Not at all! This stuff is fascinating. Do you have a paper you can send me? I'm at jwmason@econs.umass.edu.

I was just reading Dutt's recent CJE piece on AD in classical-Marxian models, which I thought really helpfully clarified the Keynesian in the short run/classical in the long run debate. What did you think of that article?

I'm inclined to agree that a secular decline in investment demand (at any given level of profitability and capacity utilization), basically due to the stronger claims of rentiers on firms' income, is a central feature of neoliberalism.

Fascinating post and discussion – if I may say so as a non-expert. Tom, what's d0, d1, d2 in your model?

As for "neoliberalism is a low-accumulation environment" wouldn't it maybe be more precise to say that it is an organizational and ideological response to a low-accumulation environment – meaning an attempt to keep rates of capitalist profit high in an environment that inhibits further capital accumulation…

Fascinating, it is. The bits of it I get, anyway…

JW, you write: "I'm inclined to agree that a secular decline in investment demand (at any given level of profitability and capacity utilization), basically due to the stronger claims of rentiers on firms' income, is a central feature of neoliberalism."

I don't have anything to back me up, other than observation) but "the stronger claims of rentiers on firms' income" is not limited to the "neoliberal" era (assuming that is Reaganomics). It is visible in the full post-WWII period, incrementally increasing.

And the cause, clear as a bell sir, the cause is that we think we need credit for growth.

I'll be quiet now.

… but, I'm not sure if your model, as I understand it, really goes to the MMT argument. Their position is that the interest can be fixed permanently at some very low level. Then taxes and/or transfers are adjusted to make up the difference (positive or negative) between consumption plus investment at that interest rate, and full utilization. One question is whether the monetary authority is capable of holding the nominal interest rate at a fixed level forever. I can't see why not (tho in an open economy you will need some kind of limit on cross-border transactions, such as capital controls.) But the more serious problem is whether the inflation-output tradeoff is stable. This was what Lerner, who invented this stuff, ended up worrying about, and I believe his conclusion was that you would probably need some additional tools — anti-trust policy and maybe direct price controls — to stabilize the relationship between inflation and utilization. Related to this is whether the stock of debt has implications for inflation.

But you can't get at these issues in a model without fiscal policy, where a commitment to maintain u=1 determines the interest rate, I don't think.

Sorry, no paper yet. Also sorry for being so telegraphic. d0, d1, d2 are just parameters in the investment equation; they describe how managers respond to the interest rate (d1) and utilization (d2) in making their investment decision. The model is really a dynamic version of the textbook keynesian-cross model, solved by setting S=I.

This is one of the models that Amitava deconstructs, and yes, that is a useful paper. I'm trying to work up a response to him as part of this project. He basically asserts that aggregate demand can affect the value of labor power (here 1-profit share), so it will have long run growth rate effects. He also believes (in his comments on Dumenil/Levy) that the utilization rate (observed capital productivity, or rho u in my model) is a long run variable with no 'normal' level. To me, both of those are part of the structure of capitalism and can't be changed through fiscal/monetary demand policy alone. So his paper really clarified, for me, the difference between SR keynes/LR marx and SR keynes/LR keynes. Good paper.

I think you are right that this little model probably won't satisfy the MMT/Lernerites. Lavoie/Godwin (Levy working paper) provide some examples of how the interest rate can be fixed, and then fiscal policy adjusts to keep utilization full. But they still have to respect the sustainability equation of motion you wrote out–they do it by making fiscal policy adjust. So I don't think that addresses Galbraith's position that deficits don't matter because you can choose BOTH the primary deficit and the interest rate.

As for neoliberalism, the comments on it seem right to me. I think Dumenil/Levy's book is pretty good–you can read my review in the July-August New Left Review.

Oh, you're that Tom M. Very cool. I'm delighted you're reading the blog.

I'm reading your paper now and will hopefully have some thoughts shortly.

Christian and Art-

I'll try to develop the argument that neoliberalism involved a reassertion of the claims of owners of financial assets as against the management of firms, in a new post.

Great discussion. The frisson between our gracious host and Tom M is terrific. Crisis of Neoliberalism sounds like a potentially important book. I wonder how well it would juxtapose with Michael Pettis' The Volatility Machine in exposing the topic of managing sovereign finance.

The most important thing to realize about neoliberalism is that neoliberalism's doctrine of public policy is stupid. Arguing with stupid is hazardous. I'm sure I'm preachin' to the choir, but just sayin' it again, to be sure.

christian h.: ". . . an attempt to keep rates of capitalist profit high in an environment that inhibits further capital accumulation…"

It is one of the sadly neglected, but insightful paradoxes of the marginal analysis of income distribution, that share of income is inverse to accumulation. Inhibiting further capital accumulation is a means and necessary condition for keeping capitalist profit high. Inhibition of capital accumulation *is* the attempt to keep capitalist profit high — that attempt is the defining core of the "environment", because the inhibition is the means to the end.