I haven’t been blogging much lately. I’ve been doing real work, some of which will be appearing soon. But if I were blogging, here are some of the posts I might write.

*

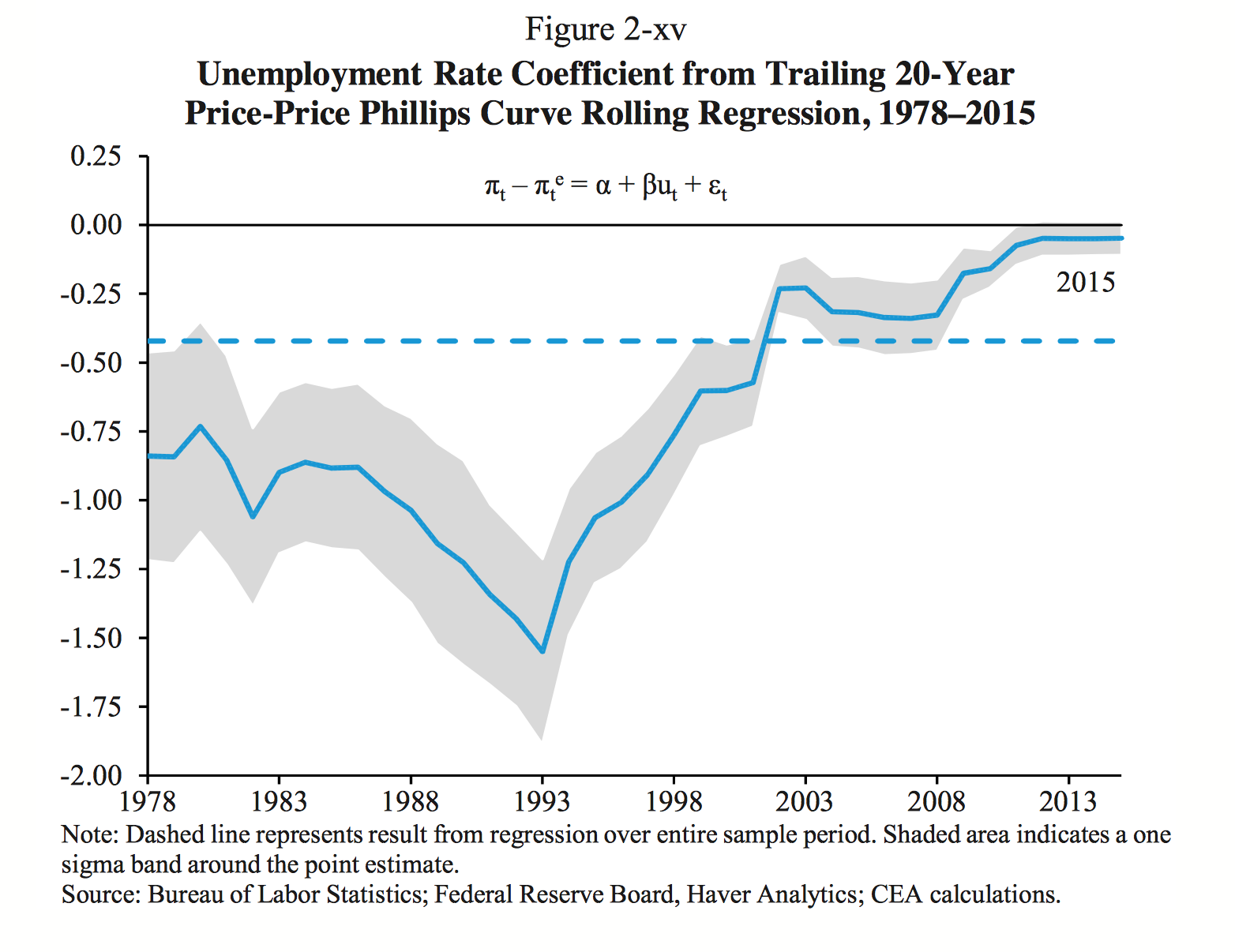

Lessons from the 1990s. I have a new paper coming out from the Roosevelt Institute, arguing that we’re not as close to potential as people at the Fed and elsewhere seem to believe, and as I’ve been talking with people about it, it’s become clear that your priors depend a lot on how you think of the rapid growth of the 1990s. If you think it was a technological one-off, with no value as precedent — a kind of macroeconomic Bush v. Gore — then you’re likely to see today’s low unemployment as reflecting an economy working at full capacity, despite the low employment-population ratio and very weak productivity growth. But if you think the mid-90s is a possible analogue to the situation facing policymakers today, then it seems relevant that the last sustained episode of 4 percent unemployment led not to inflation but to employers actively recruiting new entrants to the laborforce among students, poor people, even prisoners.

Inflation nutters. The Fed, of course, doesn’t agree: Undeterred by the complete disappearance of the statistical relationship between unemployment and inflation, they continue to see low unemployment as a threatening sign of incipient inflation (or something) that must be nipped in the bud. Whatever other effects rate increases may have, the historical evidence suggests that one definite consequence will be rising private and public debt ratios. Economists focus disproportionately on the behavioral effects of interest rate changes and ignore their effects on the existing debt stock because “thinking like an economist” means, among other things, thinking in terms of a world in which decisions are made once and for all, in response to “fundamentals” rather than to conditions inherited from the past.

{kind=link}

An army with only a signal corps. What are those other effects, though? Arguments for doubting central bankers’ control over macroeconomic outcomes have only gotten stronger than they were in the 2000s, when they were already strong; at the same time, when the ECB says, “let the government of Spain borrow at 2 percent,” it carries only a little less force than the God of genesis. I think we exaggerate power of central banks over real economy, but underestimate their power over financial markets (with the corollary that economists — heterodox as much as mainstream — see finance and real activity as much more tightly linked than they are).

It’s easy to be happy if you’re heterodox. This spring I was at a conference up at the University of Massachusetts, the headwaters of American heterodox economics, where I did my Phd. Seeing all my old friends reminded me what good prospects we in the heterodox world have – literally everyone I know from grad school has a good job. If you are wondering whether your prospects would be better at a nowhere-ranked heterodox economics program like UMass or a top-ranked program in some other social science, let me assure you, it’s the former by a mile — and you’ll probably have better drinking buddies as well.

The euro is not the gold standard. One of the topics I was talking about at the UMass conference was the euro which, I’ve argued, was intended to create something like a new gold standard, a hard financial constraint on governments. But that that was the intention doesn’t mean its the reality — in practice the TARGET2 system means that national central banks don’t face any binding constraint , unlike under the gold standard the central bank is “outside” the national monetary membrane. In this sense the euro is structurally more like Keynes’ proposals at Bretton Woods, it’s just not Keynes running it.

Can jobs be guaranteed? In principle I’m very sympathetic to the widespread (at least among my friends on social media) calls for a job guarantee. It makes sense as a direction of travel, implying a commitment to a much lower unemployment rate, expanded public employment, organizing work to fit people’s capabilities rather than vice versa, and increasing the power of workers vis-a-vis employers. But I have a nagging doubt: A job is contingent by its nature – without the threat of unemployment, can there even be employment as we know it?

The wit and wisdom of Haavelmo. I was talking a while back about Merijn Knibbe’s articles on the disconnect between economic theory and the national accounts with my friend Enno, and he mentioned Trygve Haavelmo’s 1944 article on The Probability Approach in Econometrics, which I’ve finally gotten around to reading. One of the big points of this brilliant article is that economic variables, and the models they enter into, are meaningful only via the concrete practices through which the variables are measured. A bigger point is that we study economics in order to “become master of the happenings of real life”: You can contribute to economics in the course of advancing a political project, or making money in financial markets, or administering a government agency (Keynes did all three), but you will not contribute if you pursue economics as an end in itself.

Coney Island. Laura and I took the boy down to Coney Island a couple days ago, a lovely day, his first roller coaster ride, rambling on the beach, a Cyclones game. One of the wonderful things about Coney Island is how little it’s changed from a century ago — I was rereading Delmore Schwartz’s In Dreams Begin Responsibilities the other day, and the title story’s description of a young immigrant couple walking the boardwalk in 1909 could easily be set today — so it’s disconcerting to think that the boy will never take his grandchildren there. It will all be under water.